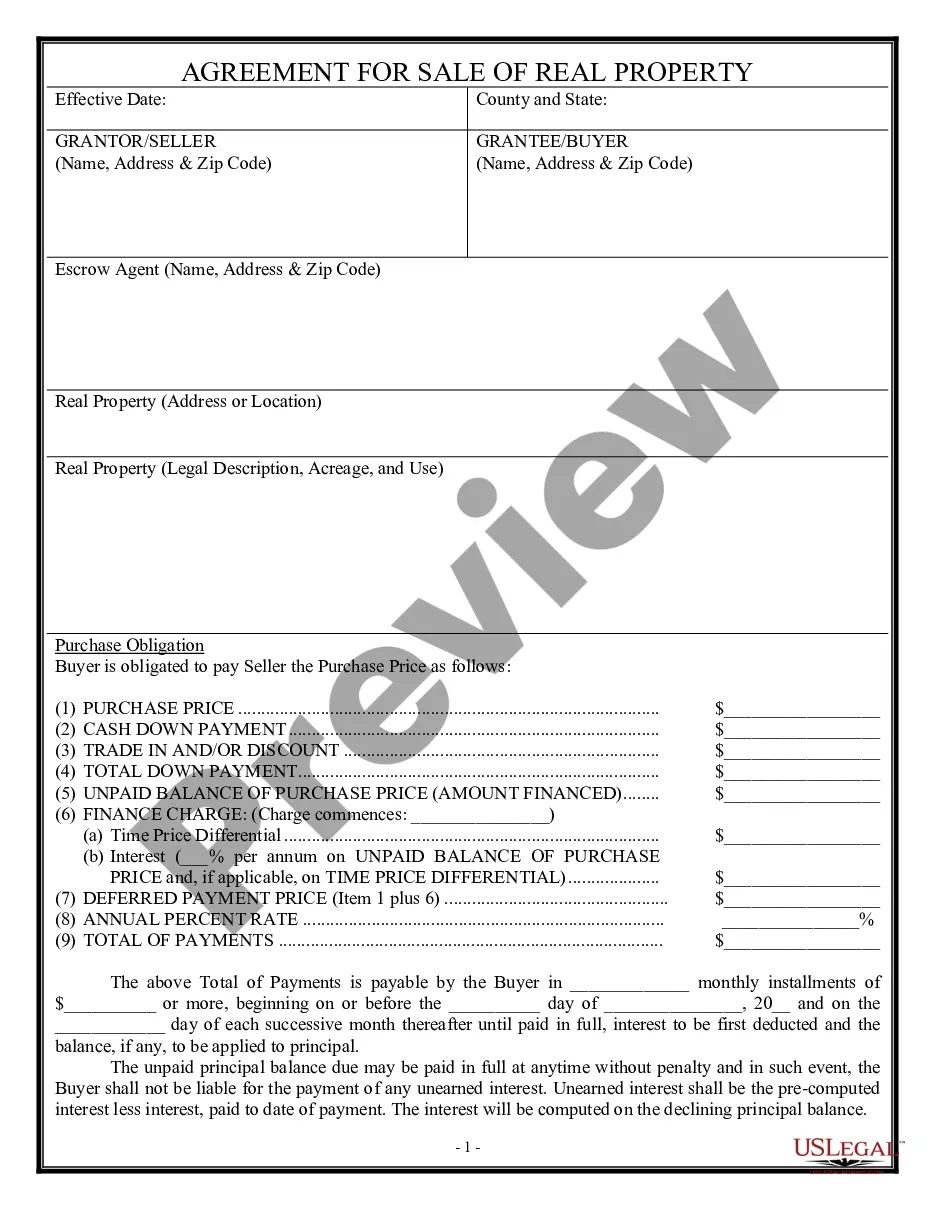

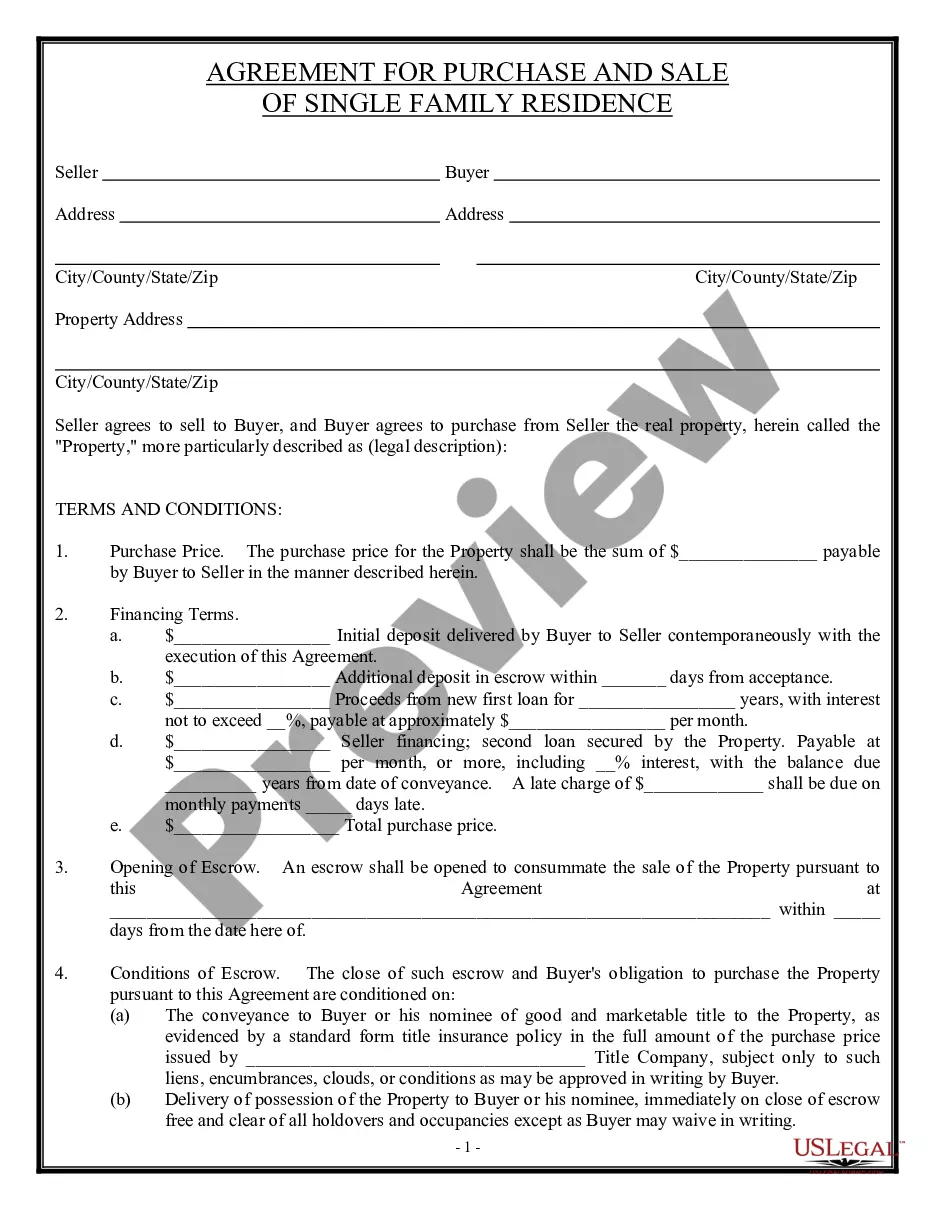

Closing Property Title Without Paying Taxes In California

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Prop. 19 would allow a property owner to transfer their low property tax up to three times. Second, Prop. 19 would limit the transfer of low property tax assessments from deceased owners to their children or grandchildren (if all of their children have already died), which current law allows.

In November 2020, California voters passed Proposition 19, which made changes to property tax benefits for families, seniors, severely disabled persons, and victims of natural disasters. These changes became effective in February and April 2021, depending on the component of the measure.

As provided by the California Constitution, certain qualified properties are exempt from paying property taxes. Examples include properties used exclusively for religious, scientific, hospital or charitable purposes.

Senior Tax Exemptions in California The Senior Citizen Homeowners' Property Tax Exemption is available to homeowners who are at least 65 years old and meet certain income requirements.

By California law, whoever owns the property on January 1st of the current calendar year is responsible for taxes up until the close of escrow date. Once the close of escrow is completed, the new owner is responsible for that year's property taxes at a prorated amount.

You do not have to report the sale of your home if all of the following apply: Your gain from the sale was less than $250,000. You have not used the exclusion in the last 2 years. You owned and occupied the home for at least 2 years.

The home must have been the principal place of residence of the owner on the lien date, January 1st. To claim the exemption, the homeowner must make a one-time filing with the county assessor where the property is located.

California Property Tax Planning under Proposition 19 If the LLC is the original owner, then as long as no new person gains more than 50% ownership/control of the LLC, then there will be no reassessment of the underlying property.

Under California law, repairs or basic remodeling work are generally not considered subject to reassessment (e.g. fixing a roof, carpeting, cabinets, windows, or countertops), assuming no new square footage or fixtures are added. However, new construction is assessable and can increase your property tax base.

The $1 million exclusion applies separately to each eligible transferor. Transfers may be result of a sale, gift, or inheritance. A transfer via a trust also qualifies for this exclusion. For property tax purposes, we look through the trust to the present beneficial owner.