Collateral agreements for banks play a critical role in the lending process, offering security and mitigating risk for both borrowers and lenders. These agreements serve as legal contracts between the borrower and the bank, outlining the terms and conditions related to the collateral pledged as security for a loan. Collateral refers to assets or property that a borrower offers as security, which the bank can seize in the event of default or non-payment. There are various types of collateral agreements commonly used by banks to protect their interests. These may include: 1. Mortgage Collateral Agreements: In mortgage agreements, real estate properties, such as residential or commercial properties, are used as collateral. These agreements outline the terms specific to property valuation, foreclosure processes, and any additional requirements related to property maintenance and insurance. 2. Pledge of Stocks or Securities: Banks may also accept stocks, bonds, or other valuable securities as collateral. These agreements specify the types of securities accepted, their valuation, and procedures for the bank to sell or liquidate the collateral in case of default. 3. Asset-Based Collateral Agreements: These agreements involve pledging specific business assets, such as equipment, inventory, accounts receivable, or intellectual property rights, as collateral. The agreements outline the valuation, monitoring, and release processes for these collateral types. 4. Cash Collateral Agreements: In some cases, banks may accept cash or cash equivalents as collateral, especially for short-term loans or certain financial transactions. These agreements establish the terms for holding and releasing the cash collateral, including any associated interest or fees. 5. Personal Guarantees: While not strictly collateral agreements, personal guarantees are often used in conjunction with collateral. In these agreements, individuals (often business owners) pledge personal assets, such as houses, vehicles, or savings accounts, as additional security for a loan. These guarantees provide an extra layer of protection for the bank. Collateral agreements for banks are essential to ensure the lending process remains secure and minimize potential losses. The terms and conditions specified in these agreements protect the interests of both parties involved, establishing clear guidelines for the management, valuation, and potential sale of collateral assets. It is crucial for borrowers to fully understand the terms of the collateral agreement and seek legal advice if necessary, to ensure a smooth lending experience and mitigate any potential risks.

Collateral Agreement

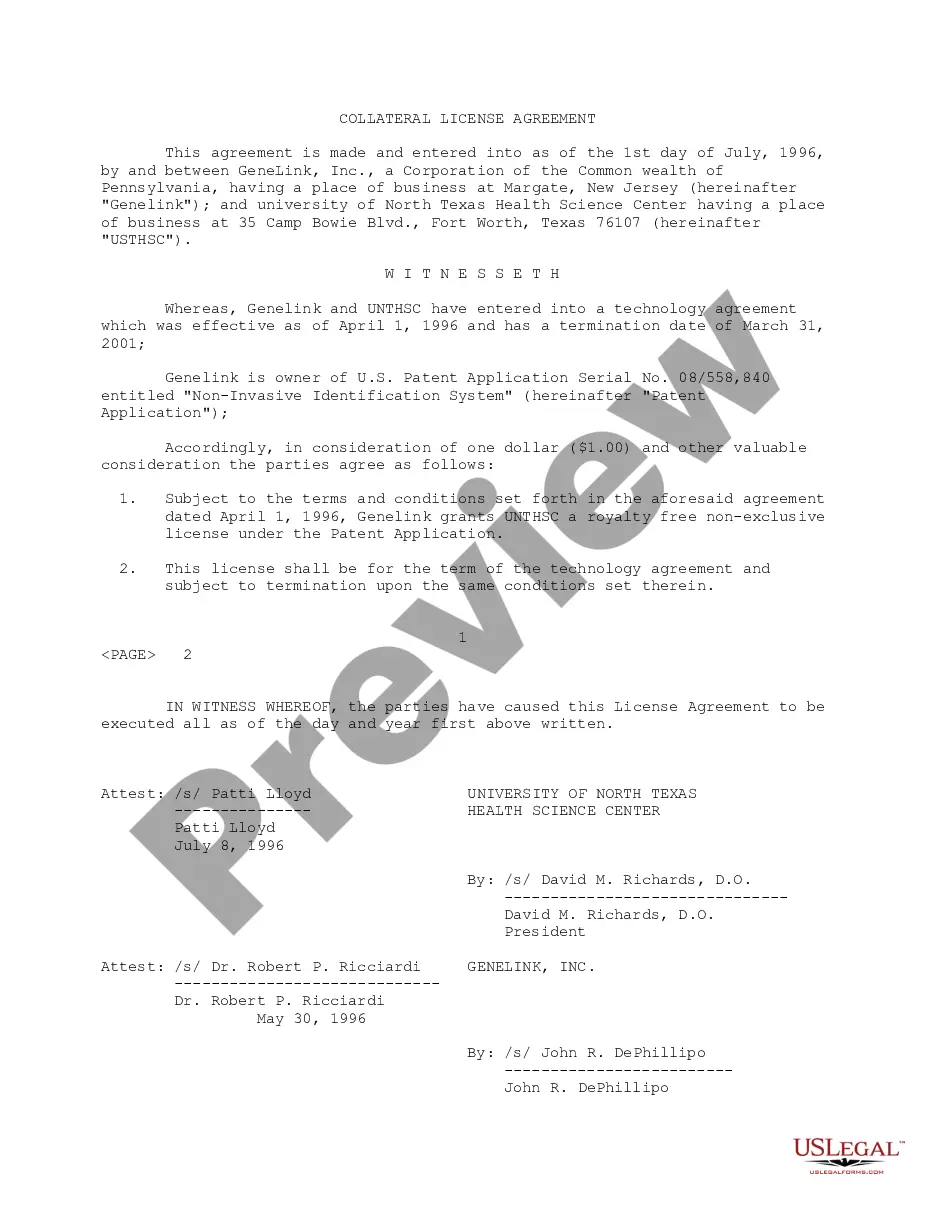

Description License Agreement Form Template

How to fill out Collateral License Agreement Between GeneLink, Inc. And The University Of North Texas Health Science Center?

When it comes to drafting a legal document, it is easier to leave it to the experts. However, that doesn't mean you yourself can not get a template to use. That doesn't mean you yourself can not get a template to utilize, however. Download Collateral License Agreement between GeneLink, Inc. and The University of North Texas Health Science Center straight from the US Legal Forms web site. It gives you numerous professionally drafted and lawyer-approved forms and samples.

For full access to 85,000 legal and tax forms, customers simply have to sign up and choose a subscription. When you’re registered with an account, log in, search for a certain document template, and save it to My Forms or download it to your device.

To make things less difficult, we have incorporated an 8-step how-to guide for finding and downloading Collateral License Agreement between GeneLink, Inc. and The University of North Texas Health Science Center quickly:

- Make sure the form meets all the necessary state requirements.

- If possible preview it and read the description before purchasing it.

- Click Buy Now.

- Select the suitable subscription to suit your needs.

- Create your account.

- Pay via PayPal or by debit/bank card.

- Choose a preferred format if a number of options are available (e.g., PDF or Word).

- Download the file.

As soon as the Collateral License Agreement between GeneLink, Inc. and The University of North Texas Health Science Center is downloaded you can fill out, print out and sign it in any editor or by hand. Get professionally drafted state-relevant files in a matter of seconds in a preferable format with US Legal Forms!