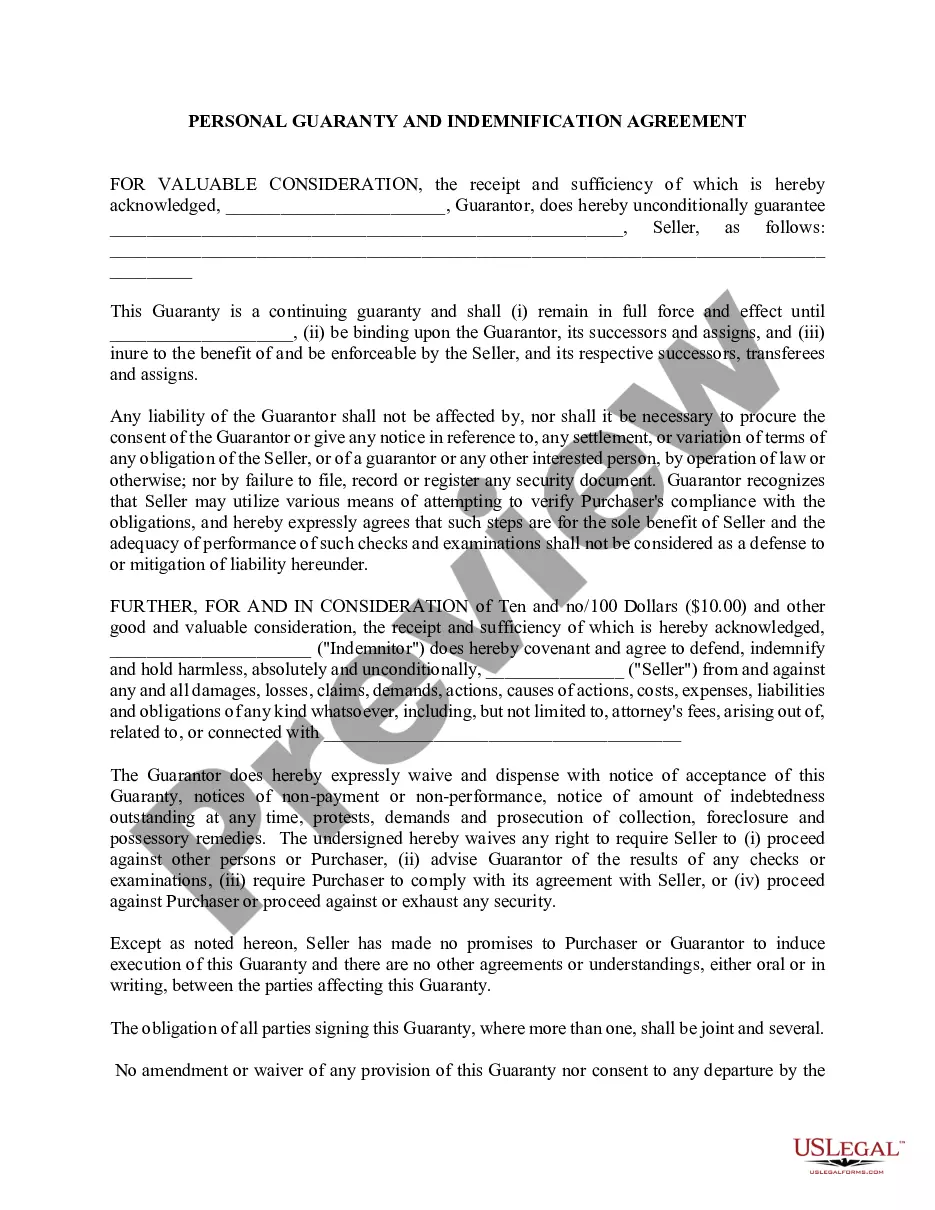

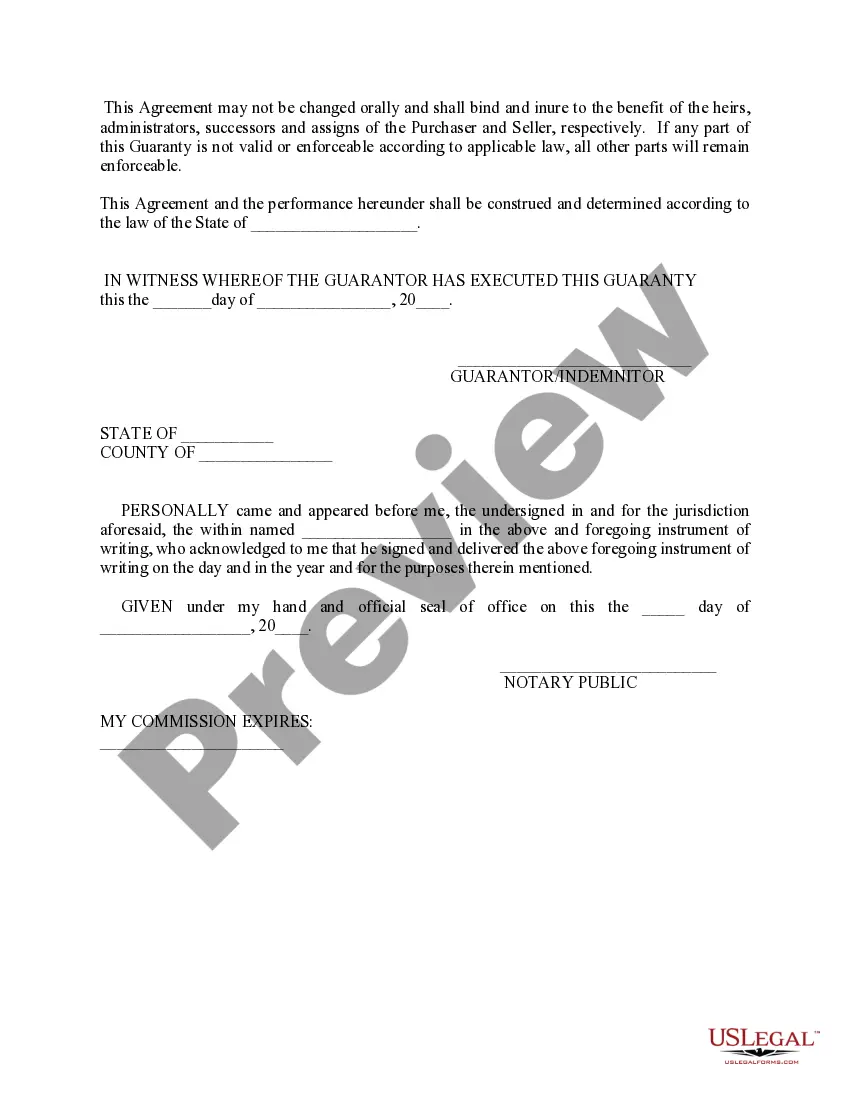

A personal guarantee letter is a legally binding document that serves as a promise from an individual to be personally responsible for fulfilling the financial obligations of another party. This document is commonly used in various situations where a borrower, such as a small business owner or a student, lacks sufficient creditworthiness or collateral to secure a loan or a lease agreement. The personal guarantee letter reassures the lender or landlord that they can rely on the personal assets and income of the guarantor to recover any outstanding debt if the primary borrower defaults. In essence, a personal guarantee letter embodies the commitment and assurance of the guarantor to assume liability for any financial loss incurred by the lender or landlord. It is crucial to include certain key elements in the personal guarantee letter to make it effective and legally enforceable. These elements typically consist of: 1. Names and Contact Information: The personal guarantee letter should begin with the full names, addresses, and contact details of both the guarantor and the primary borrower. Including these details ensures clarity and unequivocal identification of the involved parties. 2. Purpose of the Guarantee: Clearly state the purpose for which the personal guarantee is being provided, such as a loan, lease agreement, or contract. This part of the letter should highlight the exact terms and conditions being guaranteed, including the amount borrowed or leased, repayment period, interest rates, and any other relevant details pertaining to the financial arrangement. 3. Personal Liability: Explicitly mention that the guarantor is assuming personal liability for the debt or obligation in case of default by the primary borrower. This expresses the guarantor's willingness to be legally responsible for the outstanding amount and any associated costs, such as interest or penalties. 4. Release and Waiver: It is advisable for the guarantor to include a statement waiving any rights they may have against the lender or landlord until the primary borrower's obligation has been fully discharged and liquidated. This ensures that the guarantor cannot hold the lender liable for any actions related to the loan or lease agreement. 5. Governing Law and Jurisdiction: Specify the law that governs the personal guarantee letter and indicate the jurisdiction in which any legal disputes arising from the guarantee will be resolved. This aspect helps establish the legal framework and provides clarity on the rights and obligations of the parties involved. Examples of personal guarantee letters can vary depending on the specific type of financial arrangement in question. Some common types include: 1. Loan Guarantee Letter: This type of personal guarantee letter is typically used when an individual serves as a guarantor for a loan, ensuring that the lender will be repaid even if the primary borrower defaults. 2. Lease Guarantee Letter: In situations where a potential tenant lacks sufficient credit history or income to secure a lease agreement, a lease guarantee letter can be employed. The guarantor becomes personally liable for covering any unpaid rent or damages caused by the tenant. 3. Business Loan Guarantee Letter: When a business owner seeks a loan for their company, but the lender requires additional assurance, a personal guarantee letter can be used. The business owner becomes the guarantor, assuming responsibility for the loan if the business fails to repay. 4. Student Loan Guarantee Letter: Students who lack a credit history or a satisfactory income may require a personal guarantee letter when applying for student loans. In this case, a parent or guardian typically serves as the guarantor to ensure that the loan will be repaid if the student defaults. By incorporating the necessary elements and understanding the various types of personal guarantee letters, individuals can establish a clear and legally binding commitment when assuming responsibility for someone else's financial obligations.

Example Of Personal Guarantee Letter

Description

How to fill out Example Of Personal Guarantee Letter?

Accessing legal templates that meet the federal and state regulations is essential, and the internet offers numerous options to pick from. But what’s the point in wasting time searching for the correctly drafted Example Of Personal Guarantee Letter sample on the web if the US Legal Forms online library already has such templates collected in one place?

US Legal Forms is the biggest online legal catalog with over 85,000 fillable templates drafted by attorneys for any professional and personal situation. They are simple to browse with all documents arranged by state and purpose of use. Our professionals stay up with legislative changes, so you can always be confident your paperwork is up to date and compliant when acquiring a Example Of Personal Guarantee Letter from our website.

Obtaining a Example Of Personal Guarantee Letter is quick and easy for both current and new users. If you already have an account with a valid subscription, log in and download the document sample you need in the preferred format. If you are new to our website, follow the steps below:

- Examine the template utilizing the Preview feature or through the text outline to ensure it meets your requirements.

- Locate another sample utilizing the search tool at the top of the page if needed.

- Click Buy Now when you’ve found the right form and choose a subscription plan.

- Create an account or sign in and make a payment with PayPal or a credit card.

- Choose the right format for your Example Of Personal Guarantee Letter and download it.

All documents you locate through US Legal Forms are multi-usable. To re-download and complete previously obtained forms, open the My Forms tab in your profile. Take advantage of the most extensive and easy-to-use legal paperwork service!

Form popularity

FAQ

A guarantor's form should include a space to fill in the home address, work address, phone number, and email address. The contact details are what will be used to contact the guarantor in the future if the principal fails to meet agreement terms. This is a very important feature of the guarantor's form.

Corporate credit cards that are issued to an individual are another example of a personal guarantee. The individual or employee is responsible for the debt that the organization takes on and the overall spending on the credit card. Here, the cardholder takes the role of a guarantor.

Your guarantor will have to sign a contract with the letting agent or landlord. This will set out the terms of the guarantor and their responsibilities to the property. Most contracts will state that a guarantor is liable to cover any unpaid rent for the length of the tenancy.

A guaranteed loan is used by borrowers with poor credit or little in the way of financial resources; it enables financially unattractive candidates to qualify for a loan and assures that the lender won't lose money. Guaranteed mortgages, federal student loans, and payday loans are all examples of guaranteed loans.

The letter should include the name and address of the guarantor, a statement of their willingness to guarantee any debts or obligations of the other party, an explanation of the obligations being guaranteed, the period of time for which the obligations will continue, and the date of the agreement.