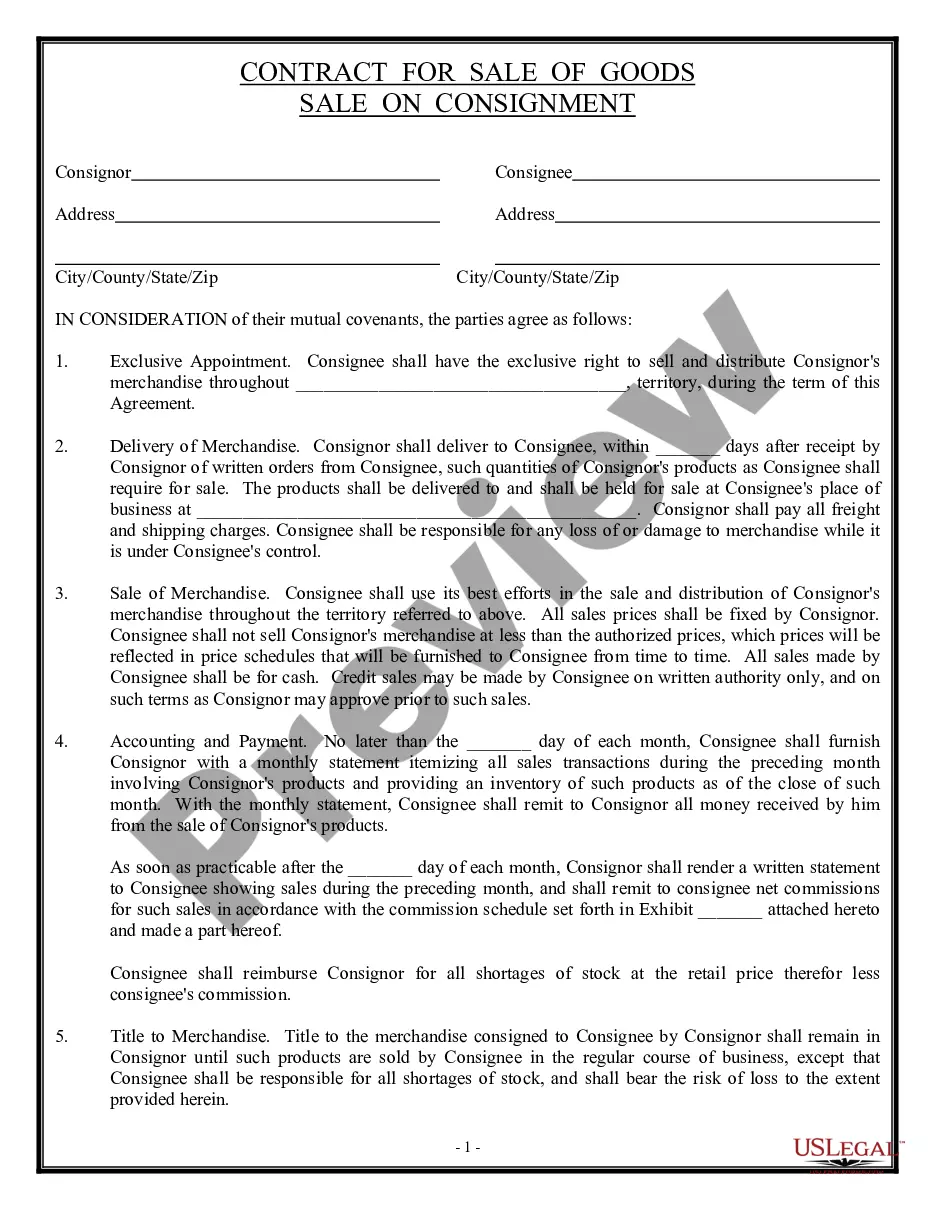

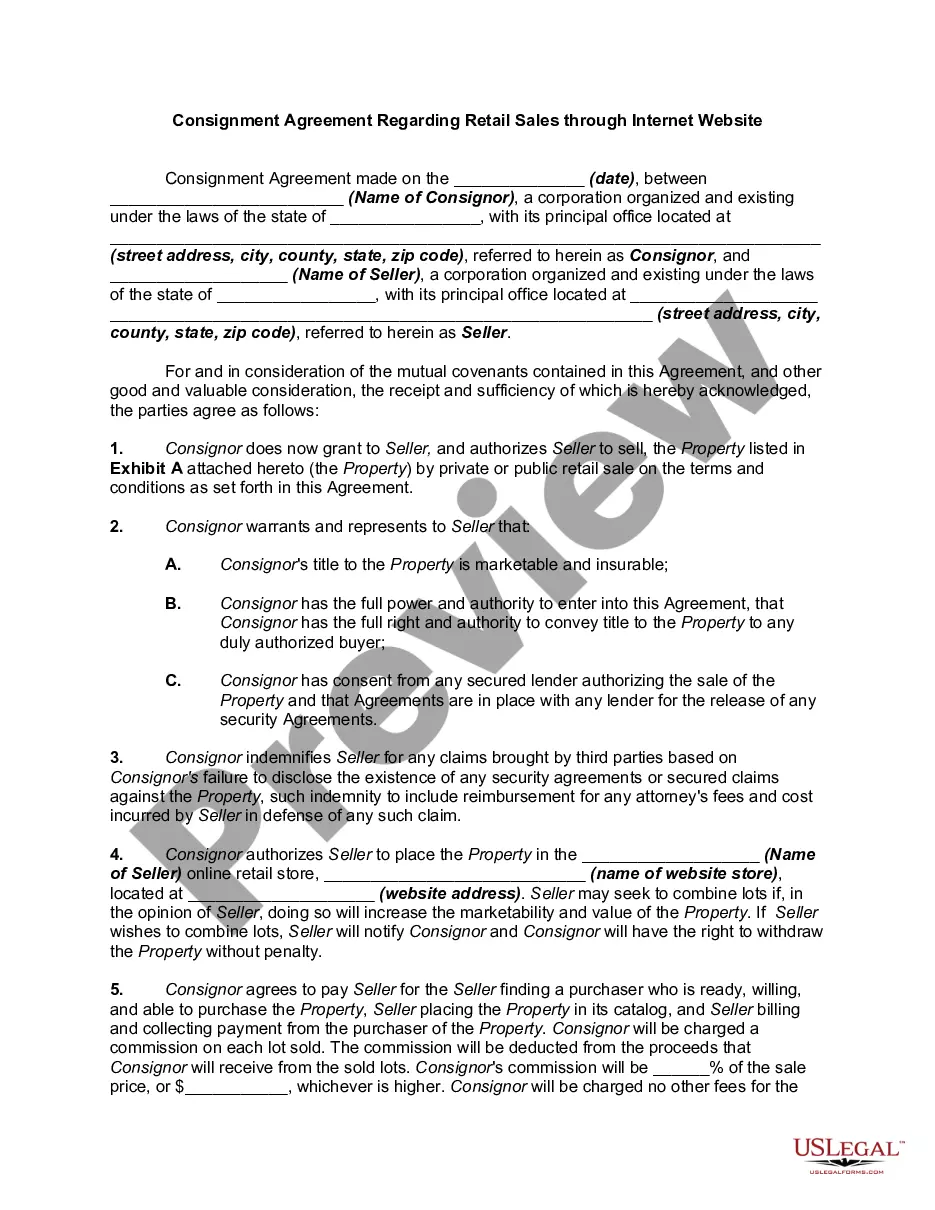

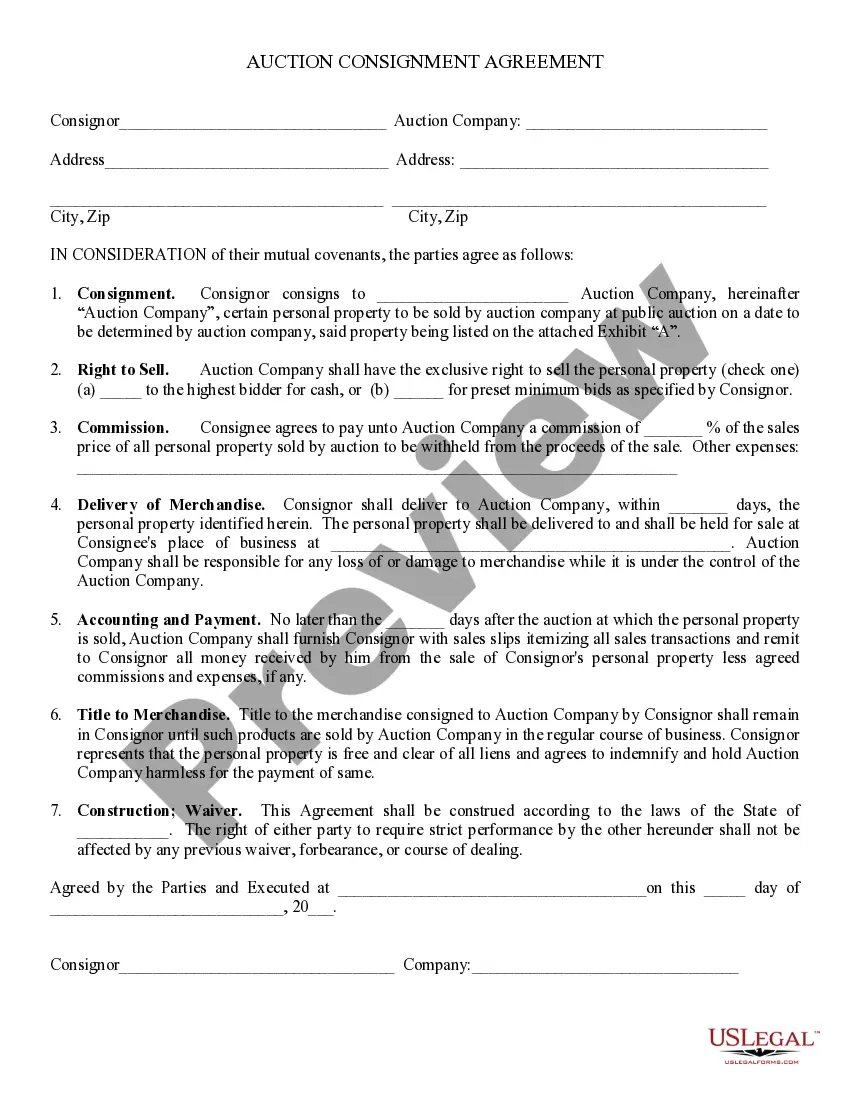

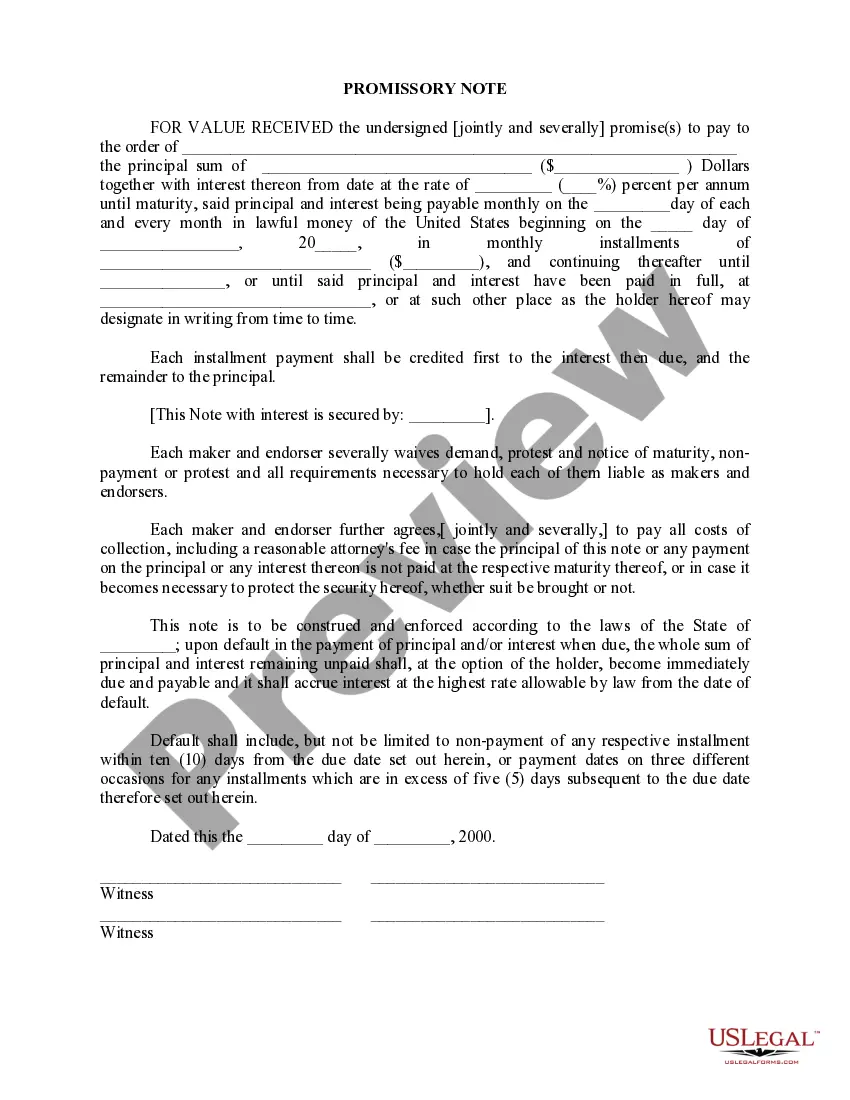

Consignment Note For Fridges In Illinois

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Use tax is a tax imposed on the privilege of using, in Illinois, any item of tangible personal property that is purchased anywhere at retail.

Some customers are exempt from paying sales tax under Illinois law. Examples include government agencies, some nonprofit organizations, and merchants purchasing goods for resale. Sellers are required to collect a valid exemption or resale certificate from buyers to validate each exempt transaction.

Beginning January 1, 2026, Illinois will repeal the 1% sales and use grocery tax on food for human consumption that is to be consumed off premises where it is sold.

Effective January 1, 2025, retailers previously obligated to collect and remit Illinois Use Tax (UT) on retail sales sourced outside of Illinois and made to Illinois customers are now subject to destination-based retailers' occupation tax (ROT).

The following types of income are exempt from Illinois Income Tax: Interest on U.S. Treasury bonds, notes, bills, certificates, and savings bonds.

Illinois' general state retailers' occupation and use tax rates are: 6.25 percent on general merchandise, including items required to be titled or registered by an agency of Illinois state government; and. 1 percent on qualifying foods, drugs, and medical appliances.

Other common Illinois exemptions include: Charitable, religious, educational, or government organizations. However, exemptions for charitable organizations vary in scope and requirements. Manufacturing machinery and equipment. Interstate commerce. Planes, trains, trucks, etc.

Illinois requires retailers, including those operating through third-party marketplaces, to collect and remit tax based on the customer's location. This includes both in-state and remote sellers meeting the economic nexus threshold (e.g., $100,000 in sales or 200 transactions annually in Illinois).

If the customer picks up the item at the seller's location, tax should be collected for the state in which the seller is located. If the item is shipped to the customer, then tax applies for the delivery state, whether that is the same state where the seller is located or a different state.

Illinois recognizes economic nexus for any vendor with $100,000 or more in cumulative gross receipts or 200 or more transactions into Illinois from sales of tangible personal property. Once you have economic nexus established, you will be obligated to collect sales tax from buyers in the state.