Escrow Agreement Example In Virginia

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

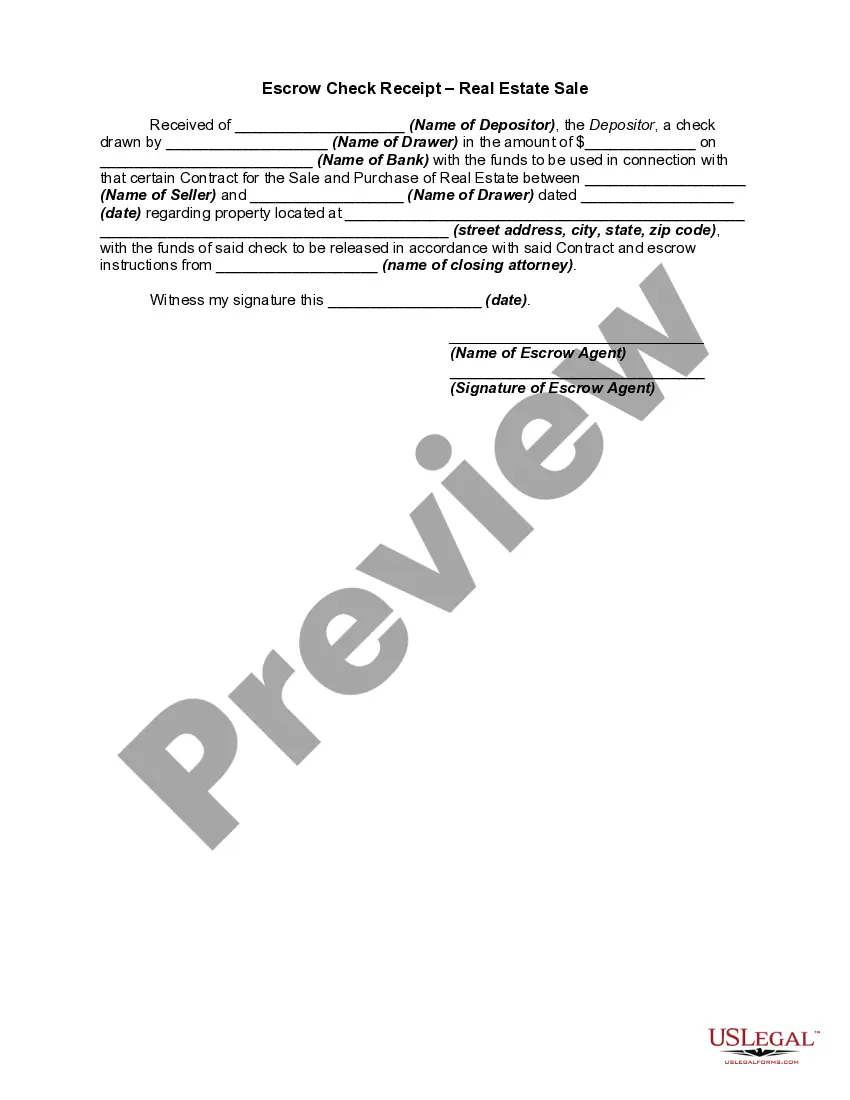

Virginia Escrow Laws These state that the account must be set up with a federally insured institution, such as a bank, and be designated as an escrow account for the specific real estate transaction. Every check deposited into or written from the account, as well as statements, must be clearly labeled as escrow funds.

An escrow agreement normally includes information such as: The identity of the appointed escrow agent. Definitions for any expressions pertinent to the agreement. The escrow funds and detailed conditions for the release of these funds.

The Escrow Holder: prepares escrow instructions. requests a preliminary title search to determine the present condition of title to the property. requests a beneficiary's statement if debt or obligation is to be taken over by the buyer. complies with lender's requirements, specified in the escrow agreement.

The supervising broker and any other licensee with escrow account authority may be held responsible for these accounts. All such accounts, checks, and bank statements shall be labeled "escrow" and the accounts shall be designated as "escrow" accounts with the financial institution where such accounts are established.

Currently, the escrow states are: Alaska, Arizona, California, Hawaii, Idaho, Nevada, New Mexico, parts of Ohio, Oregon, Utah and Washington. States that structure closings differently. You and the seller are not required to be in the same location.

An escrow agreement normally includes information such as: The identity of the appointed escrow agent. Definitions for any expressions pertinent to the agreement. The escrow funds and detailed conditions for the release of these funds.

The escrow letter is typically issued by a title company and states that all necessary documents and funds related to the transaction have been received and will be processed when the transaction is completed.