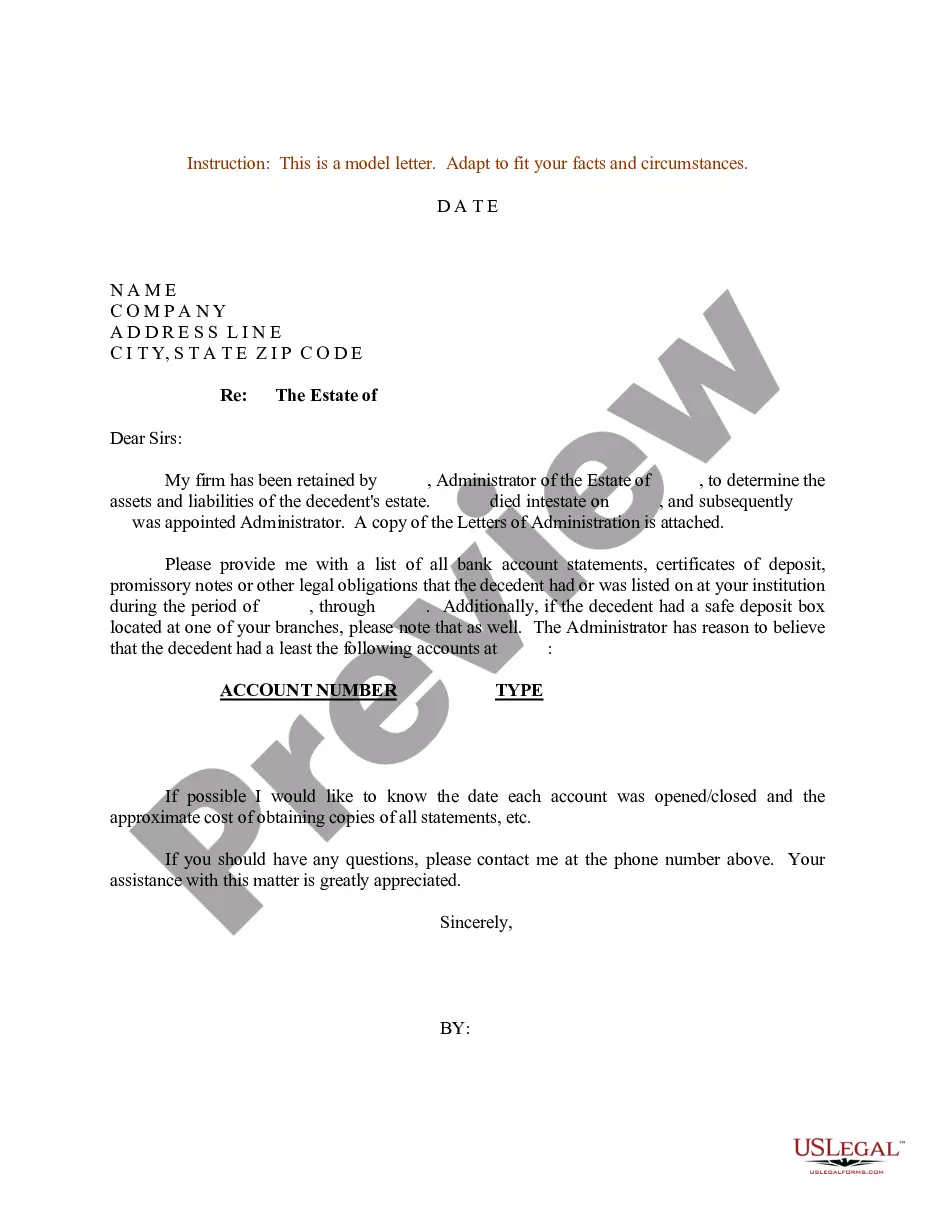

Decedent Account Bank Format In Oakland

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

It's best to open an estate account with the decedent's bank in the state where they lived.

When a person passes away, their assets are distributed in ance with either their estate plan or California's intestate succession laws. However, certain assets, including most bank accounts, can pass directly to beneficiaries, without the need for probate or the court's intervention.

Six Steps of the Probate Process Step 1: File a petition to begin probate. You'll have to file a request in the county where the deceased person lived at the time of their death. Step 2: Give notice. Step 3: Inventory assets. Step 4: Handle bills and debts. Step 5: Distribute remaining assets. Step 6: Close the estate.

The account holder only needs to notify their bank of who the beneficiary should be. The bank, on its end, will give the account owner a beneficiary designation form to fill out. The completed form gives the bank authorization to convert the account to a POD.

How to open an estate account Step 1: Begin the probate process. The steps for beginning this process depend on the state in which the deceased person resided. Step 2: Obtain a tax ID number for the estate account. Step 3: Bring all required documents to the bank. Step 4: Open the estate account.

Once you've been appointed as the personal representative of a loved one's estate, you should open an estate checking account. An estate checking account serves as a temporary account to manage the estate's financial affairs.

Who can access and close the deceased's bank account? The executor named in the will can do this, or if no executor has been nominated, the administrator (main beneficiary). They'll contact the bank in question with proof of death to begin the process. The Death Certificate is typically accepted as proof.

Visit Banks in Their Area You will need to provide documentation to prove both that the account holder died and you have the legal authority (as a designated beneficiary, joint account holder or executor/administrator) to access the account.

In these cases, simply visit the bank with a valid ID and a certified copy of the death certificate. You will then have access to the account, allowing you to withdraw the funds as needed.

Rule: (a) Upon the death of an accountholder, the FDIC will insure the deceased owner's accounts as if he or she were still alive for six months after his or her death.