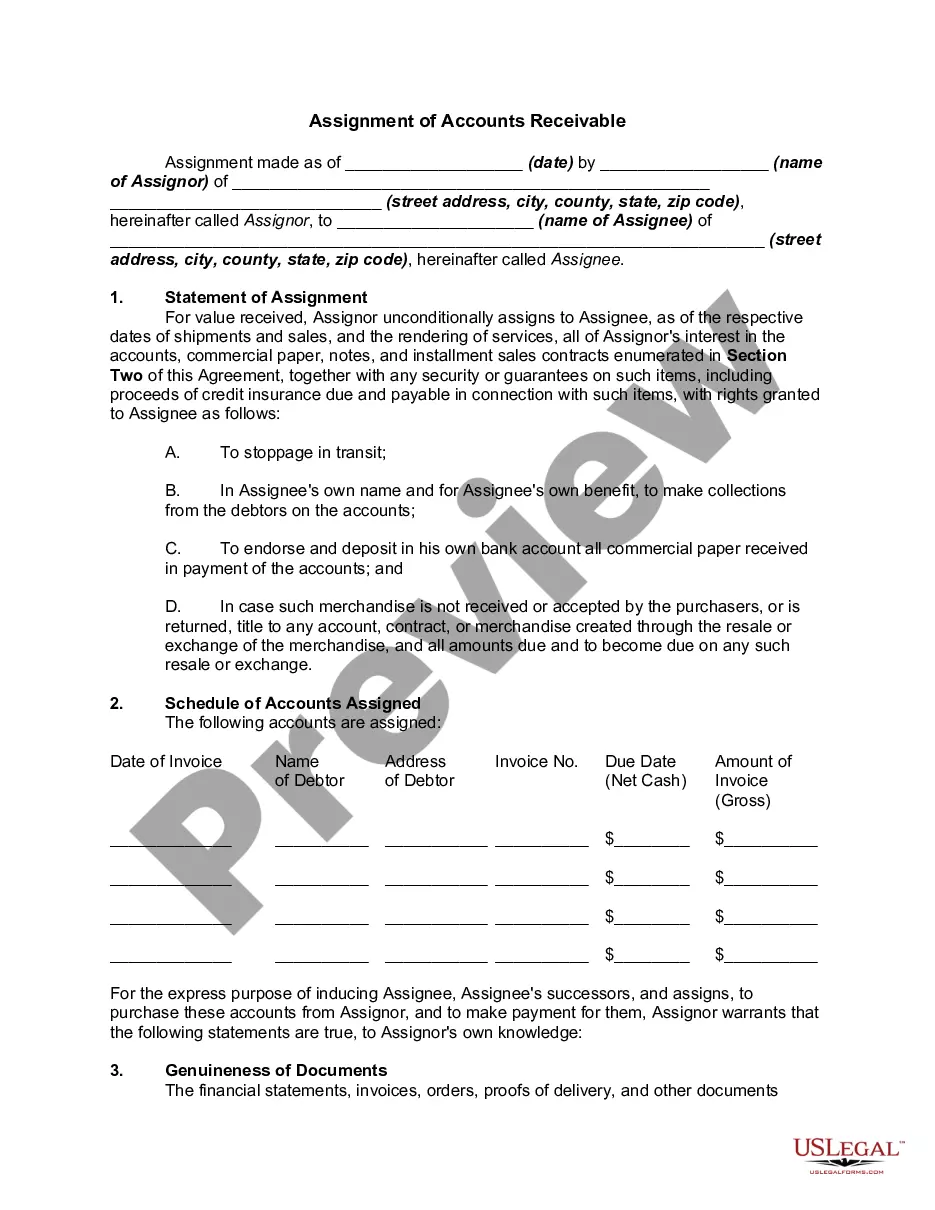

Accounts Receivable Contract With Nike In Nevada

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

The key difference between Contract asset and Account receivable is its conditionality i.e. Contract Asset is recognized in the Financial Statements when the right to receive the payment is conditional upon something other than just passage of time (having conditional right to receive payment).

Contract Receivables means, with respect to a Contract, all amounts due and payable or to become due and payable under such Contract, together with all rights to receive such amounts under such Contract.

Contract AR should be entered when the revenue has been earned but not collected. This normally occurs at the time goods or services are provided and should coincide when the invoice is sent. Postponing the recording of contract AR until the payment is received is not encouraged.

NIKE Brand Revenue was up 10 percent to a record $18.1 billion. Our Other Businesses grew 9 percent to a record $2.7 billion. NIKE Brand Futures orders are up 15 percent. And Earnings Per Share grew 14 percent, coming in at $4.39 – also a new record.

Sumerra is managing the audit process, Nike FCO program, on behalf of Nike – Working with Nike, Third Party Auditors, Licensees and Factories to ensure the audits are done in the right manner and at the right time.

Nike's accounts payable hit its 5-year low in May 2020 of 2.248 billion. Nike's accounts payable decreased in 2020 (2.248 billion, -13.9%), 2023 (2.862 billion, -14.8%), and 2024 (2.851 billion, -0.4%) and increased in 2021 (2.836 billion, +26.2%) and 2022 (3.358 billion, +18.4%).

Nike's operated at median receivables turnover of 11.6x from fiscal years ending May 2020 to 2024. Looking back at the last 5 years, Nike's receivables turnover peaked in May 2021 at 12.4x. Nike's receivables turnover hit its 5-year low in May 2022 of 10.2x.