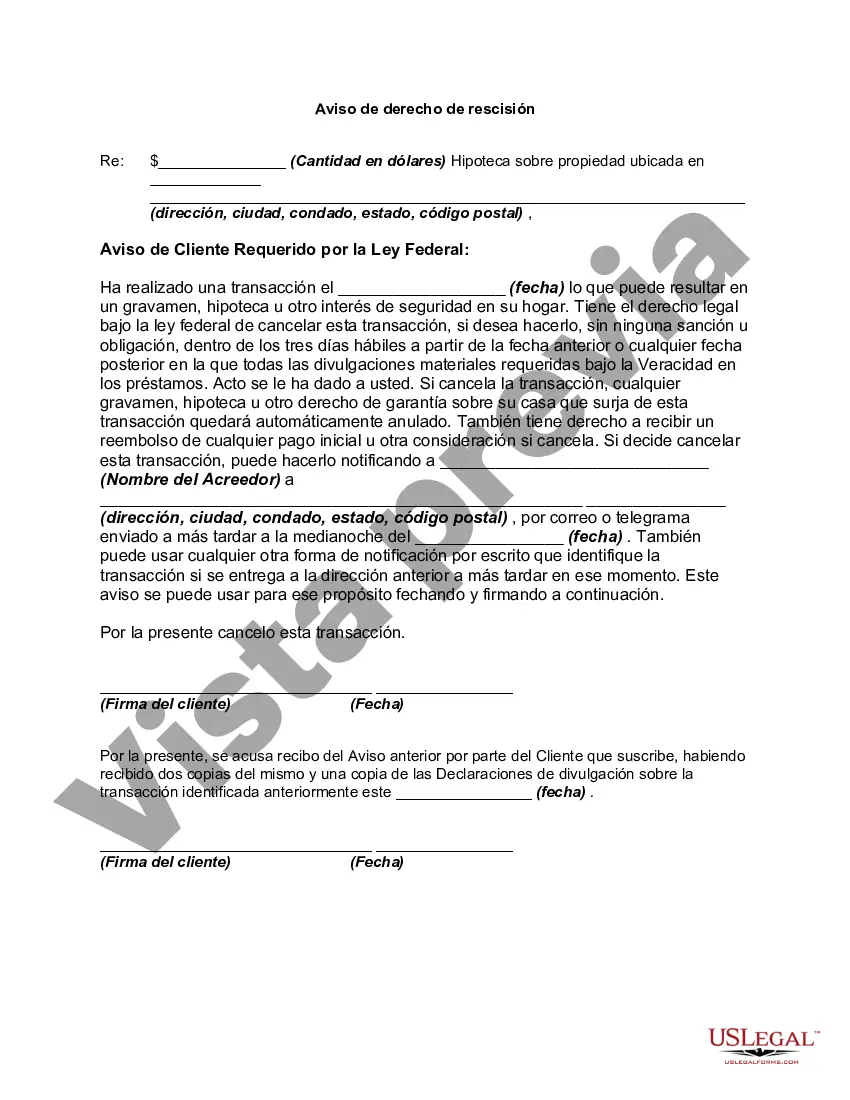

In a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership is or will be subject to the security interest has the right to rescind the transaction. Lenders are required to deliver two copies of the notice of the right to rescind and one copy of the disclosure statement to each consumer entitled to rescind. The notice must be on a separate document that identifies the rescission period on the transaction and must clearly and conspicuously:

" disclose the retention or acquisition of a security interest in the consumer's principal dwelling;

" the consumer's right to rescind the transaction; and

" how the consumer may exercise the right to rescind with a form for that purpose.

The California Right to Rescind when a Security Interest in a Consumer's Principal Dwelling is Involved — Rescission is a legal provision that grants consumers the right to cancel certain types of mortgage loans or home equity lines of credit. This right is established under federal law, specifically the Truth in Lending Act (TILL) and it's implementing regulation, Regulation Z. When a security interest, such as a mortgage or lien, is attached to a consumer's primary residence in California, the right to rescind allows the borrower to undo the transaction within a specified time frame. The purpose of this right is to offer consumer protection and provide an opportunity to reconsider and potentially avoid unfavorable loan terms or agreements. The general rule for the California Right to Rescind is that the consumer has three business days to exercise the right after the loan closing or receiving the Truth in Lending disclosures, whichever occurs later. However, there are certain scenarios where the right to rescind can extend beyond the initial three-day period: 1. Material Disclosures Not Provided: If the lender fails to provide all the required material disclosures or necessary documents, the right to rescind may extend to three years from the loan closing date. 2. Inaccurate Disclosures: If the lender provides inaccurate or misleading disclosures, the borrower has three years from the date of loan closing to exercise the right to rescind. 3. Change in Terms: If the loan terms change significantly after the closing, the consumer may have three years to rescind from the date of the change. It's important to note that the California Right to Rescind applies only to loans secured by the consumer's principal dwelling. This typically includes mortgages, home equity lines of credit, and other loans involving the primary residence. In order to exercise the right to rescind, the consumer must provide a written notice of rescission to the lender within the specified time frame. Upon receiving the notice, the lender must then take the necessary steps to unwind the loan transaction. This typically involves returning any fees or payments made by the consumer and releasing the security interest attached to the property. In conclusion, the California Right to Rescind when a security interest in a consumer's principal dwelling is involved — Rescission is a crucial legal provision that safeguards borrowers' interests and provides an opportunity to undo certain types of mortgage loans or home equity lines of credit. Consumers should be aware of their rights and consult legal professionals if they believe their lender has violated any disclosure requirements or if they wish to exercise their right to rescind within the allowed time frames.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.