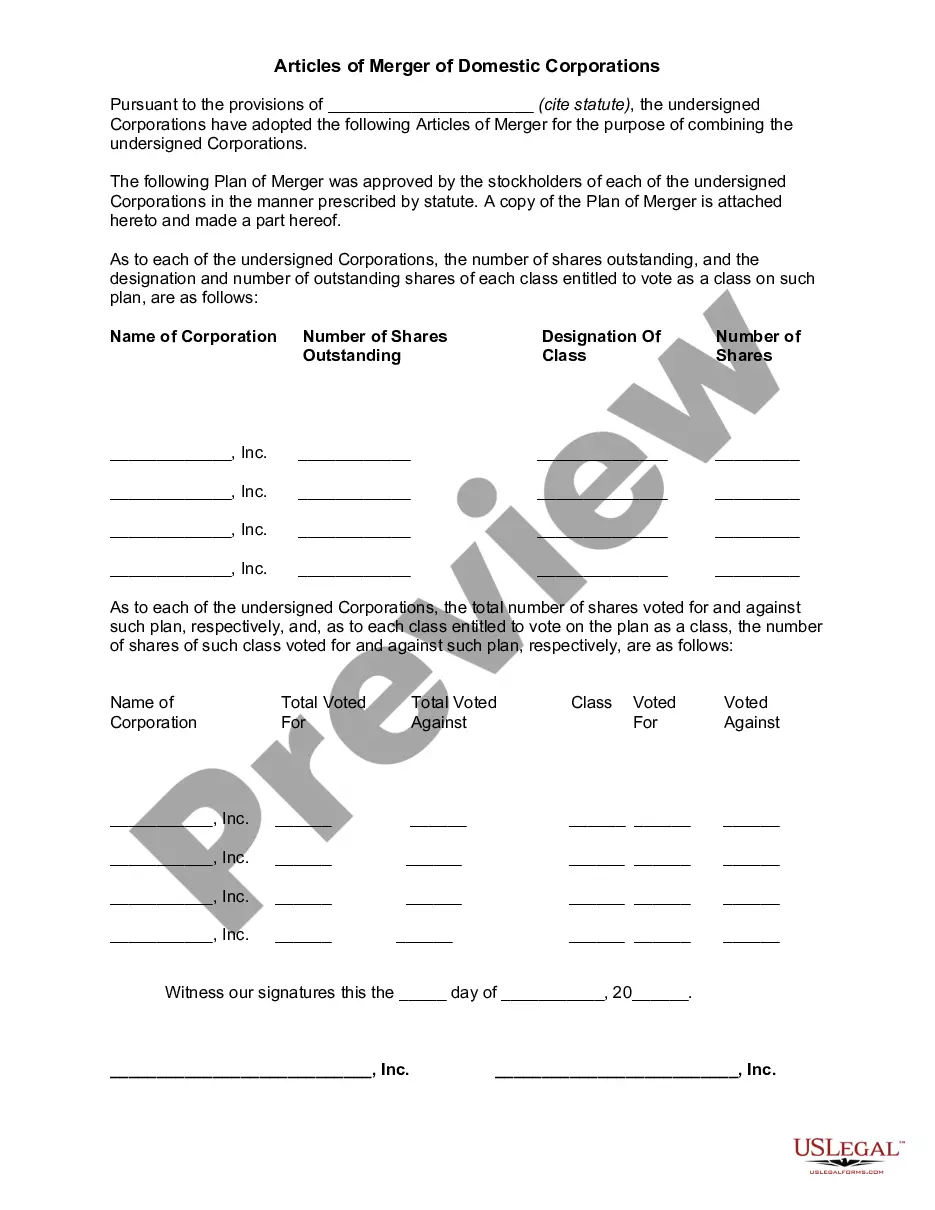

Statutes of the particular jurisdiction may require that merging corporations file copies of the proposed plan of combination with a state official or agency. Generally, information as to voting rights of classes of stock, number of shares outstanding, and results of any voting are required to be included, and there may be special requirements for the merger or consolidation of domestic and foreign corporations.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Title: Domestic Corporation vs Foreign Corporation: Understanding the Key Differences Introduction: When talking about corporations, two commonly used terms are domestic corporation and foreign corporation. While both types refer to legally recognized business entities, they differ in their formation, location, and various legal aspects. This article aims to provide a detailed description of the dissimilarities between domestic and foreign corporations, along with insights into different types of each. 1. Domestic Corporation: A domestic corporation is a term used to describe a company that is incorporated and operates within the borders of a particular country. It is organized and governed under the laws and regulations of that country. Key characteristics and features of a domestic corporation include: a. Formation and Registration: Domestic corporations are established by filing the necessary legal documents, such as Articles of Incorporation, with the relevant government agency of the country where the company will operate. These corporations have a legal presence and are granted all the rights and obligations within that jurisdiction. b. Governance and Compliance: Domestic corporations are subject to the laws and regulations of their home country, including taxation, corporate governance rules, reporting requirements, and other legal formalities. They are governed by a board of directors and must comply with domestic corporate laws. c. Liability and Taxation: Domestic corporations generally have limited liability, meaning the owners (shareholders) are not personally responsible for the company's debts and obligations. Moreover, they are subject to domestic taxation laws, paying taxes according to the country's tax rates and regulations. 2. Foreign Corporation: A foreign corporation, on the other hand, refers to a company that is formed and operates in one country but conducts business activities within another country. The essential aspects of foreign corporations include: a. Foreign Qualification: To operate in a foreign country, a foreign corporation must apply for foreign qualification or incorporation in that particular jurisdiction. This involves registering with the appropriate regulatory agency and complying with local laws and authorities. b. Limited Operations: Foreign corporations are restricted to conducting certain activities, typically outlined in their foreign qualification application. These activities may include sales, marketing, manufacturing, or other operations necessary for conducting business within the foreign jurisdiction. c. Double Taxation and Compliance: Foreign corporations may face unique tax implications as they are subject to taxation in both their home country and the foreign jurisdiction where they are doing business. Compliance with local laws, regulations, reporting requirements, and taxes becomes crucial for foreign corporations. Different Types of Domestic and Foreign Corporations: 1. Types of Domestic Corporations: — C Corporation (standard corporation— - S Corporation (tax benefit corporation) — NonprofiCorporationio— - Professional Corporation (for licensed professionals like lawyers or doctors) — Benefit Corporation (socially-responsible corporation) 2. Types of Foreign Corporations: — Branch Office (extension of the parent company) — Subsidiary (a separate legal entity owned by a foreign corporation) — Representative Office (limited operations for market research or sales) — Joint Venture (partnership with a local entity) — Regional Headquarters (coordinating operations in a specific region) Conclusion: In summary, domestic and foreign corporations differ in terms of formation, registration, governance, liability, taxation, and compliance. Domestic corporations are incorporated and operate within a specific country, while foreign corporations are formed in one country but conduct business activities in another. Understanding these differences is essential for businesses looking to expand their operations globally while aligning with local laws, regulations, and tax obligations.