Stockholder Meeting For Windows In Minnesota

Description

Form popularity

FAQ

A flat tax rate of 9.8 percent applies to Minnesota taxable income. Many corporations operate in more than one state. Under the U.S. Constitution, a state can legally tax only the income of a business that is “fairly apportioned” to its activity in the state.

To form an S Corporation in Minnesota, you'll need to file Articles of Incorporation with the Secretary of State. Once the corporation is established, you'll need to file IRS Form 2553 to elect S Corporation status.

Only income sourced to Minnesota is subject to this tax. The corporate franchise tax, also frequently referred to as the corporate income tax, applies to “C” corporations (i.e., corporations and some partnerships) that are taxable under subchapter “C” of the Internal Revenue Code.

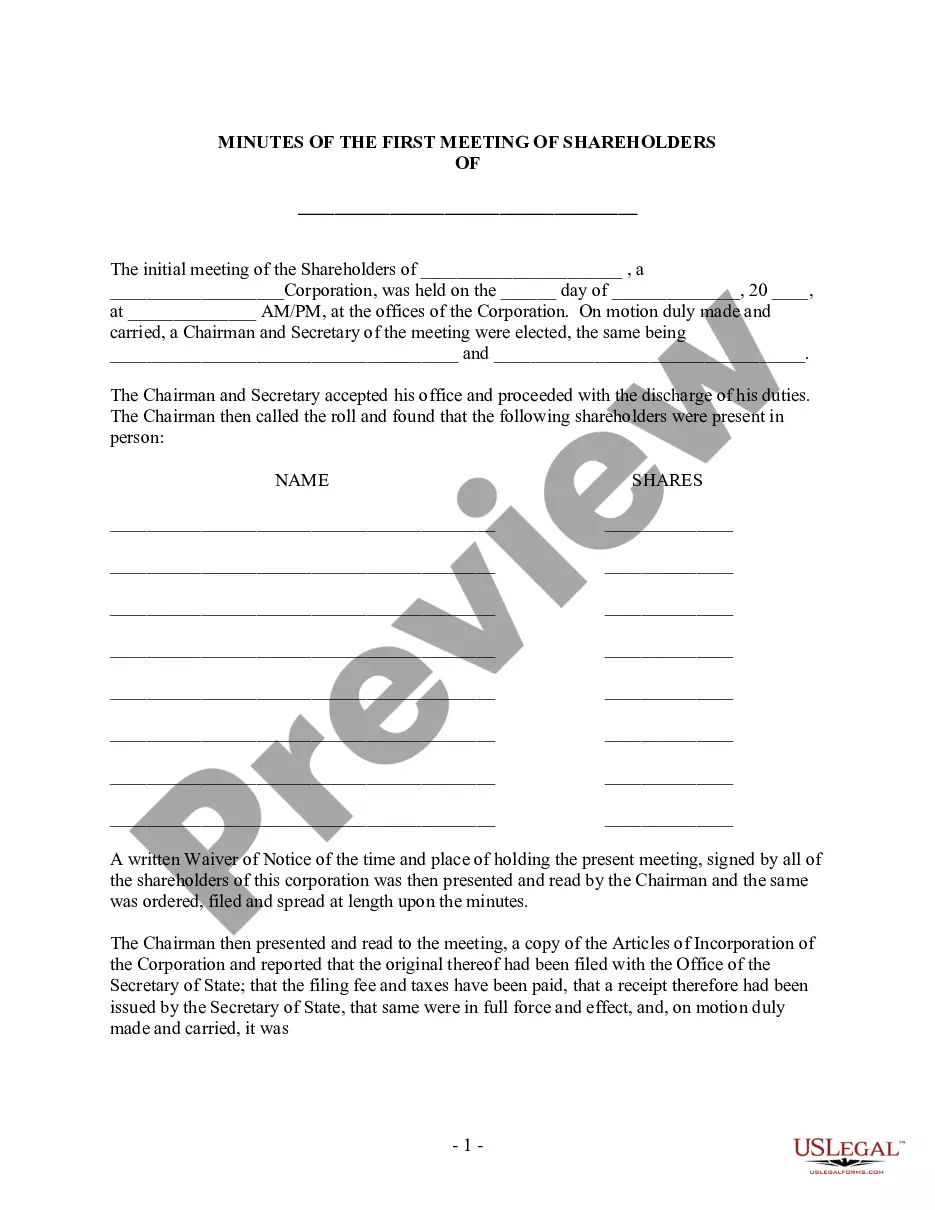

All shareholders must be notified of the format, date, time, and place of the meeting. How far in advance notices should be distributed may depend on your state, but generally, they should be sent out more than 10 days prior to the meeting, but less than 60 days.

How to Form an S Corp in Minnesota Name your Minnesota LLC. Appoint a registered agent in Minnesota. File Minnesota Articles of Organization. Create an operating agreement. Apply for an EIN. Apply for S Corp status with IRS Form 2553.

In shareholders' meetings, this means aligning the agenda with shareholder rights and interests. In board meetings, the agenda should focus on strategic and oversight matters.

LLCs and S corps are each separate business entities A corporation is formed by filing articles of incorporation with its state of incorporation. To be taxed as an S corporation it then has to file an election form with the IRS. An LLC is formed by filing articles of organization with its formation state.

What should be recorded in meeting minutes? Any actions taken (or agreed to be taken) during the meeting. Voting outcomes on proposals brought forward to the board. The outcome of motions (taken or rejected) Items to be held over to a meeting at a later date.

As the lone attendee you must document the date, time and location of the meeting. You must also list the discussion items, summarize the key points and document the decisions made. You must note all the positions in attendance, even if you occupy all of them.