Retirement Plans For Dummies In San Bernardino

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

The $1,000 per month rule is designed to help you estimate the amount of savings required to generate a steady monthly income during retirement. ing to this rule, for every $240,000 you save, you can withdraw $1,000 per month if you stick to a 5% annual withdrawal rate.

The safe withdrawal rule is a classic in retirement planning. It maintains that you can live comfortably on your retirement savings if you withdraw 3% to 4% of the balance you had at retirement each year, adjusted for inflation.

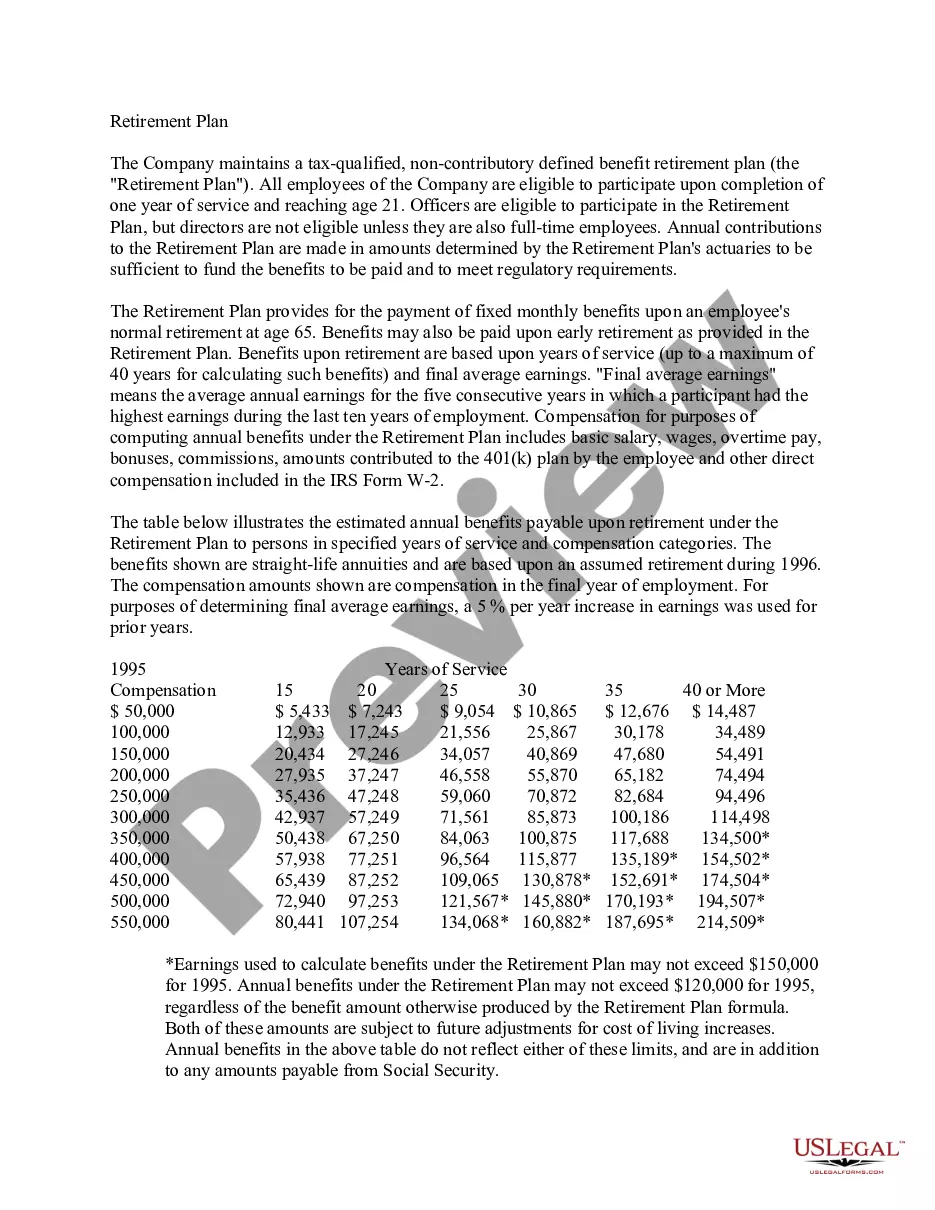

Your retirement benefit is calculated using a formula with three factors: Service credit (Years) multiplied by your benefit factor (percentage per year) multiplied by your final monthly compensation equals your unmodified allowance. Service Credit - Total years of employment with a CalPERS employer.

The San Bernardino County Employees' Retirement Association (SBCERA) is an independent, defined benefit pension plan providing retirement, disability, and death benefits on behalf of approximately 50,000 members and beneficiaries.

Examples of defined contribution plans include 401(k) plans, 403(b) plans, employee stock ownership plans, and profit-sharing plans. A Simplified Employee Pension Plan (SEP) is a relatively uncomplicated retirement savings vehicle.

The average annual CalPERS pension for all retirees who retired with a service retirement is $42,516, which breaks down to more than $3,500 per month. Overall, 61.6% of all CalPERS service retirees receive $3,500 a month or less, while only 6.4% receive more than $9,000 per month.

CalPERS offers a defined benefit plan where retirement benefits are based on a formula, rather than contributions and earnings to a savings plan. Retirement benefits are calculated based on a member's years of service credit, age at retirement, and final compensation (average salary for a defined period of employment).

Disadvantages of Early Retirement Foregoing employer-sponsored health care costs. Getting hit with penalties and fines for accessing your retirement funds early. Realizing a loss of benefits.

The minimum retirement age for service retirement for most members is 50 years with five years of service credit. The more service credit you have, the higher your retirement benefits will be.