File Notice Lis Pendens Foreclosure In Tarrant

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

When can a lender start foreclosure? Most loans from a bank must be 120 days delinquent before any foreclosure activity starts. However, smaller lenders can sometimes start foreclosure even if you are only one day late. The lender is only required to send you two notices before a foreclosure sale.

Texas is a power of sale jurisdiction, meaning that a lender can go through with the sale of your property without having to go to court. As a result, foreclosures in Texas can be very quick, sometimes being completed about two or three months after the process begins, though this is quicker than average.

In Texas, the types of foreclosure include expedited, judicial, and non-judicial. Most foreclosures are non-judicial types. This means court approval isn't required and speeds up the process. Many Texas foreclosures take 160 days.

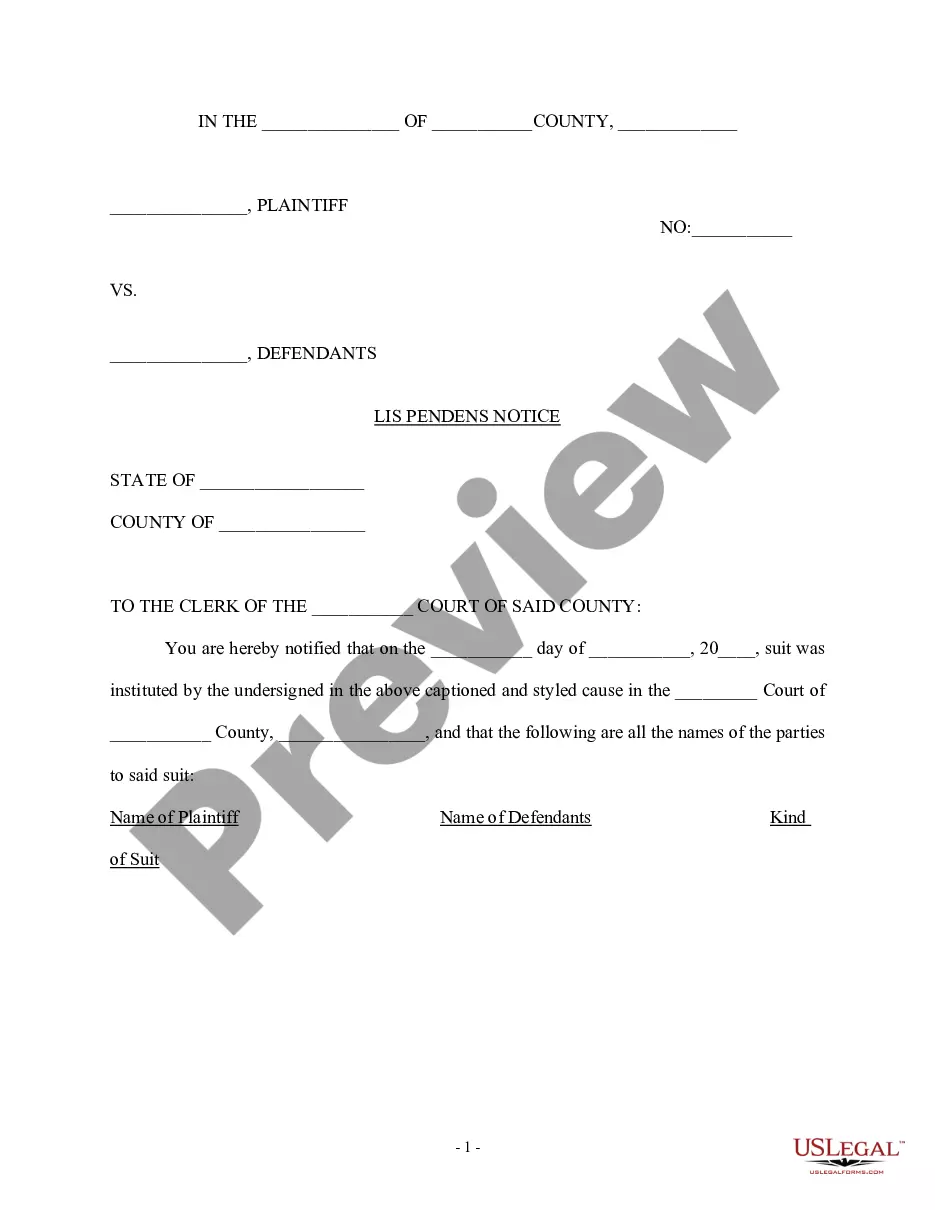

To file a Lis Pendens in Texas, the party initiating the lawsuit must follow procedures outlined in the Texas Property Code. This includes submitting a declarative affidavit to the county clerk's office where the property is located. The affidavit must generally contain: Names of the parties involved.

We can outline the key timeline events in the Texas foreclosure process. Generally, homeowners fall into default after missing 3-6 months of mortgage payments. Upon reaching at least 120 days behind on payments, homeowners may receive a notice of default.

It's important to note that homeowners in Texas also have legal options to stop foreclosure. These solutions often require professional legal guidance, and they can provide effective solutions for keeping your home or other property.

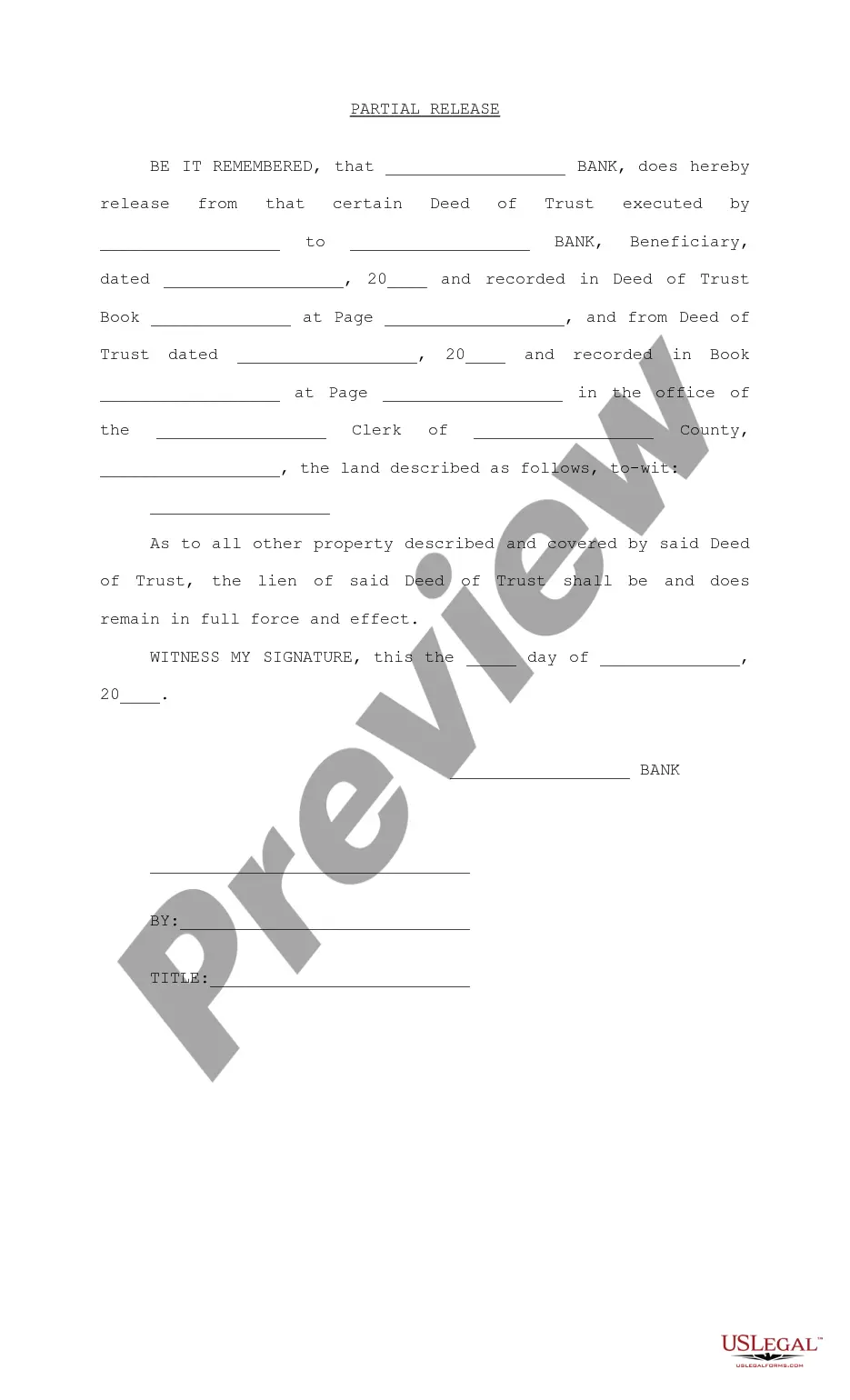

A release of lis pendens under Texas law to provide notice to third parties that litigation is resolved and title to real property is no longer in controversy.

Short Answer: After filing a lis pendens, property sales may stall due to legal disputes impacting the title. Misfiling can result in sanctions or slander of title damages. Removal involves court-ordered expungement or voluntary discharge.

(2) A notice of lis pendens is not effectual for any purpose beyond 1 year from the commencement of the action and will expire at that time, unless the relief sought is disclosed by the pending pleading to be founded on a duly recorded instrument or on a lien claimed under part I of chapter 713 against the property ...

The titleholder can sell a property and transfer the deed to someone else while subject to a lis pendens. However, most title companies will not provide insurance for homes with a lis pendens, and closing agents may close with the lien being bonded.