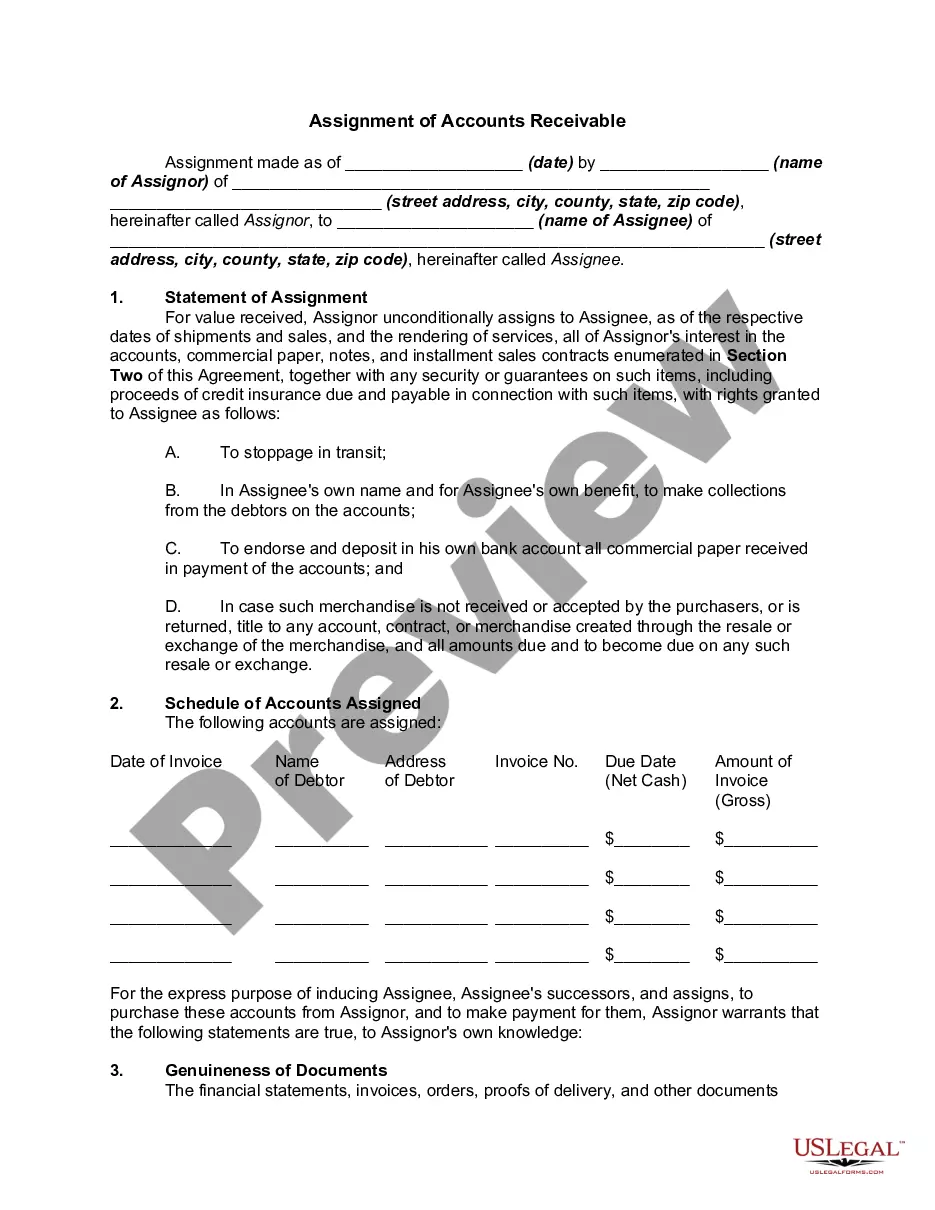

Net Receivable Sales Formula In Arizona

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Find the total sales for each year and the total value of all annual outstanding accounts. Find the average percentage that the debt accounted for and divide the value by your total sales figures for each year. You can then apply that percentage to your current sales figures.

How to Calculate Net Accounts Receivable? To calculate net accounts receivable, you need: total accounts receivable, allowance for doubtful accounts, and sales returns and allowances. Then, subtract the allowance for doubtful accounts, sales returns and allowances from the Total Account Receivables.

To calculate a company's DSO, you divide its accounts receivable by its total credit sales and multiply the result by the total amount of days within the period. The formula is:DSO = (accounts receivable / credit sales) x number days in specific periodRelated: Q&A: What Is Accounts Receivable and How Does It Work?

The days' sales in accounts receivable is calculated as follows: the number of days in the year (use 360 or 365) divided by the accounts receivable turnover ratio during a past year.

States using this apportionment formula—say Arizona, for example—place greater emphasis on sales derived from the state to apportion taxable income. A business with 20% of its payroll, 40% of its property, and 50% of its sales in Arizona would give a double portion or 100% to sales.

This form is an information return. An information return that is incomplete or filed after its due date (including extensions) is subject to a penalty of $100 per month or fraction of a month during which the failure continues, up to a maximum penalty of $500.

Arizona charges a flat income tax of 2.50% on all income brackets and filing statuses. This flay income tax rate applies to Arizona taxable income. The starting point for computing Arizona taxable income is federal adjusted gross income (AGI).

All business income of each trade or business of the taxpayer shall be apportioned to this state by use of the apportionment formula in A.R.S. § 43-1139. The elements of the apportionment formula are the property factor, the payroll factor, and the sales factor of the trade or business of the taxpayer.

For the 2023, the Arizona Pass-Through Entity (PTE) income tax is assessed at a rate of 2.50% of the income attributable to the partnership's or S Corporation's resident partners or shareholders, and the income derived from sources within Arizona attributable to the nonresident partners or shareholders.

A limited liability company (LLC) that is classified as a partnership for federal income tax purposes must file Arizona Form 165. A single-member LLC that is disregarded as an entity for federal income tax purposes is treated as a branch or division of its owner, and is included in the tax return of its owner.