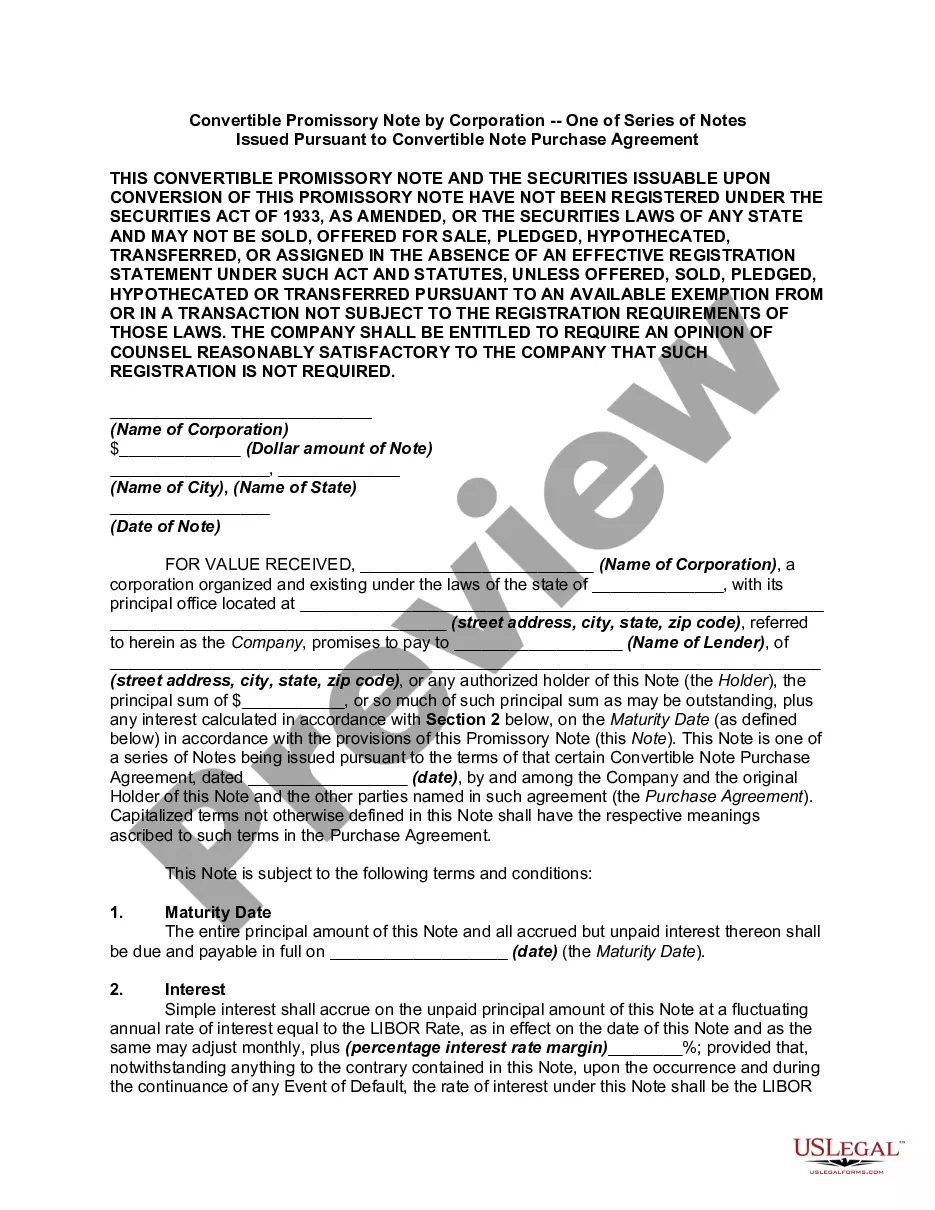

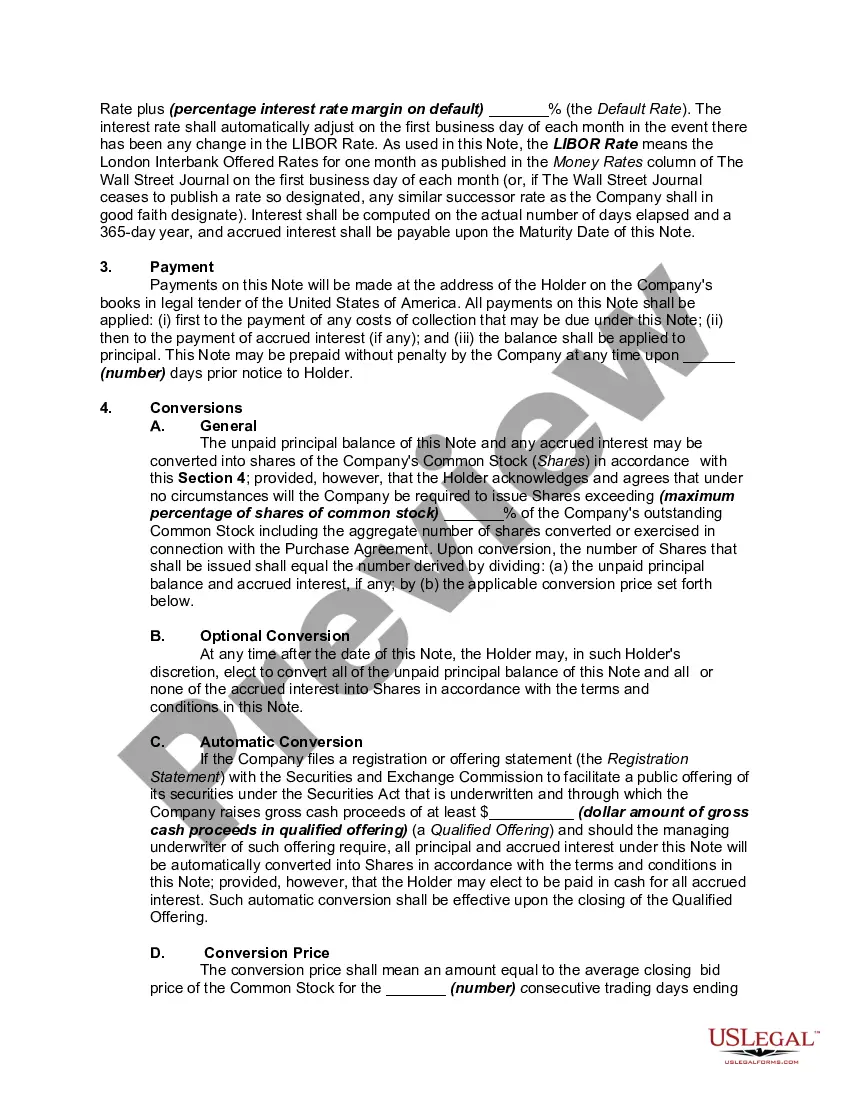

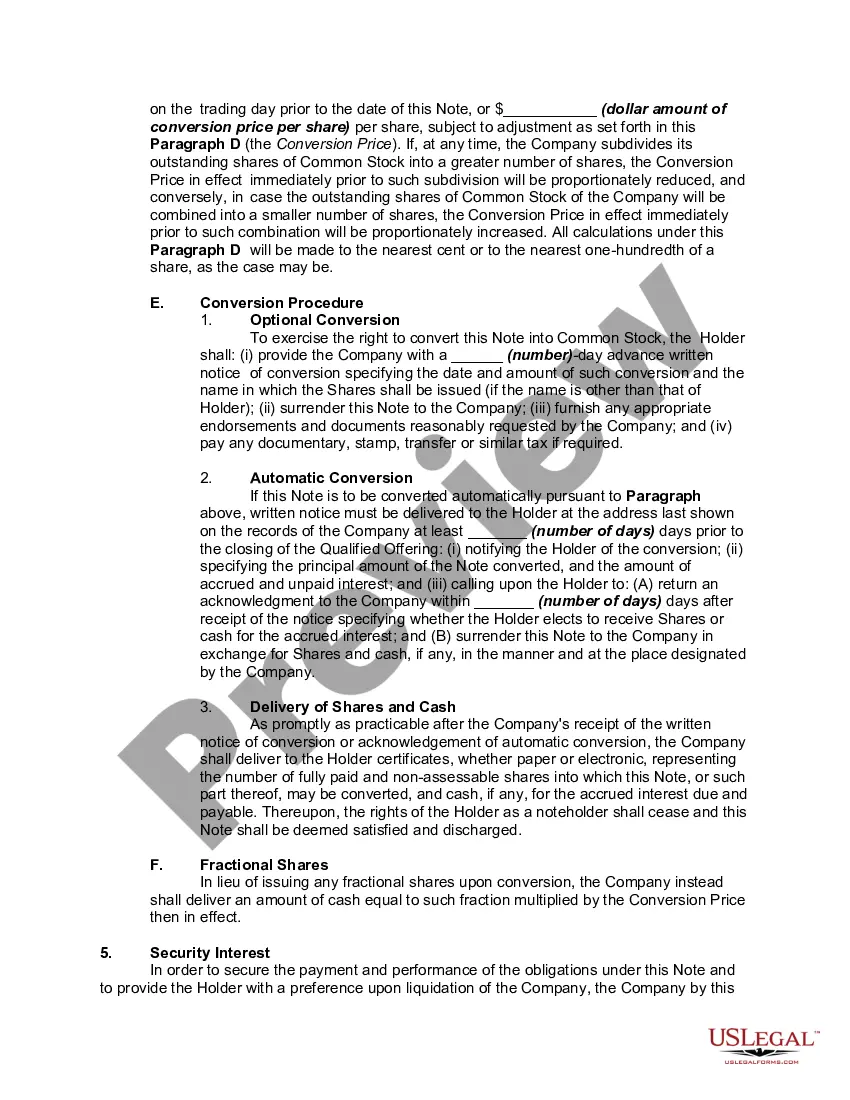

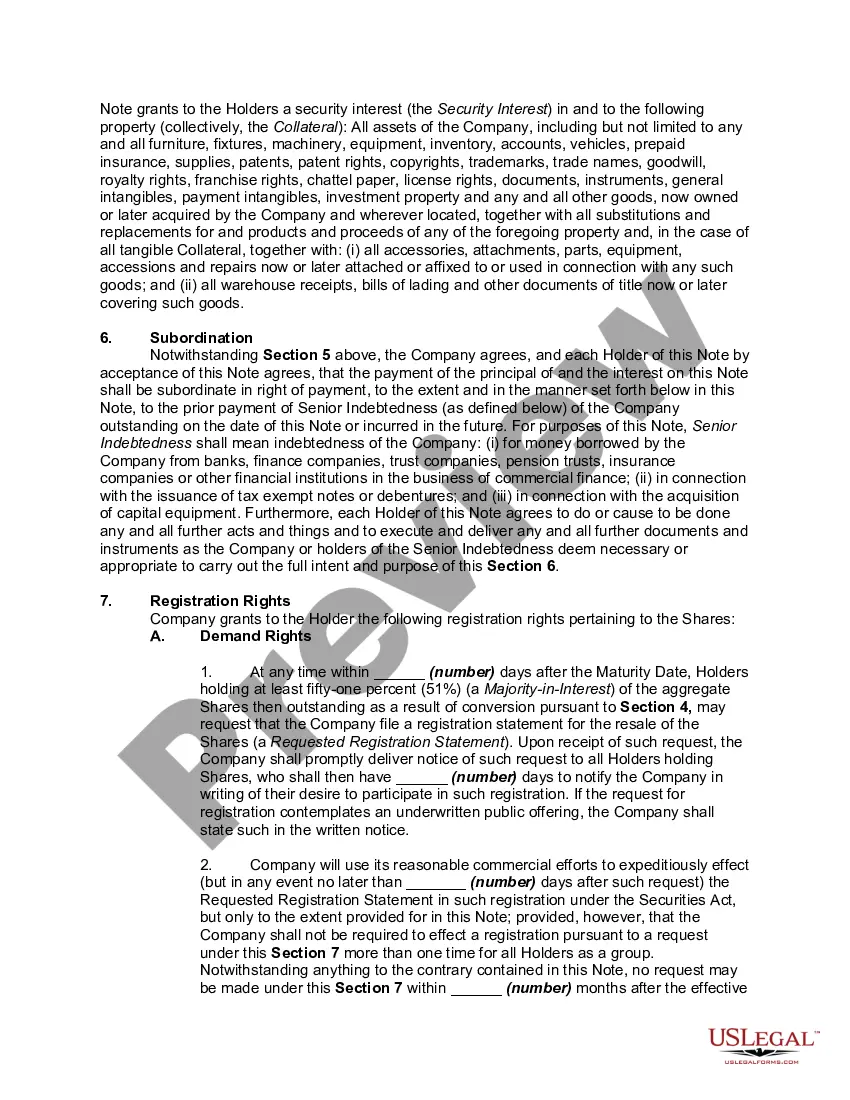

A Convertible Note is a simple promissory note, usually bearing interest and payable at some future date. The unique aspects of a convertible note are:

A. It converts into equity in the company so long as certain agreed metrics are achieved;

B. Conversion rather than repayment is the usual intention of the parties

C. The usual events for conversion (a conversion event) could be some or all of:

1. Later financing acquired of an agreed minimum level;

2. Developmental milestones reached by the company; and/or

3. Strategic partnerships concluded with important companies;

The conversion into equity is usually at a valuation that is consistent with the valuation agreed to with investors in an investment round that occurs at a later time.

A promissory note is a legally binding agreement between a borrower and a lender, in this case, a bank. It is a written promise by the borrower to repay a specific amount of money to the lender within a predetermined timeframe, usually with interest. This document serves as evidence of a debt obligation and outlines the terms and conditions of the loan. Promissory notes issued by banks can have different types depending on their purpose and features. Here are some common ones: 1. Commercial promissory notes: These notes are commonly used in business transactions, such as financing the purchase of assets, inventory, or covering operational expenses. Businesses may seek loans from banks to fund expansions, acquisitions, or to manage day-to-day operations. 2. Real estate promissory notes: Banks issue these notes specifically for funding real estate transactions, including property purchases, construction projects, or renovations. This type of promissory note may be secured by the property itself, serving as collateral for the loan. 3. Student promissory notes: These notes are often used by banks to provide educational loans to students pursuing higher education. The note outlines the terms and conditions of repayment, which typically begin after the student completes their education. Interest rates and deferment options may be available. 4. Personal promissory notes: Individuals may turn to their bank for personal loans, such as debt consolidation, home improvements, or covering unexpected expenses. The bank issues a personal promissory note, outlining the repayment terms and interest rates applicable to the loan. 5. Small business administration promissory notes: The Small Business Administration (SBA) works with banks to provide loans to small businesses through programs such as the SBA 7(a) or SBA 504. These promissory notes are designed to support small business growth and can have specific terms and conditions set by the SBA. It is important to carefully review and understand the terms of any promissory note issued by a bank before signing. Make sure to take note of the loan amount, interest rates, repayment schedule, and any penalties or fees for late payment or default. Always consult with legal and financial professionals to ensure you have a clear understanding of your obligations under the promissory note.