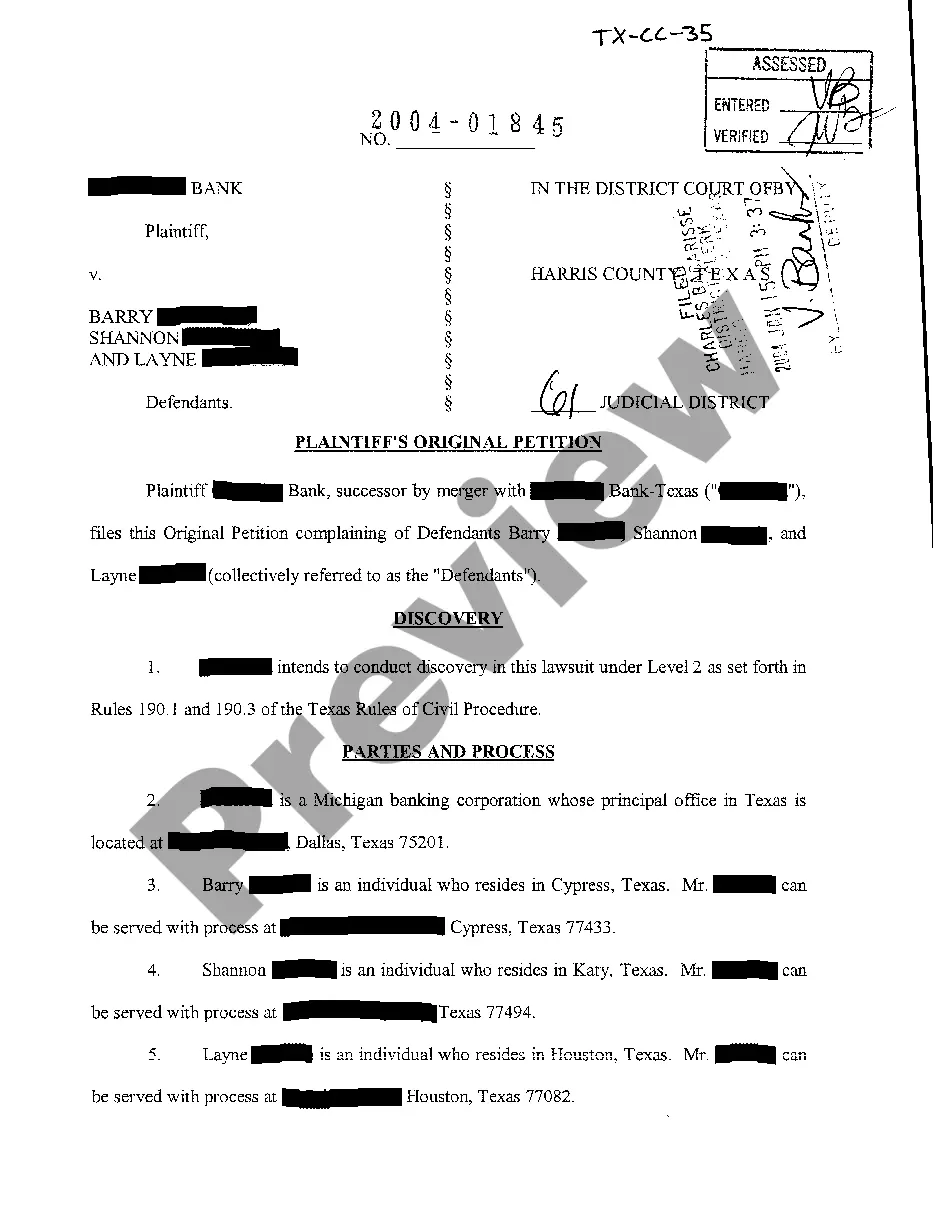

Secured Debt Shall For Loan In San Bernardino

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Are secured loans easier to get? Generally speaking, yes. Because you're usually putting your home as a guarantee for payments, the lender will see you as less of a risk, and they'll rely less on your credit history and credit score to make the judgement.

If you can't or don't want to keep paying the secured debt, you have the option to surrender the collateral. This means you give the property back to the lender, and you're no longer responsible for the debt.

Secured debt - A debt that is backed by real or personal property is a “secured” debt. A creditor whose debt is “secured” has a legal right to take the property as full or partial satisfaction of the debt. For example, most homes are burdened by a “secured debt”.

Debt Settlement Assess Financial Situation. Stop Using your Credit Cards. Negotiate with Creditors. Reach Settlement Agreements. Make Settlement Payments. Monitor Credit Reports. Rebuild Credit. Balance Transfer Credit Cards.

Debt Settlement Assess Financial Situation. Stop Using your Credit Cards. Negotiate with Creditors. Reach Settlement Agreements. Make Settlement Payments. Monitor Credit Reports. Rebuild Credit. Balance Transfer Credit Cards.

Old (Time-Barred) Debts In California, there is generally a four-year limit for filing a lawsuit to collect a debt based on a written agreement.

Restarting the Statute of Limitations: A Risk to Be Aware Of Any payment, written acknowledgment of the debt, or agreement to settle can reset the four-year clock, allowing creditors to file a lawsuit again.

Debt collectors may not be able to sue you to collect on old (time-barred) debts, but they may still try to collect on those debts. In California, there is generally a four-year limit for filing a lawsuit to collect a debt based on a written agreement.

Secured and Unsecured Debt in Investing Secured debt, backed by collateral, offers a lower risk of default; however, because the rates are often lower, your potential return will also be lower. There are also other investing things to keep in mind. For example, as mentioned earlier, secured debt may have longer terms.

Why is a Mortgage Secured Debt? A mortgage is what's called a secured debt because it is backed up by collateral. In this case, the collateral is your home.