An escrow is the deposit of a written instrument or something of value with a third person with instructions to deliver it to another when a stated condition is performed or a specified event occurs. The use of an escrow is most common in real estate sales transactions where the grantee deposits earnest money with the escrow agent to be delivered to the grantor upon consummation of the purchase and sale of the real estate and performance of other specified conditions.

Real Property Deposit Withholding Tax is a type of tax imposed on property sellers or landlords who receive a deposit for the sale or lease agreement of real estate. This withholding tax is deducted from the deposit amount and remitted to the appropriate taxation authority. The primary purpose of the Real Property Deposit Withholding Tax is to ensure compliance with tax obligations and prevent tax evasion. It acts as a security blanket for the taxation authority, ensuring that the tax liability associated with the sale or lease of real estate is addressed at the earliest stage of the transaction. When it comes to different types of Real Property Deposit Withholding Tax, various jurisdictions may have their own specific regulations and classifications. However, below are some commonly seen types of Real Property Deposit Withholding Tax: 1. Capital Gains Withholding Tax: This type of withholding tax is applicable when a seller plans to dispose of a real estate property. The tax is withheld from the deposit amount to cover any potential capital gains tax liability that may arise from the sale. 2. Rental Income Withholding Tax: In situations where a property is being leased, landlords may be required to withhold a portion of the deposit as a form of rental income tax. This protects the taxation authority by ensuring that the tax liability associated with the rental income is addressed upfront. 3. Non-Resident Withholding Tax: Some jurisdictions impose a withholding tax on deposits made by non-residents for the purchase or lease of real estate. This tax is withheld at the time of deposit to account for potential tax obligations non-residents might have concerning the transaction. 4. Sales Tax Withholding: Some regions may require sellers to withhold a specific percentage of the deposit as sales tax on the real property. This ensures that the tax liability associated with sales tax is fulfilled before the completion of the transaction. It is essential for property sellers, landlords, and buyers/tenants to familiarize themselves with the specific regulations and requirements related to Real Property Deposit Withholding Taxes in their respective jurisdictions. Non-compliance with these regulations can lead to penalties, fines, and potential legal complications. Thus, seeking professional advice from tax experts or consulting relevant government resources is highly recommended ensuring adherence to the applicable withholding tax laws.

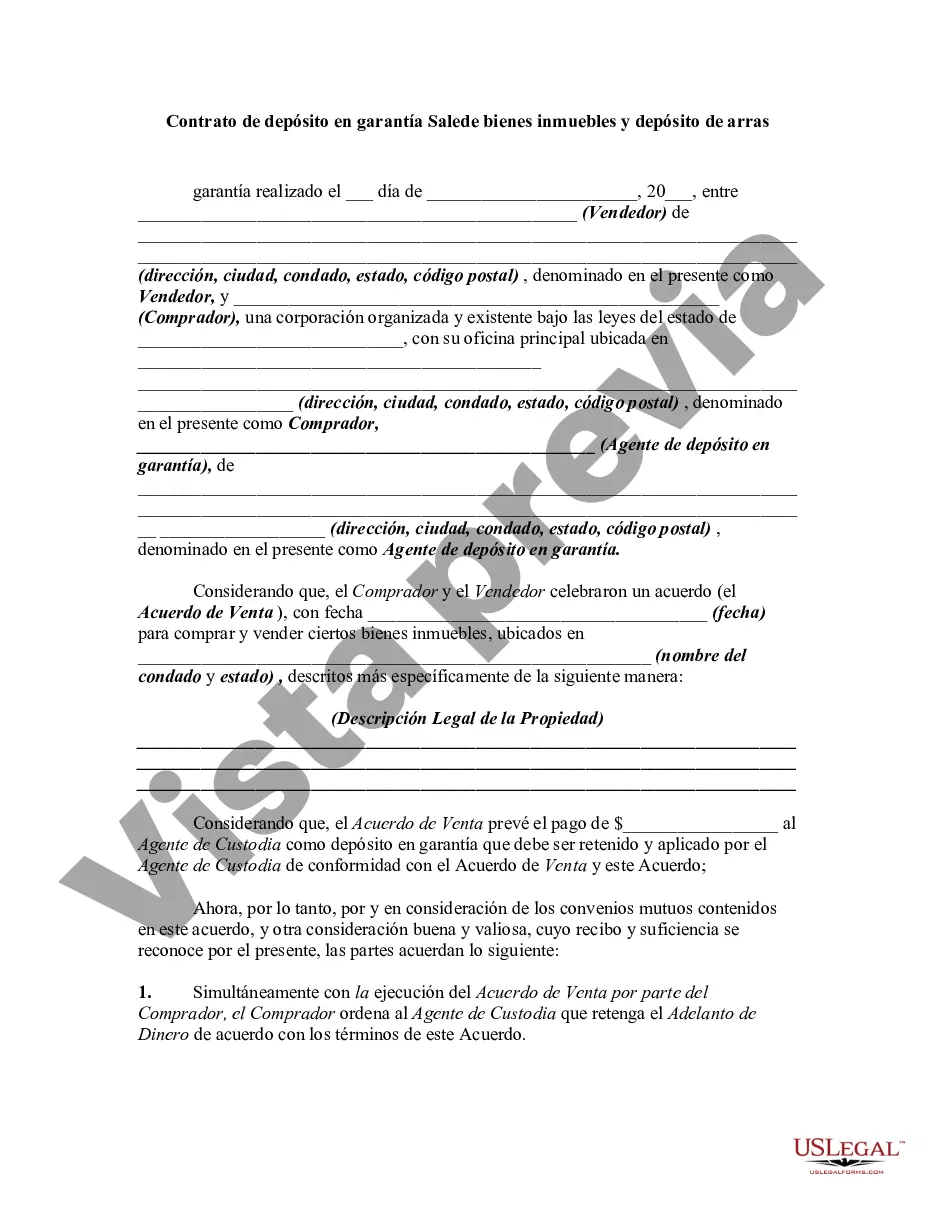

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.