Title Review For Heloc

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

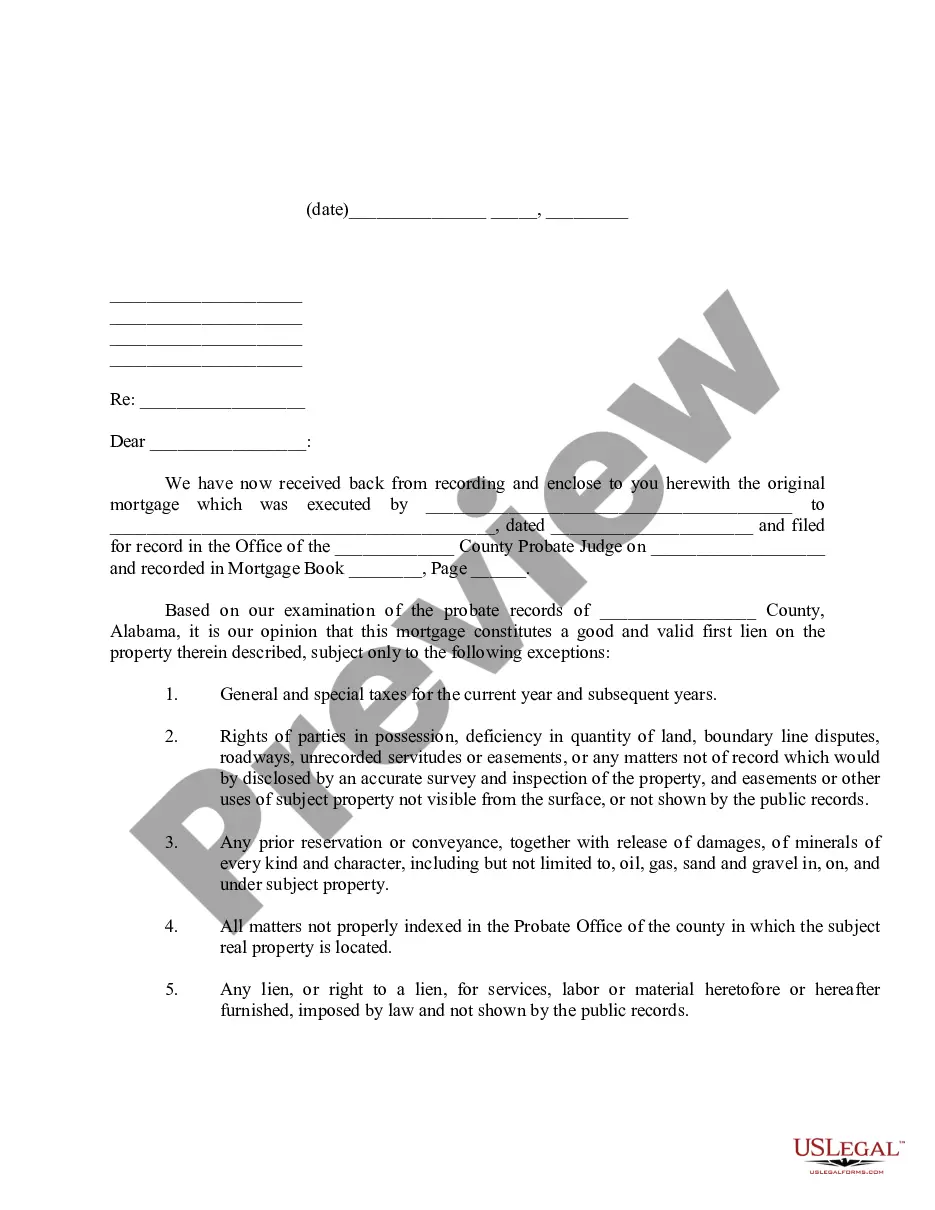

How to fill out Alabama Title Opinion Letter - Preliminary?

The Title Review For Heloc you observe on this page is a versatile legal template crafted by skilled attorneys in accordance with federal and state laws.

For over 25 years, US Legal Forms has delivered individuals, organizations, and lawyers with more than 85,000 validated, state-specific documents for any business and personal situation. It’s the quickest, easiest, and most reliable method to acquire the forms you require, as the service assures bank-level data protection and anti-malware safeguards.

Fill out and sign the documents. Print the template to complete it manually. Alternatively, use an online multi-functional PDF editor to quickly and accurately fill out and sign your form with an eSignature. Download your documents again. Use the same document again whenever necessary. Open the My documents tab in your profile to redownload any previously purchased forms. Subscribe to US Legal Forms to have verified legal templates for all of life’s situations at your fingertips.

- Search for the document you require and evaluate it.

- Examine the file you sought and preview it or check the form description to confirm it meets your needs. If it does not, utilize the search bar to find the appropriate one. Click Buy Now once you have located the template you need.

- Select and Log In.

- Pick the pricing option that fits you and create an account. Use PayPal or a credit card to make a swift payment. If you already possess an account, Log In and verify your subscription to continue.

- Obtain the fillable template.

- Select the format you desire for your Title Review For Heloc (PDF, DOCX, RTF) and download the document onto your device.

Form popularity

FAQ

The HELOC appraisal process evaluates your home's condition, contrasts it with similar recently-sold properties, and considers any unique features or upgrades your home may have.

signer applies for the home loan right along with you. However, they are not on the title of the home. The cosigners name is only on the loan, meaning that while they are financially responsible for paying back the mortgage, they do not have ownership of the property.

The approval process can take anywhere from 2-6 weeks or even longer, depending on your situation. See below for factors that affect your timeline.

Lenders typically look at your home equity, your loan-to-value ratio, your debt-to-income ratio, and your credit score before they decide whether or not you qualify for a home equity line of credit. These numbers can also affect the interest rate they might offer you on a HELOC.

To qualify for a HELOC, you need to have available equity in your home, meaning that the amount you owe on your home must be less than the value of your home. You can typically borrow up to 85% of the value of your home minus the amount you owe.