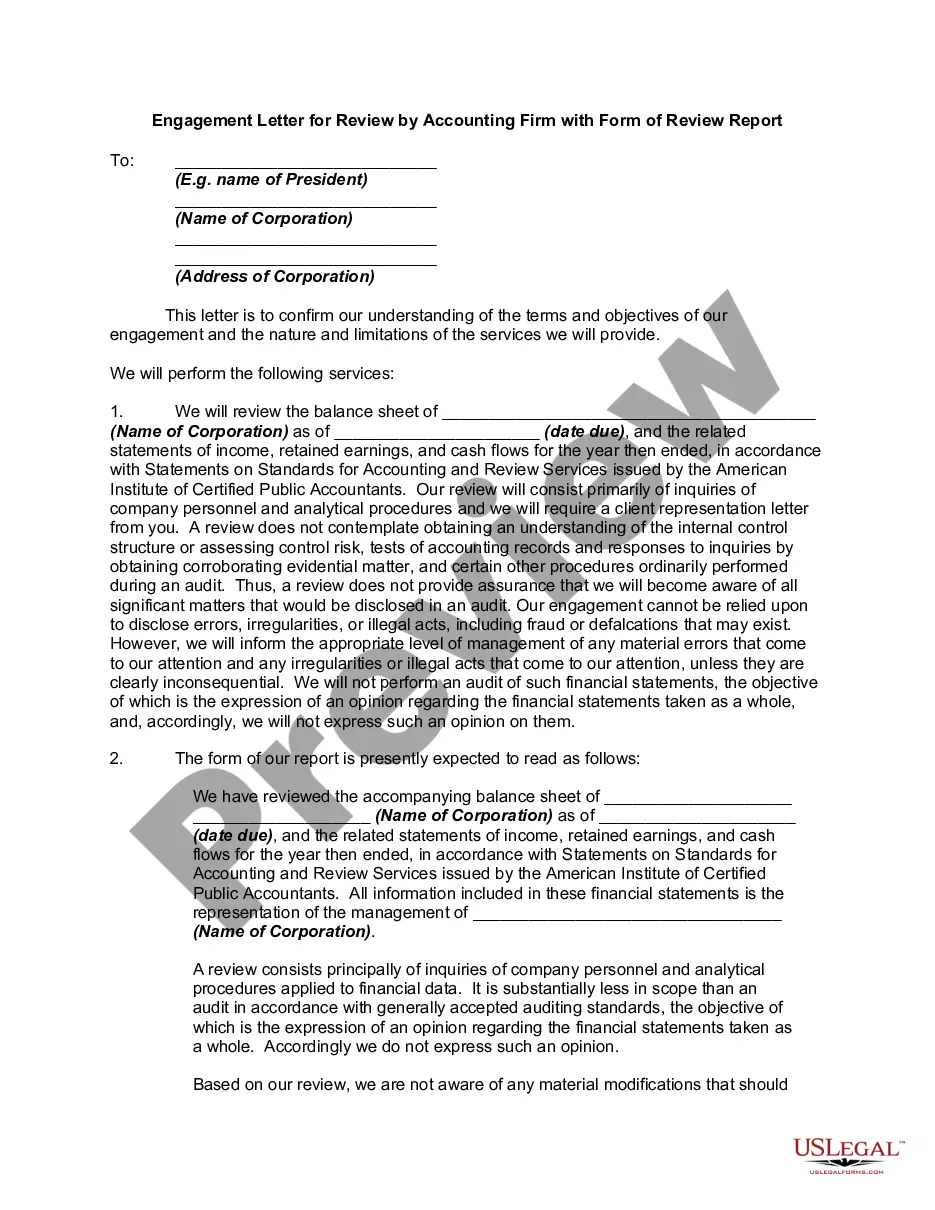

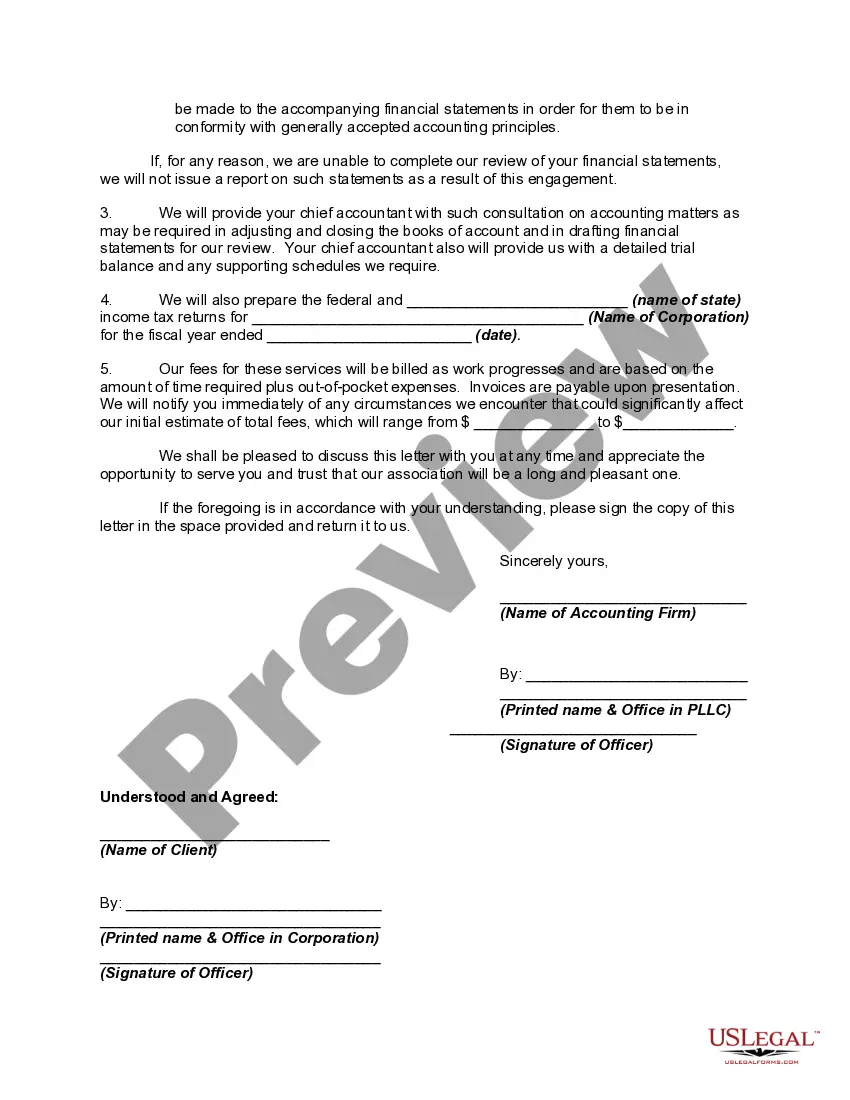

Generally, a contract to employ a certified public accountant need not be in writing. However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Audit engagement letter is a crucial document that outlines the terms and conditions agreed upon between auditors and their clients. The Institute of Chartered Accountants of India (CAI) provides a specific format for an Audit engagement letter. This letter sets the ground rules, scopes, and responsibilities of both parties involved in the audit process. The format recommended by CAI ensures transparency, accuracy, and professionalism in carrying out audits. The typical format of an Audit engagement letter example as per CAI includes the following important elements: 1. Date: The letter starts with the date it is issued to clearly establish the timeline of the engagement. 2. Addressee: The letter is addressed to the management or the client, acknowledging their responsibility and cooperation during the audit process. 3. Objective and Scope: It specifies the objectives of the audit engagement, such as expressing an opinion on the financial statements' fairness and compliance with relevant laws and regulations. The scope outlines the areas and activities covered by the audit, ensuring clarity on what will be assessed. 4. Responsibilities of Management: This section highlights the client's responsibility to provide accurate financial records, documents, and unrestricted access to relevant information. It emphasizes the role of management in maintaining internal controls and ensuring the completeness and accuracy of the financial statements. 5. Responsibilities of Auditors: It outlines the auditors' responsibilities in conducting the audit, including complying with auditing standards, planning and executing the audit work, and forming an opinion based on the evidence gathered. 6. Audit Procedures: This section briefly describes the audit procedures to be performed by the auditors, such as risk assessment, substantive procedures, review of internal controls, etc. 7. Timeline: The engagement letter includes the estimated start and end dates of the audit engagement. 8. Fees and Billing: It specifies the audit fees, payment terms, and any additional costs to be covered. 9. Confidentiality: This section establishes the confidentiality obligations of both parties to maintain the privacy of sensitive information obtained during the audit process. 10. Termination: It clearly states the conditions under which the engagement can be terminated by either party. Typically, it includes non-compliance with agreed terms, conflict of interest, or if any party becomes aware of any unethical conduct. Different types of Audit engagement letters as per CAI may include: 1. Standard Audit Engagement Letter: This is the most common type of engagement letter used when auditing the financial statements of a company. 2. Limited Scope Audit Engagement Letter: Used when the audit is specifically focused on a particular area of concern, such as internal controls or compliance with specific regulations. 3. Examination Engagement Letter: Used when the engagement is to examine specific financial information or statements for a specific purpose, like for a loan application or due diligence process. In conclusion, the Audit engagement letter example format provided by CAI lays down the foundation for a successful and professional audit engagement. It ensures clarity, defines responsibilities, and establishes mutual understanding between auditors and clients. Adhering to this format enhances the quality and effectiveness of the audit process, thereby fostering trust and credibility in financial reporting.