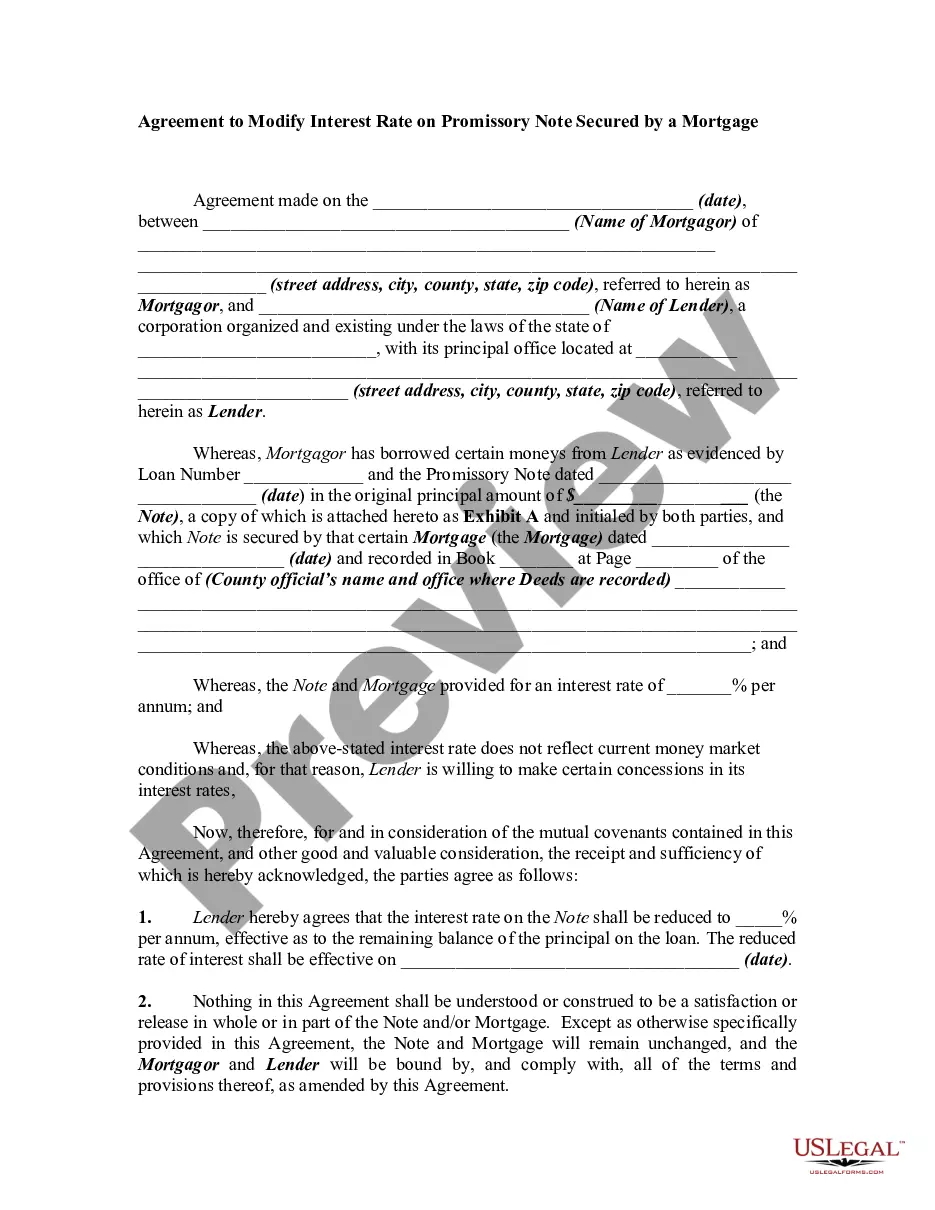

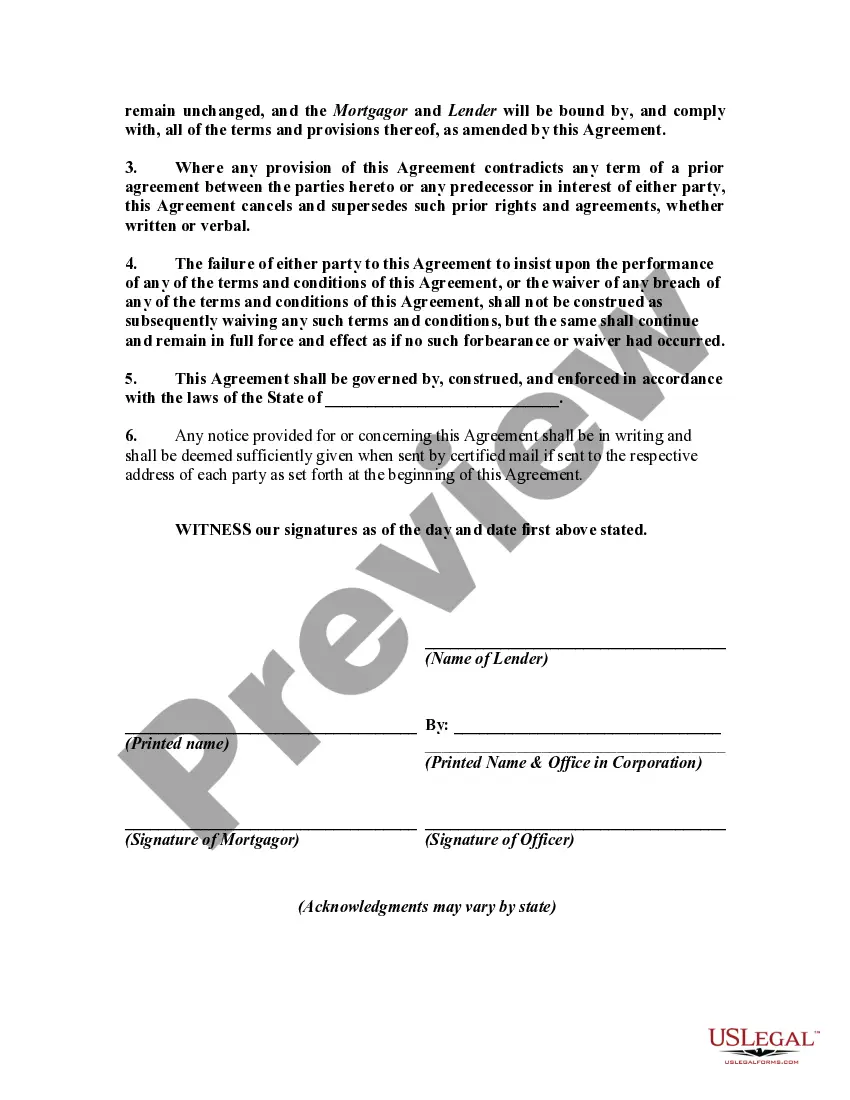

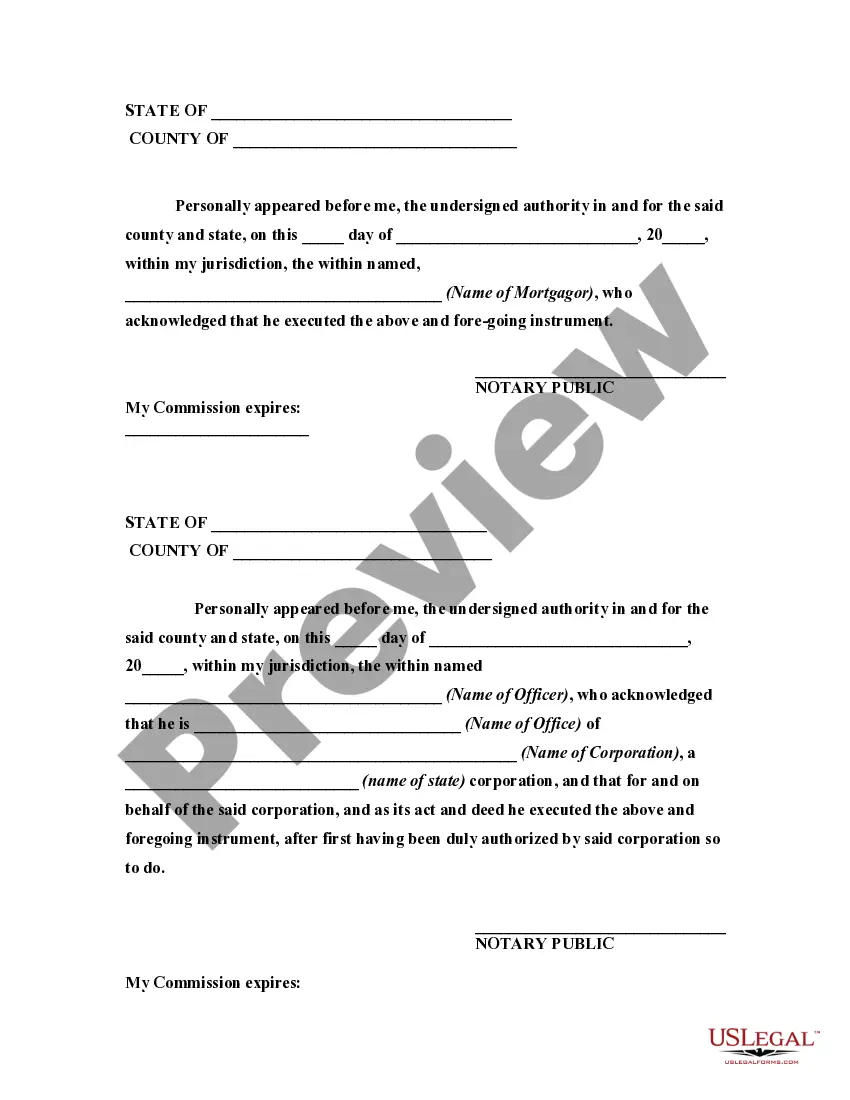

An agreement modifying a loan agreement and mortgage should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original mortgage was recorded. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Modify by mortgage with bad credit refers to the process of making changes to an existing mortgage agreement despite having a poor credit history. This option is typically available for homeowners who are struggling to meet their mortgage payments and need to modify the terms of their loan in order to make it more affordable. Having bad credit can make it challenging to find favorable loan terms or secure new financing. However, homeowners in this situation still have options through modifying their mortgage. There are several types of modifications available, including: 1. Loan Term Extension: This modification involves extending the payment period of the mortgage loan. By increasing the loan term, the monthly payments can be reduced, making it more affordable for homeowners with bad credit. However, it's important to note that this may result in paying more interest over the life of the loan. 2. Interest Rate Reduction: With this type of modification, the lender agrees to lower the interest rate on the existing mortgage. This results in reduced monthly payments, making it easier for homeowners with bad credit to manage their finances. Lower interest rates can save homeowners a significant amount of money over time. 3. Principal Forbearance: In some cases, lenders may offer principal forbearance as a modification option. This involves temporarily reducing or suspending the principal repayments, helping homeowners struggling with bad credit to alleviate the financial burden. However, it's crucial to understand that the suspended principal amount will still need to be repaid eventually. 4. Loan Modification Programs: There are various government-backed loan modification programs available for homeowners with bad credit. These programs, such as the Home Affordable Modification Program (CAMP), aim to help borrowers facing financial hardships by providing assistance with modifying their existing mortgage terms. 5. Refinancing with Cash-Out: While not strictly a modification, refinancing with a cash-out option can be a viable solution for homeowners with bad credit. By refinancing their mortgage, homeowners can tap into their home equity and receive a cash sum. This cash can then be used to pay off existing debts or make necessary home improvements, easing financial strain. When considering any modification option, it's vital for homeowners to assess the potential impact on their credit score, as well as thoroughly understand the terms and conditions offered by the lender. Seeking professional advice from mortgage experts or credit counselors can provide valuable guidance throughout the modification process and help homeowners make informed decisions. In summary, Modify by mortgage with bad credit allows struggling homeowners to make changes to their existing mortgage terms to alleviate financial difficulties. Loan term extension, interest rate reduction, principal forbearance, loan modification programs, and refinancing with cash-out are key modification options available to those with bad credit.