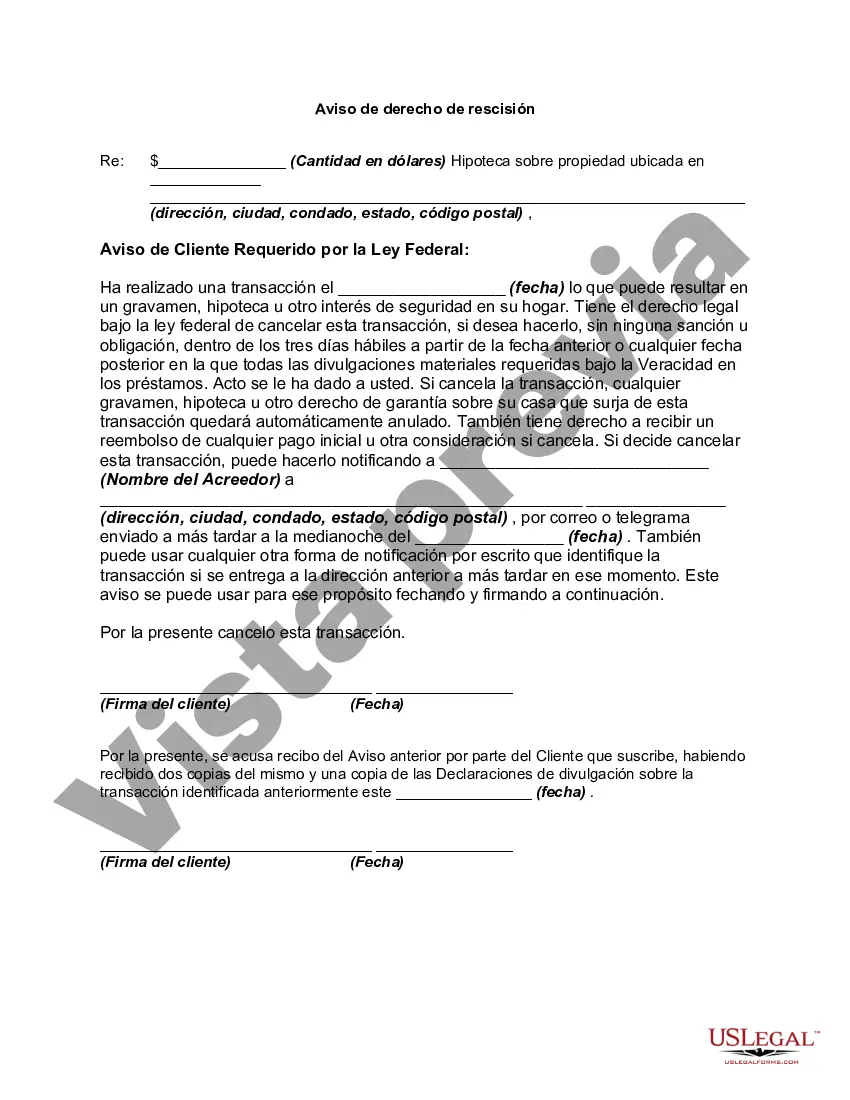

In a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership is or will be subject to the security interest has the right to rescind the transaction. Lenders are required to deliver two copies of the notice of the right to rescind and one copy of the disclosure statement to each consumer entitled to rescind. The notice must be on a separate document that identifies the rescission period on the transaction and must clearly and conspicuously:

" disclose the retention or acquisition of a security interest in the consumer's principal dwelling;

" the consumer's right to rescind the transaction; and

" how the consumer may exercise the right to rescind with a form for that purpose.

Idaho Right to Rescind When Security Interest in Consumer's Principal Dwelling is Involved — Rescission: A Detailed Description In Idaho, the Right to Rescind when a security interest in a consumer's principal dwelling is involved refers to the legal ability for homeowners to cancel or "rescind" specific types of contracts or loans, securing their residential property. There are different scenarios where the Right to Rescind can come into play when dealing with a security interest in a consumer's principal dwelling. Let's explore each of them in detail: 1. Mortgage Loans: When homeowners secure a mortgage loan using their primary residence as collateral, they are granted a specific period, known as the "right of rescission," to cancel or rescind the loan. Generally, Idaho law allows homeowners to exercise their right to rescind a mortgage loan within three business days after the loan closing, or until midnight of the third business day after the delivery of the loan disclosures and notice of the right to rescind, whichever occurs later. 2. Home Equity Loans and Lines of Credit: Similar to mortgage loans, homeowners who obtain home equity loans or lines of credit that are secured by their principal dwelling also have the right to rescind within the same timeframe of three business days after closing or after receiving the loan disclosures and notice of the right to rescind. It's essential for consumers to understand that the right to rescind is designed to protect their interests, allowing them to make informed decisions and evaluate their financial commitments before being bound by a security interest in their residential property. To exercise the right to rescind, homeowners must provide written notice to the lender or creditor expressing their intention to cancel the transaction. The notice should include the borrower's name, address, and the loan details. It is advisable to send the notice via certified mail to ensure a documented delivery acknowledgment. Upon timely receipt of the notice, the lender or creditor is legally obligated to take necessary actions to terminate the security interest in the consumer's principal dwelling. This may involve returning any payments made by the consumer and releasing any liens or encumbrances placed on the residential property. Failure by the lender or creditor to adhere to the consumer's right to rescind can have severe consequences, potentially rendering the loan or security interest voidable and exposing the lender to statutory penalties. In summary, the Idaho Right to Rescind When Security Interest in Consumer's Principal Dwelling is Involved grants homeowners the legal right to cancel or rescind certain contracts or loans secured by their residential property. Whether it involves mortgage loans or home equity loans, understanding this important consumer protection provides homeowners with the ability to make informed and financially responsible decisions regarding their most significant asset — their home.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.