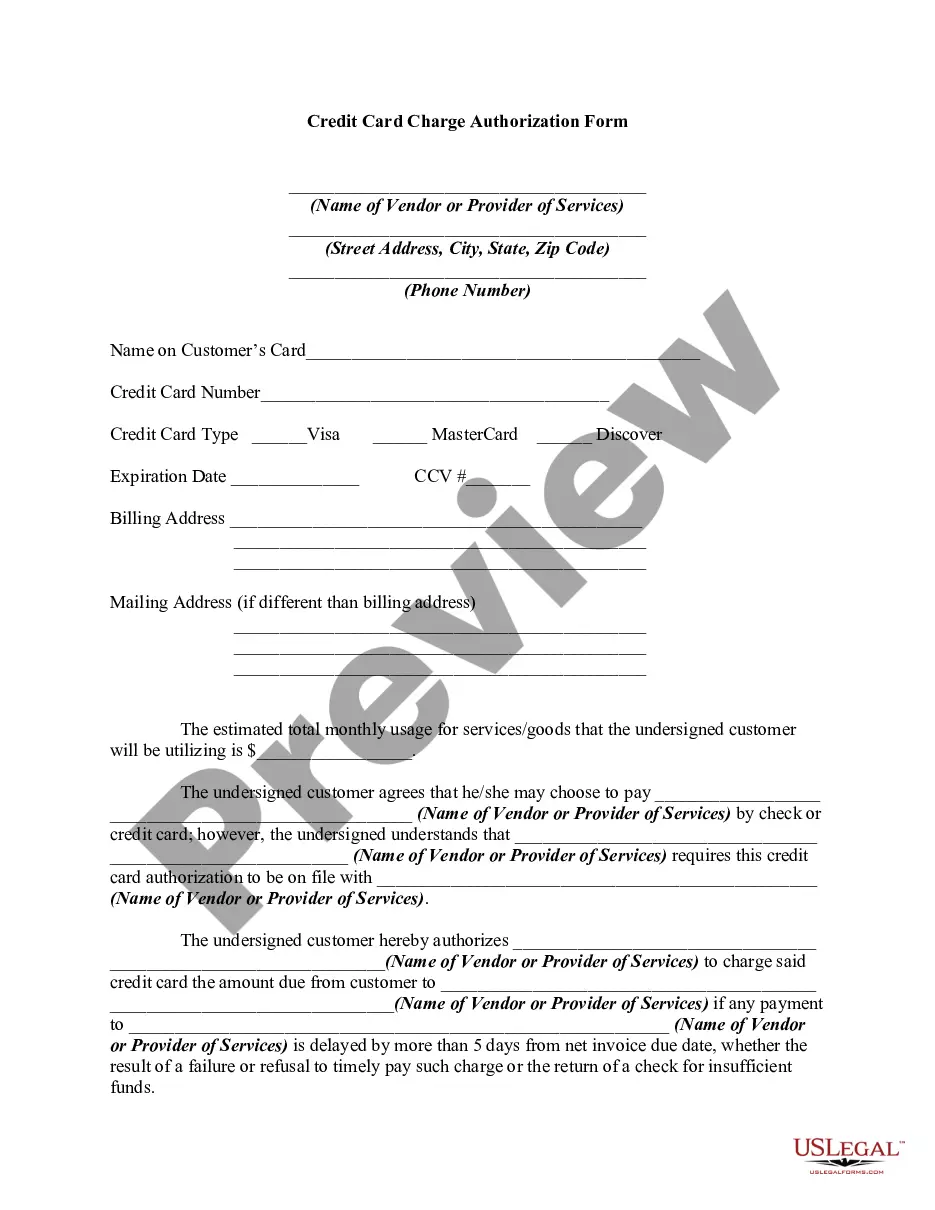

Credit Card Form Statement With Validation In Salt Lake

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Once you receive a debt validation notice, review it promptly and carefully. If you don't respond with a debt verification request within the 30-day dispute period, the collector will assume the debt is legitimate. It can become more difficult to assert your rights once the process moves forward.

The Fair Debt Collection Practices Act (FDCPA) forbids debt collectors from harassing, oppressing, or abusing the debtor or anyone they contact regarding debt repayment. Some examples of harassment are: Repetitive phone calls made with the intent to annoy, abuse, or harass. Usage of obscene or offensive language.

Summary: It can take up to 30 days for a debt collector to respond to a debt validation letter, if they ever respond at all. Failure to validate a debt could be considered a violation of the FDCPA. Learn more about your rights to protect your rights.

A debt validation letter is a document from a debt collector providing information about a debt you may owe. Collection agencies are required by law to provide validation notices and give you time to dispute the debt.

What happens if the creditor does not respond within the required time? If the creditor does not respond within 30 days, TransUnion will delete the information from your credit report. Why did the disputed item not come off my credit report?

(5) Validation period means the period starting on the date that a debt collector provides the validation information required by paragraph (c) of this section and ending 30 days after the consumer receives or is assumed to receive the validation information.

In Utah, for most debts, a creditor has six years to take legal action on that unpaid debt. After the statute of limitations expires, a creditor or debt collector can no longer sue you for the debt.

It's a violation of the FDCPA for a debt collector to refuse to send a validation notice or fail to respond to your verification letter. If you encounter such behavior, you can file a complaint with the CFPB, the Federal Trade Commission or your state's attorney general.

If these forms are not stored securely or are accessible to unauthorized individuals, it increases the likelihood of credit card fraud or data breaches. Transmission of Information: Transmitting paper forms with credit card details via fax, mail, or email is not secure.

10 Things To Check In Your Credit Card Statement Statement date. Understanding your statement date is like getting the key to your financial diary. Payment due date. Billing cycle. Grace period. Transaction details. Total amount due. Minimum amount due. Credit limit availability.