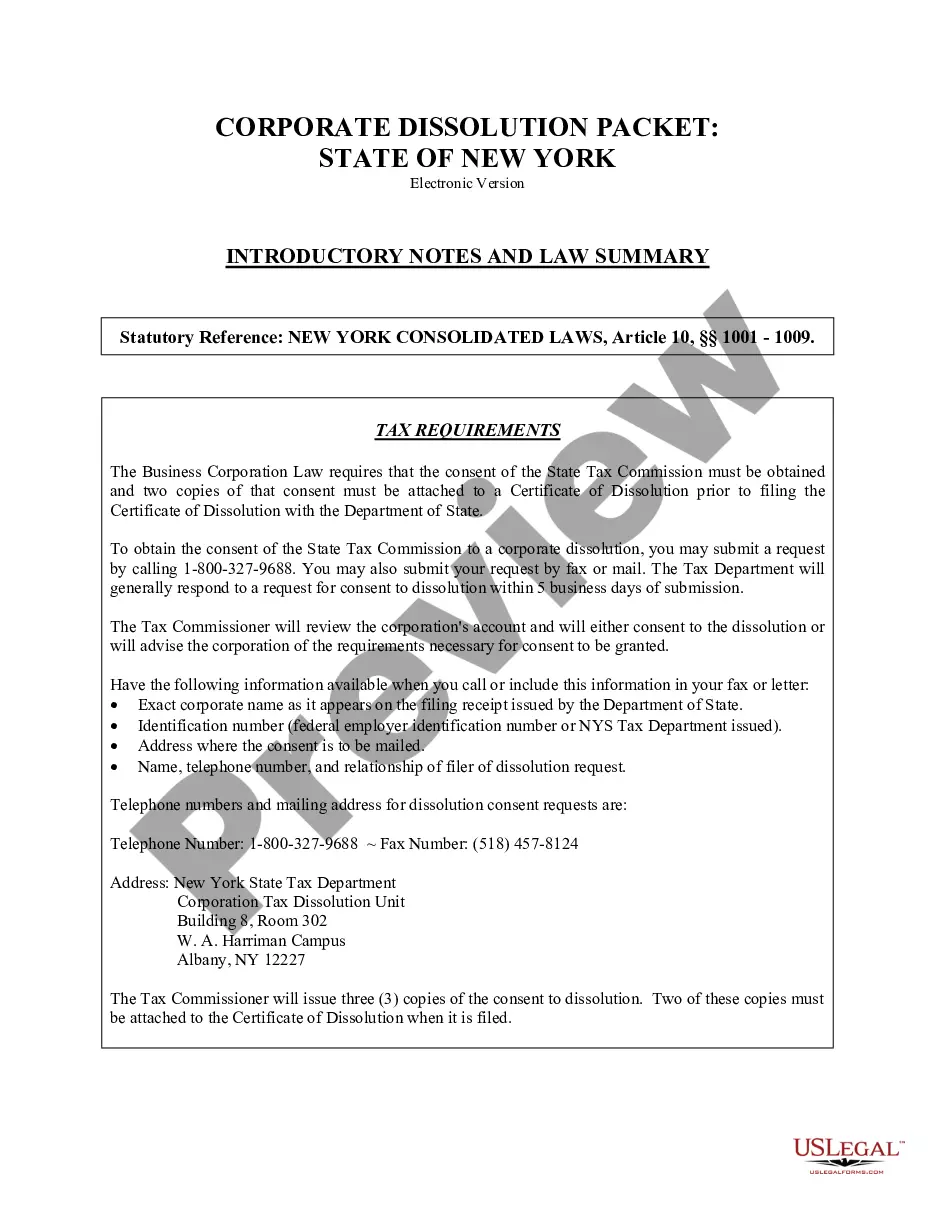

Limited Lliability

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out New York Dissolution Package To Dissolve Limited Liability Company LLC?

- Log into your US Legal Forms account if you're a returning user, ensuring your subscription is active. If it's not, renew it as per your payment plan.

- Review the available templates to find the one that precisely aligns with your needs. Utilize the Preview mode for guidance on local jurisdiction requirements.

- If you need to explore other options, use the Search tab to locate additional templates that fit your criteria.

- Select the desired document by clicking the 'Buy Now' button and choose the subscription that works best for you. Don’t forget to create an account for full access.

- Complete your purchase by entering your credit card information or using your PayPal account for a smooth transaction.

- Download the form onto your device for easy access and completion. You can also find it in the 'My Forms' section of your profile for future reference.

By utilizing US Legal Forms, you gain access to a wide selection of editable and fillable legal documents that are both comprehensive and easy to navigate.

Start your journey towards legal clarity today by exploring our extensive library of forms!

Form popularity

FAQ

Filling out an LLC is straightforward. First, gather the necessary information, such as your business name and registered agent details. Next, navigate to your state’s business filing website, where you will find the LLC application. US Legal Forms provides user-friendly templates to help you complete the application correctly, ensuring you meet all the regulatory requirements for establishing limited liability.

A limited liability company is best described as a versatile and protective business structure offering the benefits of both a corporation and a partnership. It provides owners with limited liability, allowing them to separate personal risk from business activities. Additionally, LLCs enable simplified tax treatment and flexible management, making them an ideal option for many business owners.

Limited liability protects an owner's personal assets from business debts, while unlimited liability means that the owner bears full responsibility for all obligations of the business. In simple terms, if a company with limited liability fails, only its assets are at risk. Conversely, with unlimited liability, owners risk personal financial loss, making limited liability a favorable choice for many entrepreneurs.

A limited liability company (LLC) is a unique business entity that provides its owners with protection from personal liability while allowing flexibility in management and taxation. An LLC can have one or multiple members, and it operates separately from its owners. This means that the company can incur liabilities and debts, but the personal assets of the owners typically remain protected.

Limited liability is best described as a legal principle safeguarding business owners from being personally accountable for their company’s debts. This protection encourages entrepreneurship, as individuals can innovate without the constant fear of losing their personal belongings. It empowers you to take calculated risks in your business endeavors.

Limited liability refers to the legal distinction between the owner's personal assets and the liabilities of the business. This means that if the business faces legal issues or debts, only the assets of the company are at risk. Owners can protect their personal wealth, giving them peace of mind as they run their operations.

An LLC is best suited for small to medium-sized businesses seeking liability protection and flexibility. This structure allows owners to choose how they want to be taxed, whether as a corporation or a pass-through entity. Additionally, LLCs are relatively easy to establish and maintain, making them a smart choice for new business owners.

A limited liability company, or LLC, is a business structure that combines the benefits of a corporation with those of a sole proprietorship or partnership. It offers limited liability protection to its owners, meaning they are not personally liable for the company's debts or liabilities. This legal protection makes LLCs an attractive choice for many entrepreneurs seeking security while running their businesses.

Limited liability protects business owners from personal responsibility for business debts. For instance, if a limited liability company (LLC) incurs debt, creditors cannot pursue the owner's personal assets. This means your home, car, and savings remain safe, allowing you to focus on growing your business without fear of losing everything.

You can elect to have your LLC taxed as a corporation, allowing for separate tax filings under Form 1120. This choice gives your business its own tax obligations, which may provide strategic benefits. However, it will also increase your filing complexity and associated costs. To understand your best options for maintaining limited liability and tax efficiency, consult with a tax advisor or explore resources available through US Legal Forms.