Deficiency balance letters are issued by lenders or creditors to inform borrowers about the remaining amount owed after the sale of a repossessed or foreclosed asset. These letters explain that the borrower's outstanding debt, also known as the deficiency balance, has been forgiven. This process typically occurs when the asset's sale does not generate enough funds to cover the full loan amount. The primary purpose of a deficiency balance letter is to inform borrowers about the resolution of their outstanding debt. These letters can provide relief to borrowers who struggle with financial burdens, as the forgiven debt is no longer their responsibility. This forgiveness eliminates the need for further repayment and often comes after negotiations or agreements between the borrower and the lender. Different types of deficiency balance letters forgiven include: 1. Mortgage Deficiency Balance Forgiveness: This type of deficiency balance letter applies to borrowers who faced foreclosure due to defaulting on their mortgage. The forgiven debt usually arises when the proceeds from the foreclosure sale are less than the outstanding loan amount. Lenders may choose to forgive the remaining balance, removing the borrower's obligation to repay it. 2. Auto Loan Deficiency Balance Forgiveness: When a vehicle is repossessed due to non-payment or default on an auto loan, the lender may sell the vehicle through auction or private sale. If the proceeds fall short of the outstanding balance, the lender may forgive the deficiency balance, relieving the borrower from further repayment obligations. 3. Credit Card or Personal Loan Deficiency Balance Forgiveness: In cases where borrowers default on credit card payments or personal loans, creditors may opt to forgive the remaining balance as a gesture of goodwill or as part of a negotiated settlement. This type of deficiency balance forgiveness can provide significant relief to borrowers burdened with unmanageable debt. 4. Business Loan Deficiency Balance Forgiveness: Small business owners who face financial challenges may default on their business loans, leading to repossession or liquidation of assets. If the resulting sale does not cover the outstanding loan amount, the lender may choose to forgive the deficiency balance, absolving the borrower of further liability. In conclusion, deficiency balance letters forgiven are issued by lenders to inform borrowers that the remaining balance on their debt has been forgiven. This forgiveness can occur in various scenarios such as mortgage defaults, auto loan repossessions, credit card or personal loan defaults, and business loan defaults. The letters provide relief to borrowers by absolving them of further repayment obligations and allowing them to start afresh financially.

Deficiency Balance Letter

Description Auto Deficiency Letter

How to fill out Deficiency Letter?

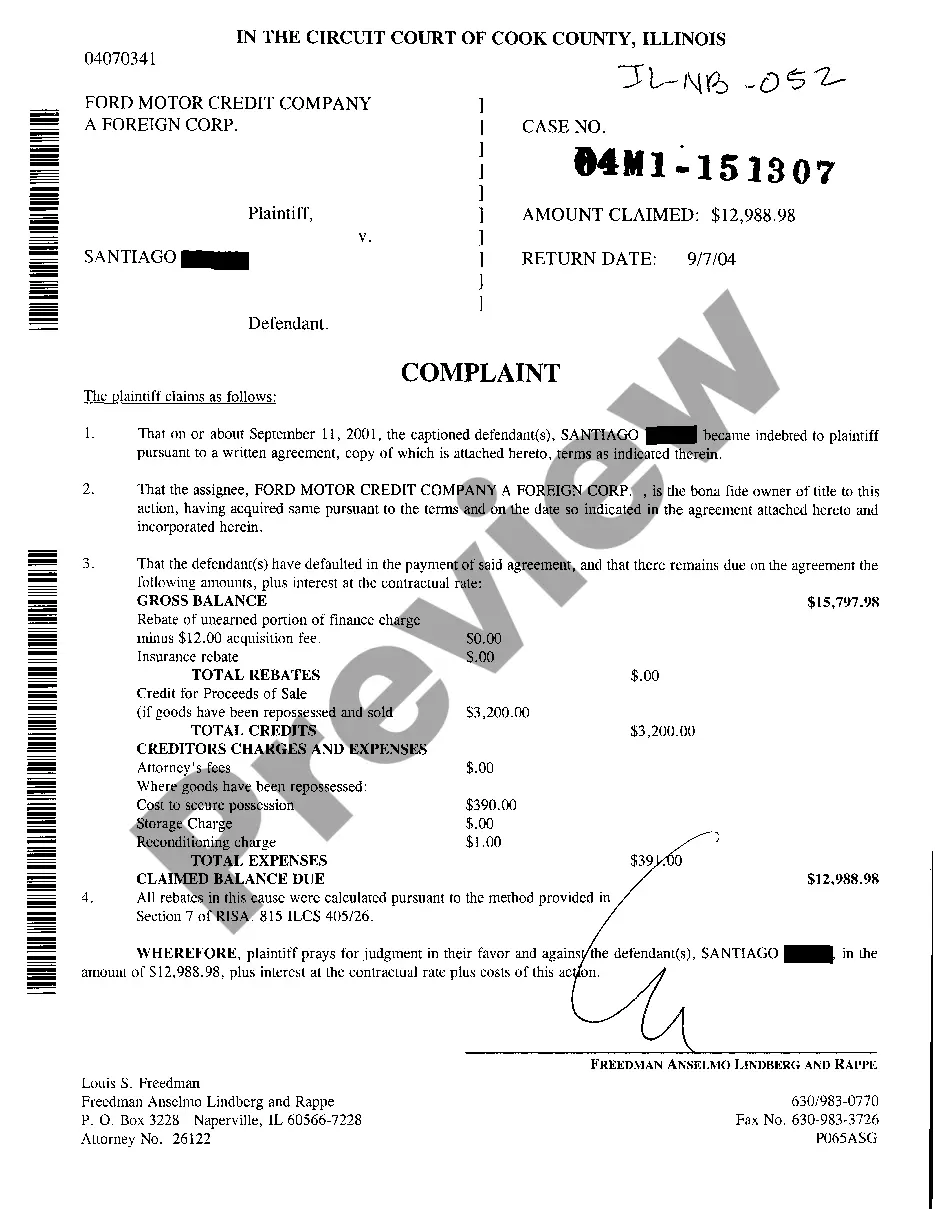

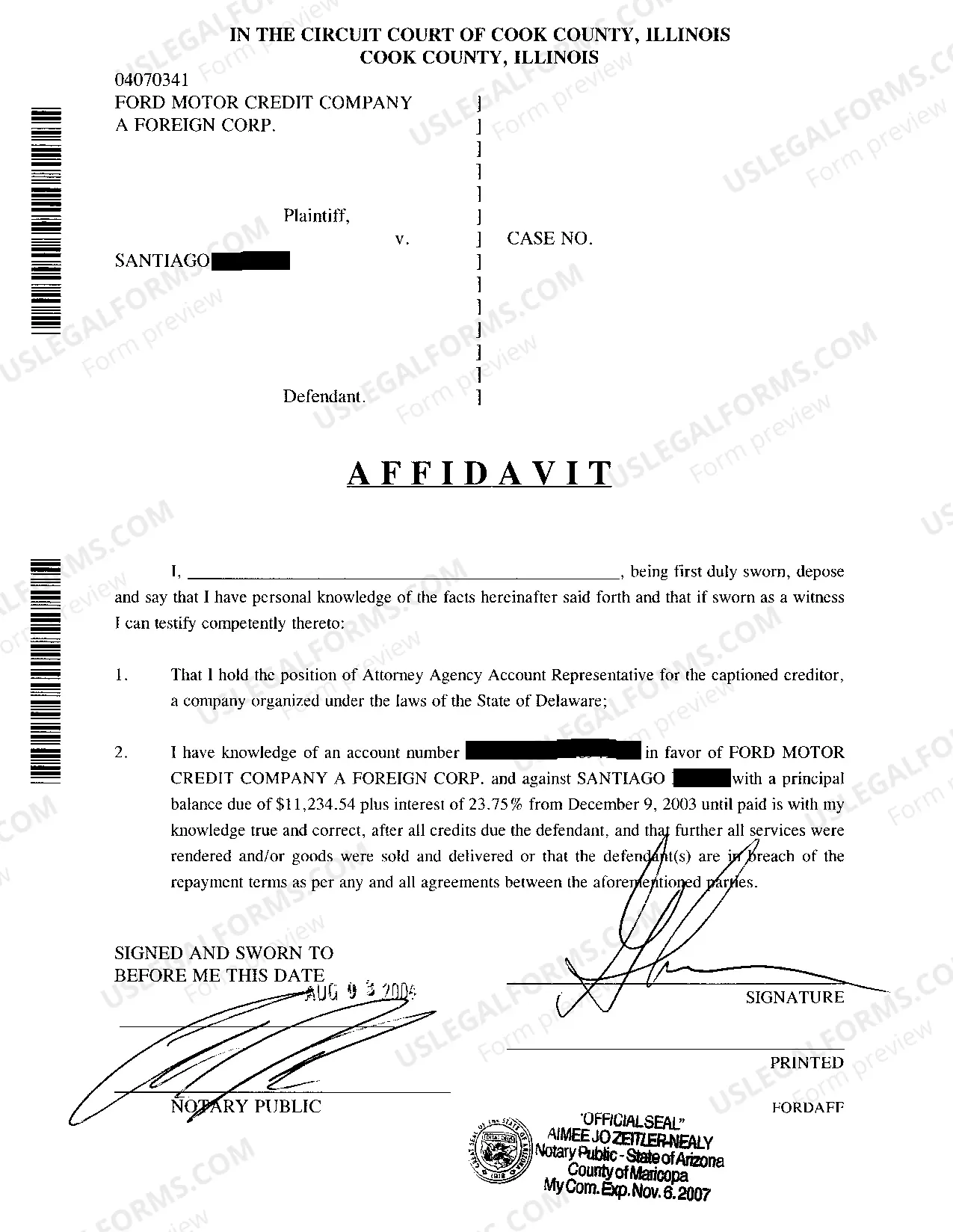

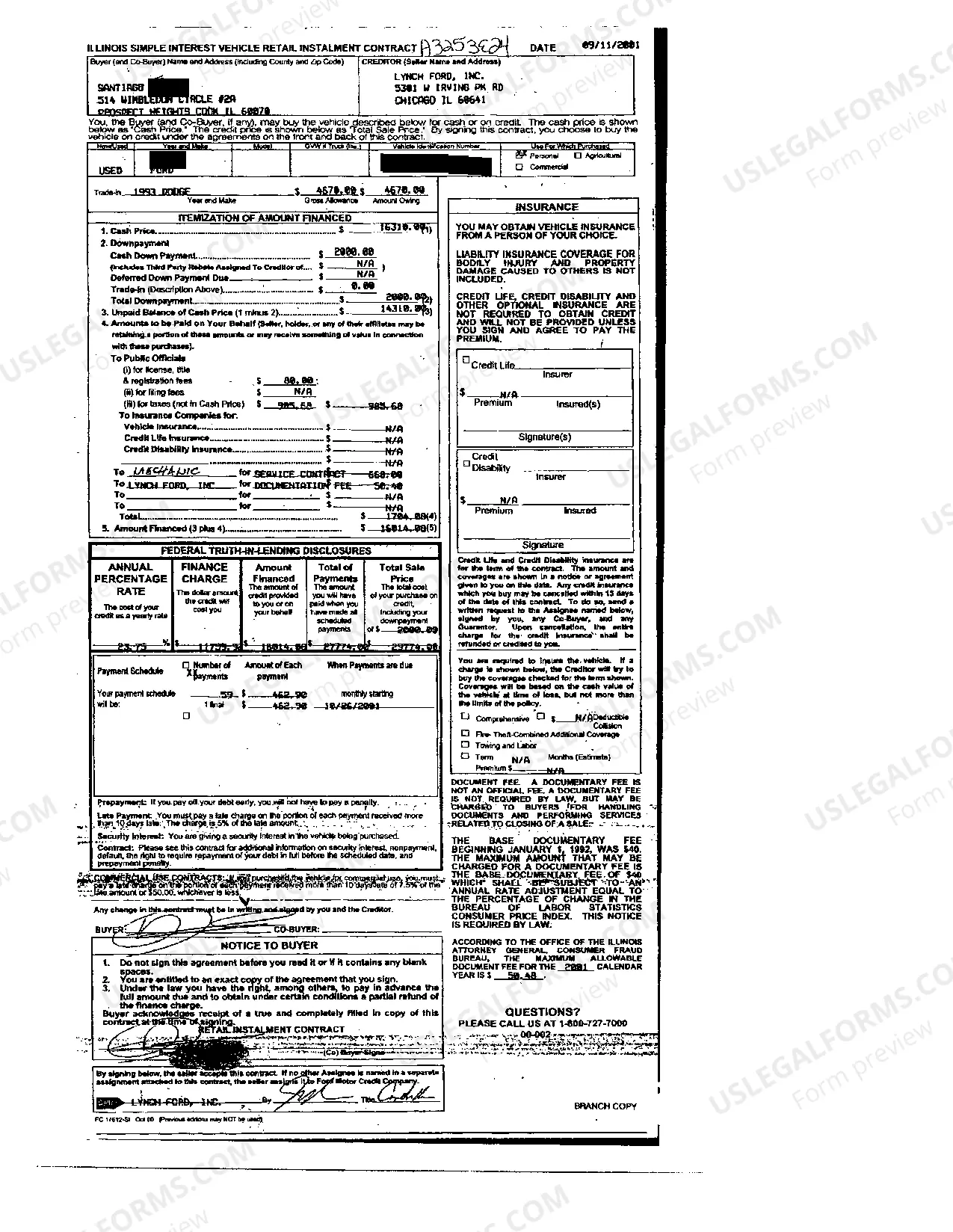

In search of Illinois Complaint to Collect Deficiency Balance after Repossession Sale of Automobile forms and completing them might be a problem. To save lots of time, costs and energy, use US Legal Forms and find the right sample specifically for your state in just a couple of clicks. Our attorneys draft every document, so you just have to fill them out. It truly is that simple.

Log in to your account and return to the form's page and download the sample. Your downloaded templates are saved in My Forms and they are available at all times for further use later. If you haven’t subscribed yet, you have to register.

Check out our detailed instructions concerning how to get your Illinois Complaint to Collect Deficiency Balance after Repossession Sale of Automobile template in a few minutes:

- To get an qualified example, check its validity for your state.

- Have a look at the example making use of the Preview function (if it’s available).

- If there's a description, read it to understand the specifics.

- Click Buy Now if you found what you're looking for.

- Pick your plan on the pricing page and create your account.

- Choose you would like to pay out with a credit card or by PayPal.

- Download the file in the favored file format.

You can print the Illinois Complaint to Collect Deficiency Balance after Repossession Sale of Automobile template or fill it out making use of any online editor. No need to concern yourself with making typos because your template can be applied and sent, and published as often as you wish. Try out US Legal Forms and access to above 85,000 state-specific legal and tax files.