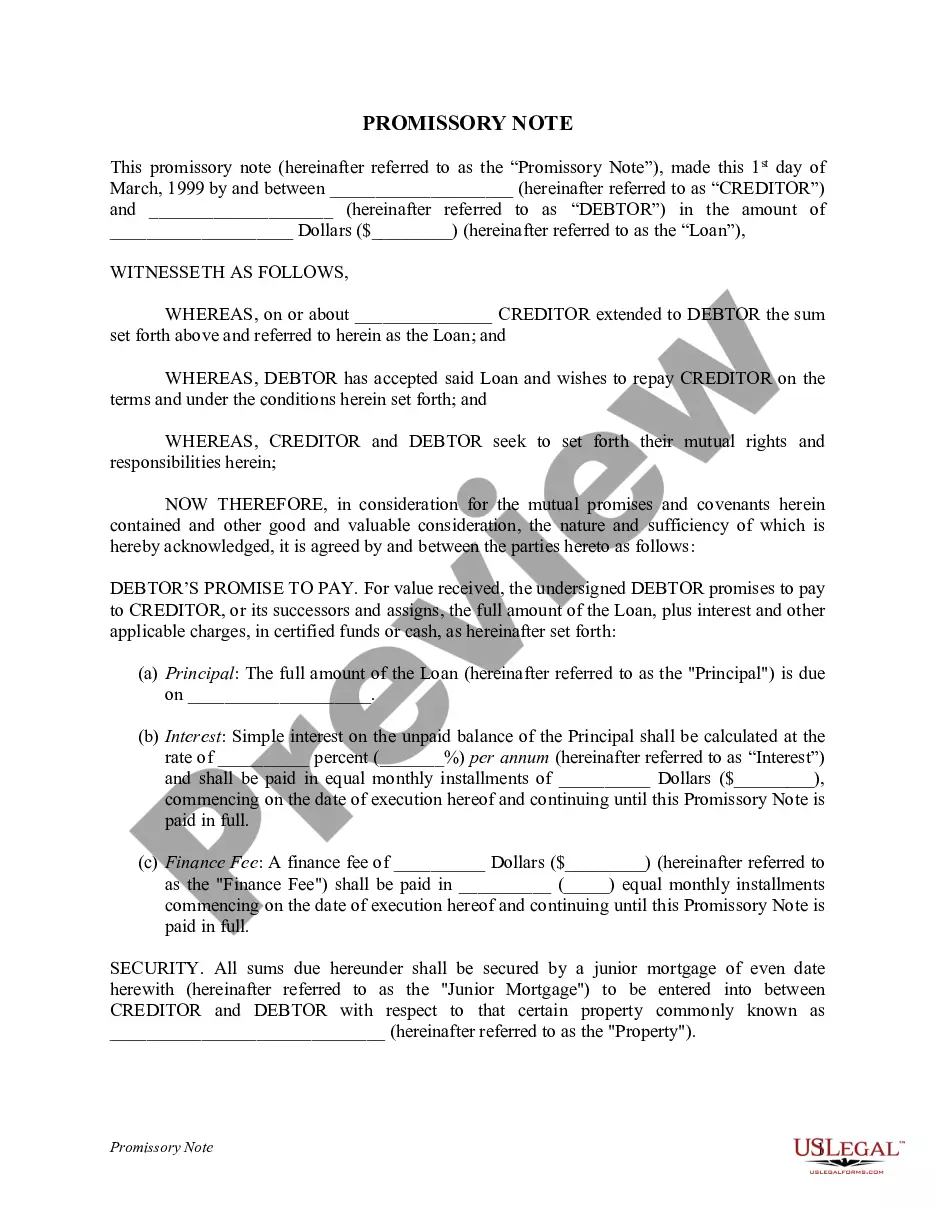

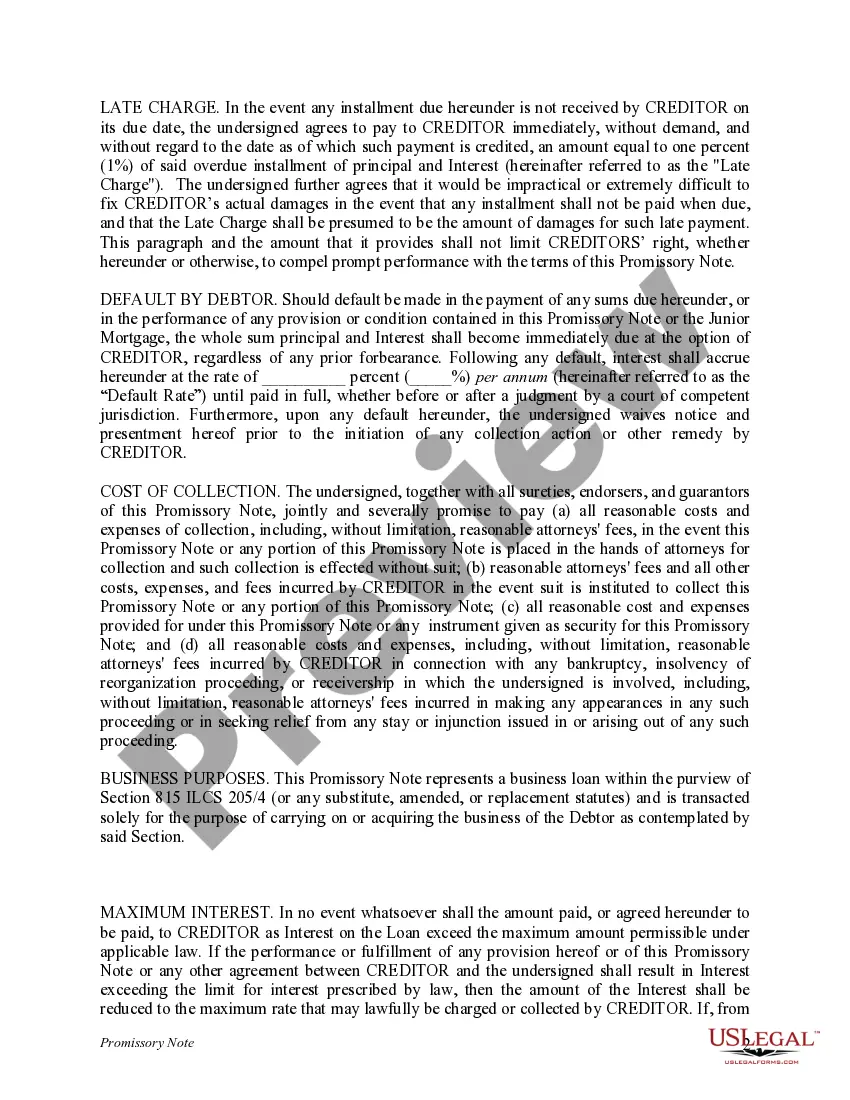

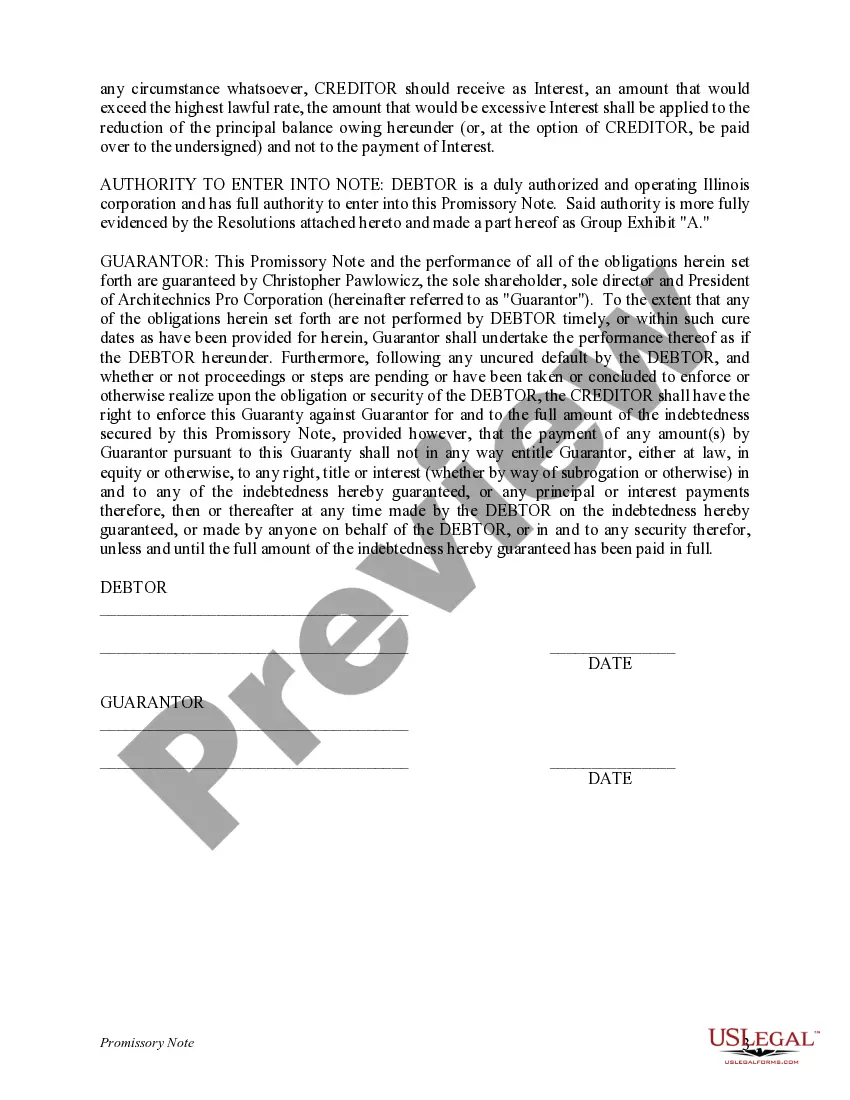

A promissory note is a legally binding document that outlines a promise made by one party, known as the "maker," to repay a debt owed to another party, known as the "payee." It serves as a written agreement containing specific terms and conditions regarding the repayment, including the amount owed, interest rate, installment schedule, and any other agreed-upon terms. Promissory notes are commonly used in various financial transactions, such as loans, mortgages, and business deals. They provide protection for both parties involved and help establish a clear repayment structure. Here are some examples of different types of promissory notes: 1. Simple Promissory Note: A simple promissory note is the most basic form and typically involves a straightforward loan between individuals, such as friends or family members. It includes essential information like the principal amount borrowed, interest rate (if any), repayment terms, and the date the note was created. Example: John agrees to lend Sarah $5,000, with an interest rate of 5%, payable in monthly installments of $200 over a period of 2 years. They document these terms in a simple promissory note. 2. Secured Promissory Note: A secured promissory note includes an added layer of security for the lender. It involves collateral provided by the borrower to guarantee repayment. If the borrower defaults, the lender can seize and sell the collateral to recover the debt. Example: A bank lends David $50,000 to purchase a car, with the car serving as collateral. David signs a secured promissory note, agreeing to repay the loan in monthly installments over five years. If he defaults, the bank has the right to repossess and sell the car to satisfy the debt. 3. Fixed-Rate Promissory Note: A fixed-rate promissory note sets a specific interest rate that remains unchanged throughout the repayment period. This type of note provides certainty for both the borrower and the lender regarding the interest payments. Example: Jane borrows $10,000 from a financial institution with a fixed interest rate of 7% per annum. The terms state that she will repay the loan in equal monthly installments of $250 over a period of five years, based on this fixed interest rate. 4. Demand Promissory Note: A demand promissory note allows the lender to demand full repayment at any time without specifying a specific repayment schedule or term. This type of note is often used in situations where the lender requires flexibility in collecting the debt. Example: Mark borrows $20,000 from his friend Lisa and signs a demand promissory note. Lisa has the right to request full repayment at her discretion, providing her with the flexibility to collect the debt when necessary. In conclusion, promissory notes provide a legally binding agreement between two parties regarding a debt repayment. These notes come in various types, including simple, secured, fixed-rate, and demand promissory notes, each serving different purposes depending on the specific transaction and requirements. They help establish clear repayment terms, protect the interests of both parties, and ensure transparency in financial agreements.

Promissory Note With Example

Description

How to fill out Promissory Note With Example?

The Promissory Note With Example you see on this page is a reusable formal template drafted by professional lawyers in compliance with federal and regional laws and regulations. For more than 25 years, US Legal Forms has provided individuals, companies, and attorneys with more than 85,000 verified, state-specific forms for any business and personal scenario. It’s the quickest, most straightforward and most trustworthy way to obtain the paperwork you need, as the service guarantees the highest level of data security and anti-malware protection.

Acquiring this Promissory Note With Example will take you just a few simple steps:

- Search for the document you need and review it. Look through the file you searched and preview it or check the form description to verify it satisfies your requirements. If it does not, make use of the search option to get the correct one. Click Buy Now once you have found the template you need.

- Sign up and log in. Choose the pricing plan that suits you and register for an account. Use PayPal or a credit card to make a quick payment. If you already have an account, log in and check your subscription to continue.

- Get the fillable template. Select the format you want for your Promissory Note With Example (PDF, Word, RTF) and download the sample on your device.

- Complete and sign the paperwork. Print out the template to complete it by hand. Alternatively, use an online multi-functional PDF editor to quickly and precisely fill out and sign your form with a valid.

- Download your papers again. Utilize the same document again whenever needed. Open the My Forms tab in your profile to redownload any previously saved forms.

Sign up for US Legal Forms to have verified legal templates for all of life’s circumstances at your disposal.

Form popularity

FAQ

Raising Rent ? Landlords in Louisiana may increase the rent to any amount with no notice or justification. Notice of Entry ? Louisiana does not require any notice before entering the unit or property. Repairs ? It is the landlord's responsibility to keep the rental in safe and healthy living conditions.

Louisiana tenants have the right to live in a property that meets fair housing requirements, as well as the right to due process if the landlord decides to file an eviction claim. If any damages in the property exceed normal wear and tear, Louisiana tenants may send a written notice to the landlord for a fix.

You can sue your landlord when: Your landlord discriminates against you. Your landlord takes your security deposit illegally. Your rental unit is inhabitable. The property owner interferes with your right to quiet enjoyment. Your landlord fails to make the necessary repairs.

The rental agreement is an official contract entered between the tenant and owner of a property. Tenant is the person who wishes to take temporary possession of the owner's property by paying the rental amount. The tenant can stay/use the property of the owner for the time mentioned in the rental agreement.

Rental Application Fee Law StateFeeLouisianaNo limitationsMaineFee must not exceed the actual cost of the screening.MarylandNo limitationsMassachusettsOnly a licensed broker can charge an application fee (MA G.L. c 186 § 15B(b)).46 more rows ?

Landlords are responsible for giving the tenant the promised property on time and in good, working and safe condition. The property should be maintained in a condition that suits the tenant and should be kept safe. Any damages that provide a danger to the tenant and their family should be attended to immediately.

Louisiana is considered a landlord-friendly state due to its lack of rent control laws. The state also prohibits cities and towns from creating rent control laws. This means landlords can ask for whatever rent amount they see fit.

A Louisiana month-to-month rental agreement, known as a ?tenancy-at-will,? enables both the landlord and the tenant to continue under the lease arrangement until a party cancels. The minimum time period in Louisiana is 10 days' notice for terminating a month-to-month lease.