Installment Note In Accounting

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Promissory Note With Installment Payments?

The Installment Note In Accounting presented on this page is a reusable legal document crafted by expert attorneys in compliance with national and local regulations.

For over 25 years, US Legal Forms has supplied individuals, businesses, and lawyers with more than 85,000 authenticated, state-specific documents for any commercial and personal circumstance. It’s the quickest, easiest, and most dependable way to acquire the paperwork you require, as the service guarantees bank-grade data security and anti-malware safeguards.

Subscribe to US Legal Forms to access verified legal templates for all of life's situations at your fingertips.

- Browse for the document you desire and review it.

- Sign up and Log In.

- Acquire the editable template.

- Fill out and sign the document.

- Download your papers one more time.

Form popularity

FAQ

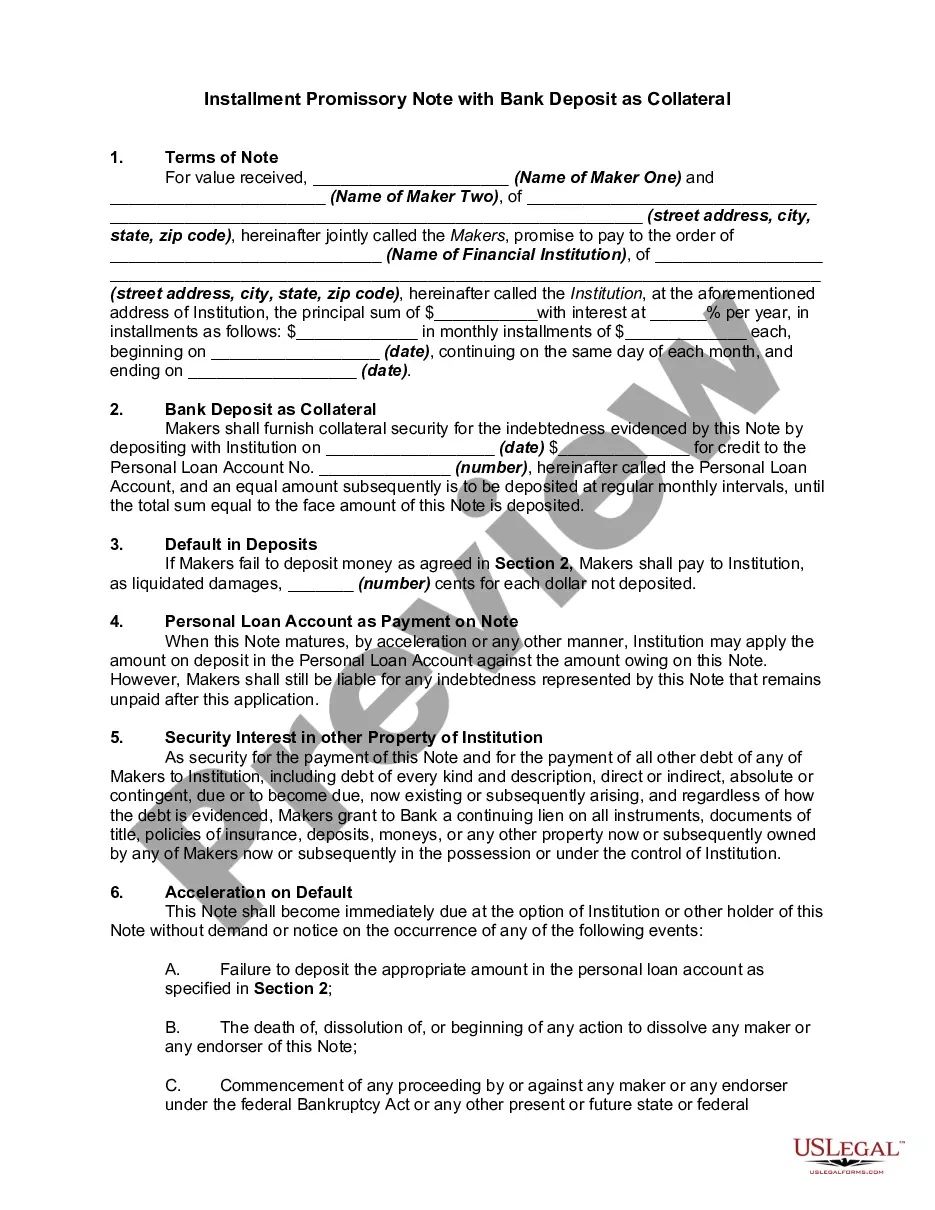

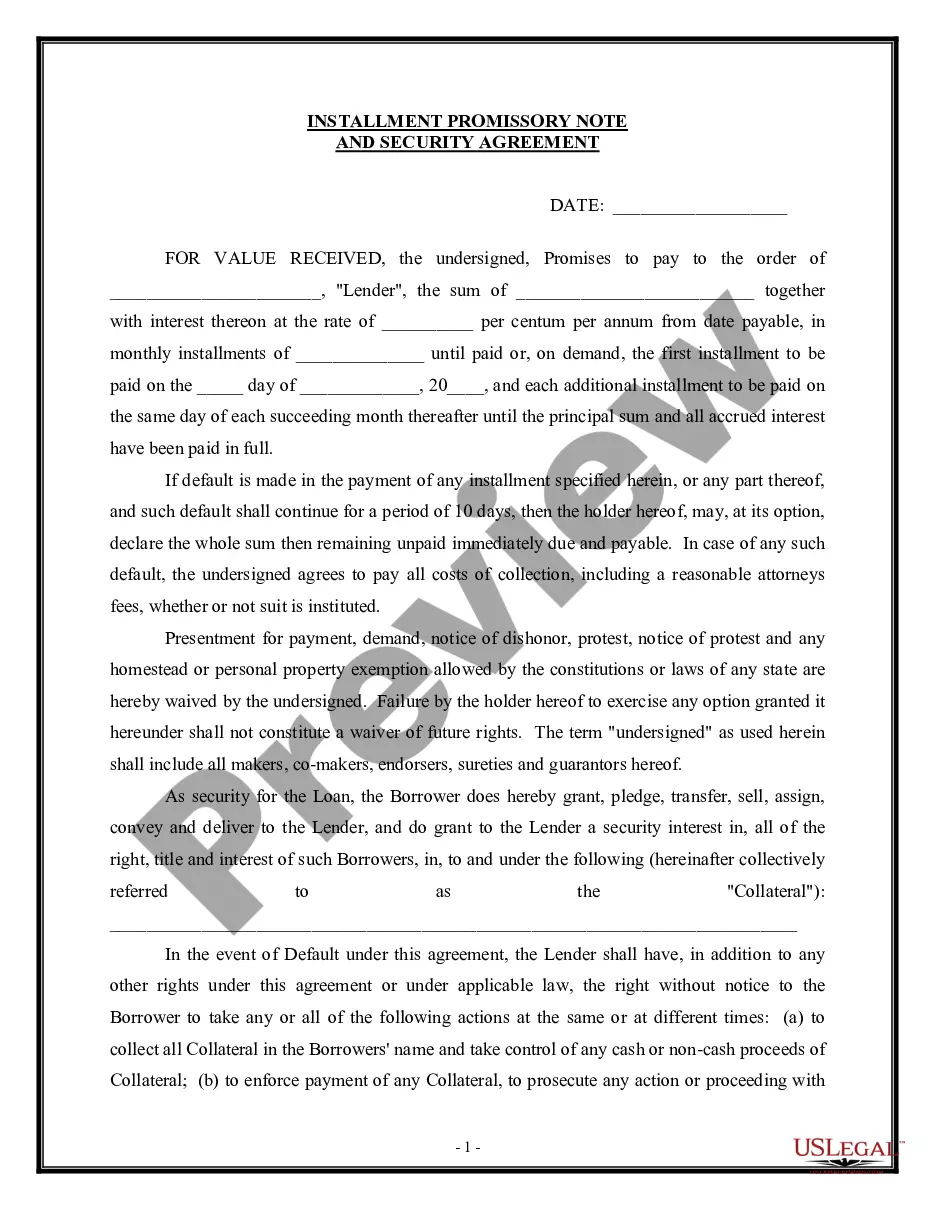

An installment note requires payments of both principal and interest over time, while a straight note involves only interest payments initially. With an installment note in accounting, you gradually reduce the principal as you make payments, which provides a clear understanding of your outstanding liability. In contrast, a straight note requires a lump sum payment of principal at maturity. Understanding these differences helps in selecting the right type of note for your financial strategy.

An installment note is recorded just like a single payment note when the note is acquired. The cash is debited at the acquisition of the note and the installment note payable is credited. The same entry (with the corresponding amount) is made for each period.

Mortgages and car loans are common examples of installment notes, as both involve equal payments across the life of the loan that could be 5 years for a car and 30 years for a mortgage.

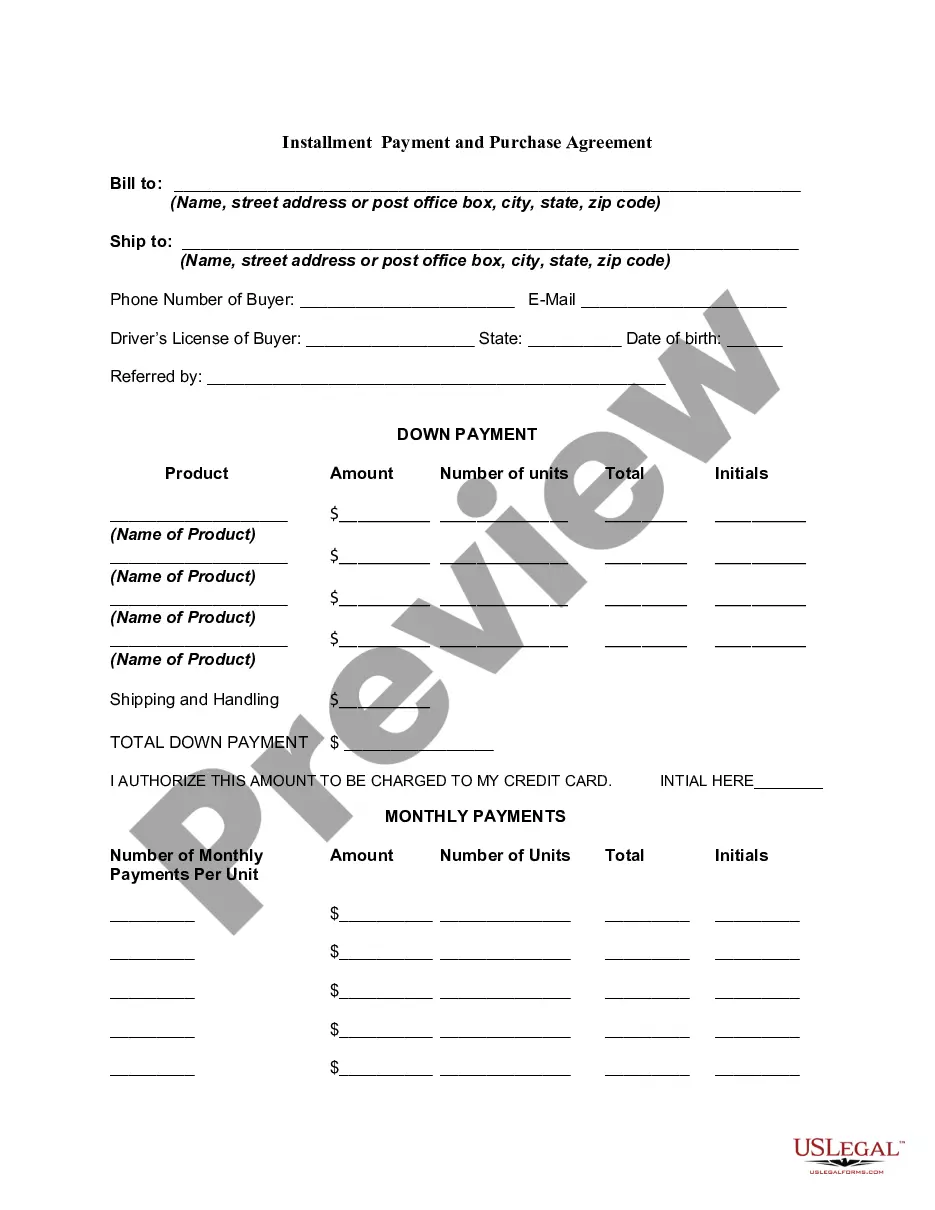

An installment note is a loan agreement that allows a borrower to pay back a debt in regular payments, or installments, over a period of time. It usually involves a lender and a borrower, with the terms of repayment stated in writing. The note is signed by both parties to confirm the loan agreement and its terms.

As you repay the loan, you'll record notes payable as a debit journal entry, while crediting the cash account. This is recorded on the balance sheet as a liability. But you must also work out the interest percentage after making a payment, recording this figure in the interest expense and interest payable accounts.