New York Corporate NY Withholding Tax: A Comprehensive Overview Introduction: New York corporate NY withholding tax is a type of tax imposed on businesses conducting operations in the state of New York. It is withheld from various types of payments made by a business entity to non-resident individuals or entities as mandated by the New York State Department of Taxation and Finance (MYSELF). This tax is part of the state's efforts to collect revenues and ensure compliance with tax regulations. Let's delve into the details of New York corporate NY withholding tax and its different types. Key Concepts: 1. Withholding Tax: Withholding tax is an amount deducted or withheld from payments made to non-residents that will be credited against their final tax liability. In the case of New York corporate NY withholding tax, it is the responsibility of the paying entity to withhold a certain percentage of a payment and remit it to the. 2. Non-Resident Individual or Entity: A non-resident individual refers to someone who resides outside of New York but receives income from a New York-based source, such as wages or business income. A non-resident entity comprises businesses or organizations not incorporated or organized under New York State laws. Types of New York Corporate NY Withholding Tax: 1. Non-Resident Employee Wage Withholding: When a non-resident employee works in New York, the employer is required to deduct New York State income tax from the employee's wages. The withholding tax depends on the employee's income level and filing status. The employer must register with the and submit the withheld tax on behalf of the employee. 2. Non-Resident Self-Employment Tax: Non-resident individuals engaged in self-employment activities in New York are subject to New York corporate NY withholding tax. They need to register with the, make estimated tax payments, and file an annual return reporting their self-employment income. 3. Non-Resident Corporate Partners/Shareholders: If a non-resident individual or entity is a partner or shareholder in a New York-based partnership or corporation, the partnership or corporation may be required to withhold tax on behalf of the non-resident partner or shareholder. The withheld amount is then remitted to the. 4. Rental Income Withholding: When a non-resident individual or entity earns rental income from a New York property, the person or entity that pays the rental income needs to withhold a specific percentage of the payment and remit it to the. Conclusion: New York corporate NY withholding tax encompasses various types of taxes imposed on non-resident individuals or entities doing business or earning income within the state. By adhering to the withholding requirements, businesses ensure compliance with New York State tax laws and contribute to the state's revenue collection. It is essential for businesses and individuals to understand the different types of New York corporate NY withholding taxes, their rates, and filing obligations to avoid any penalties or non-compliance issues.

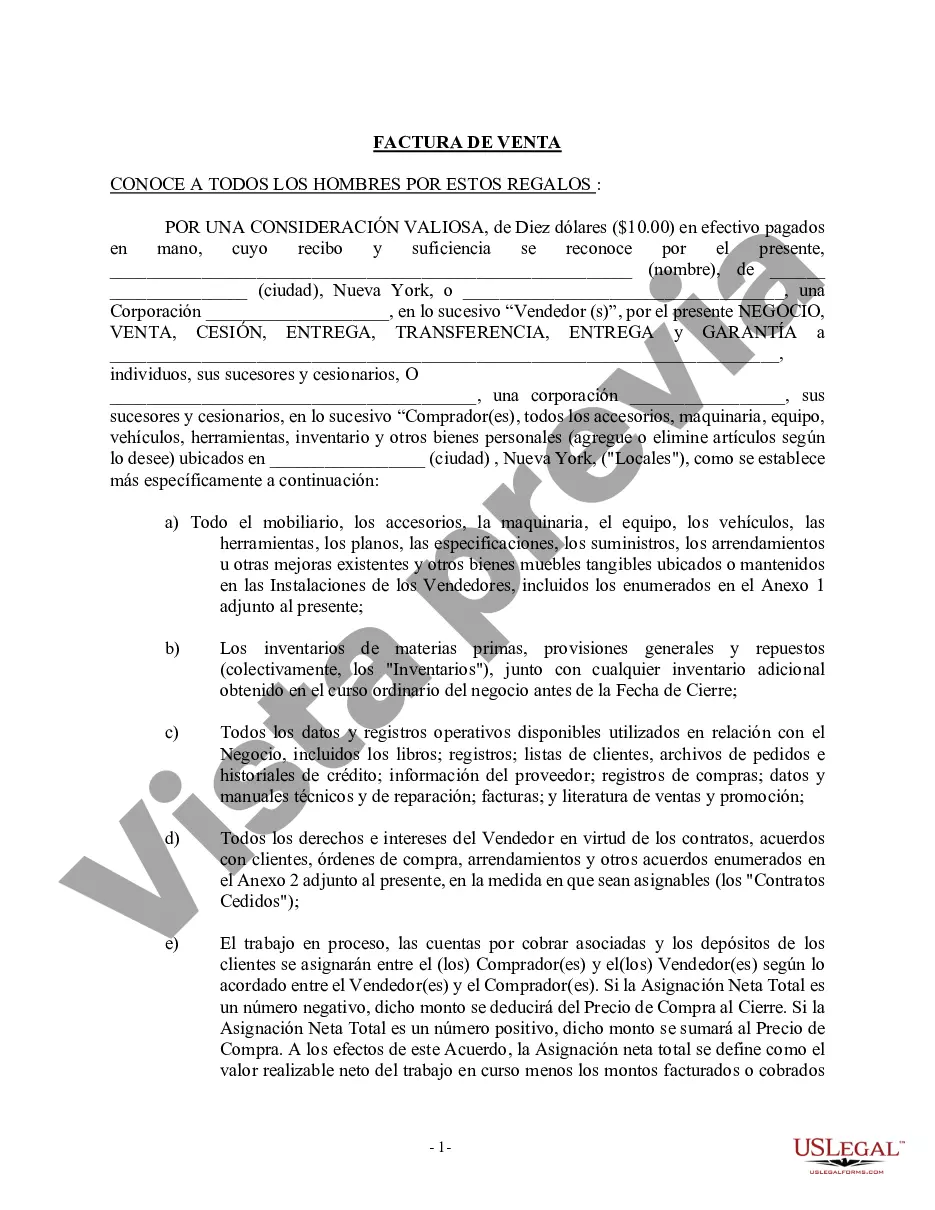

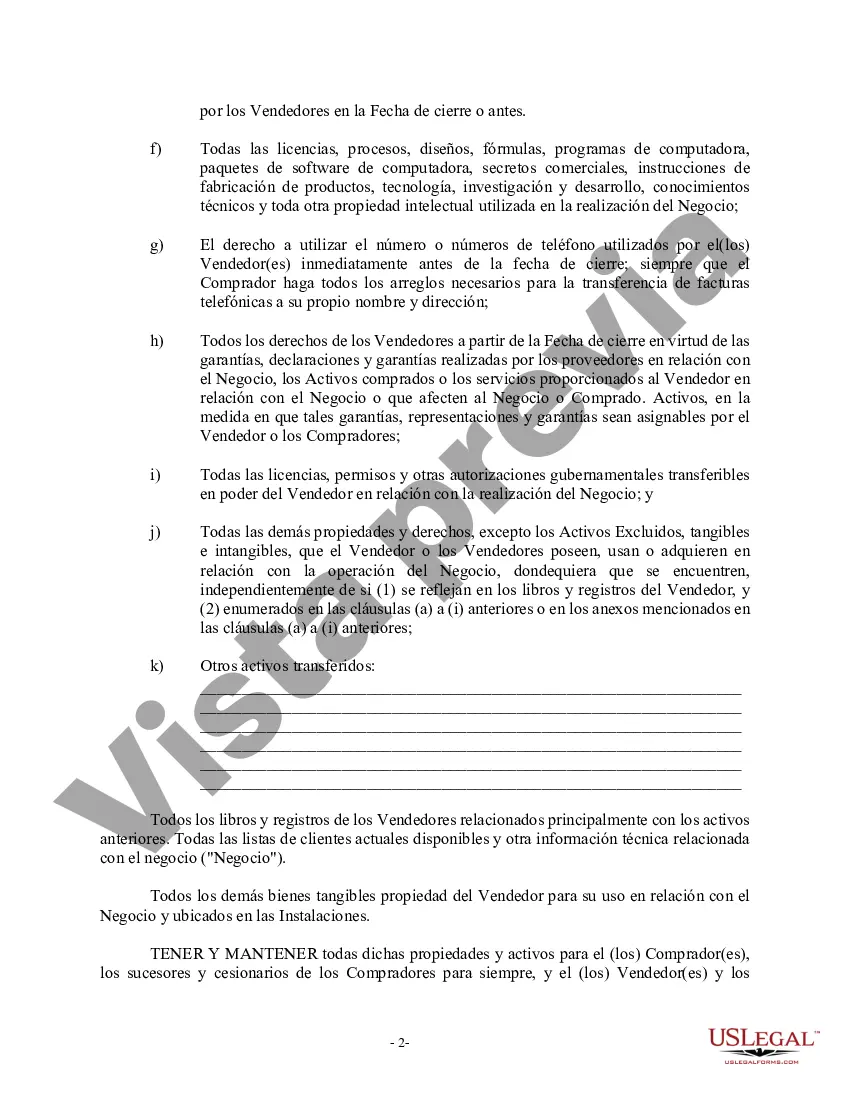

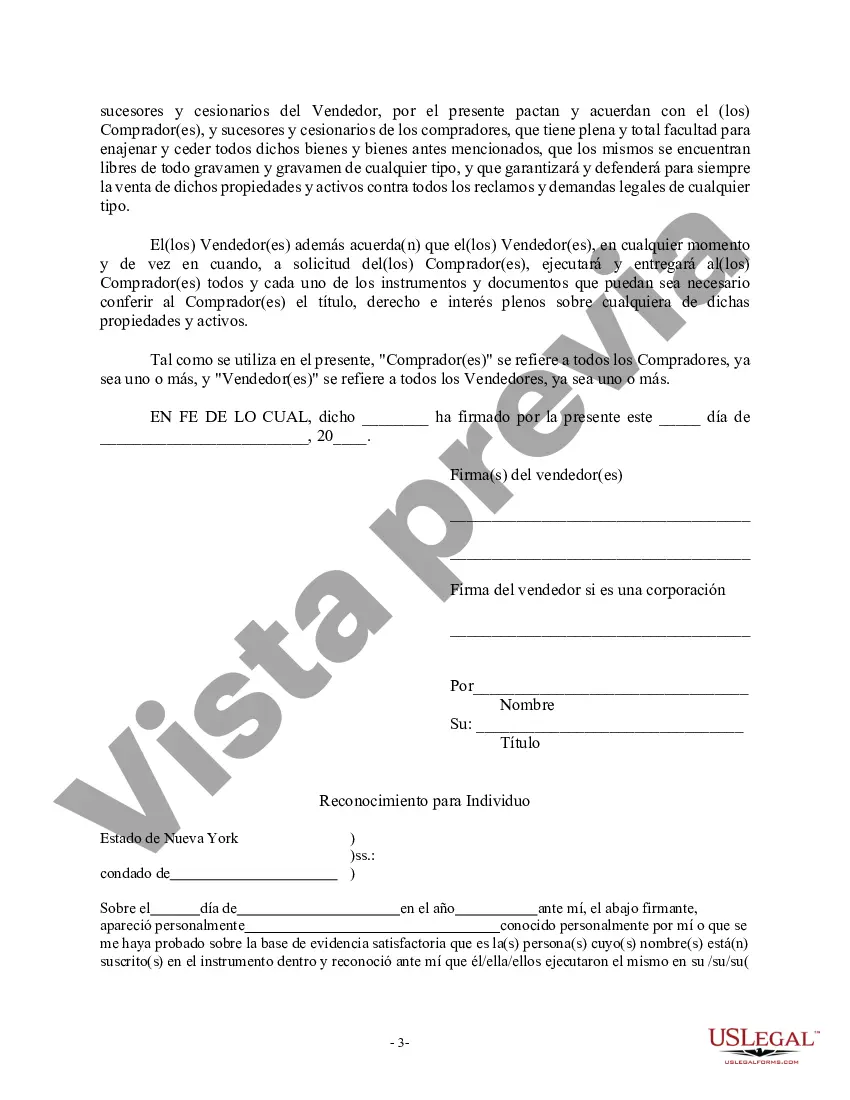

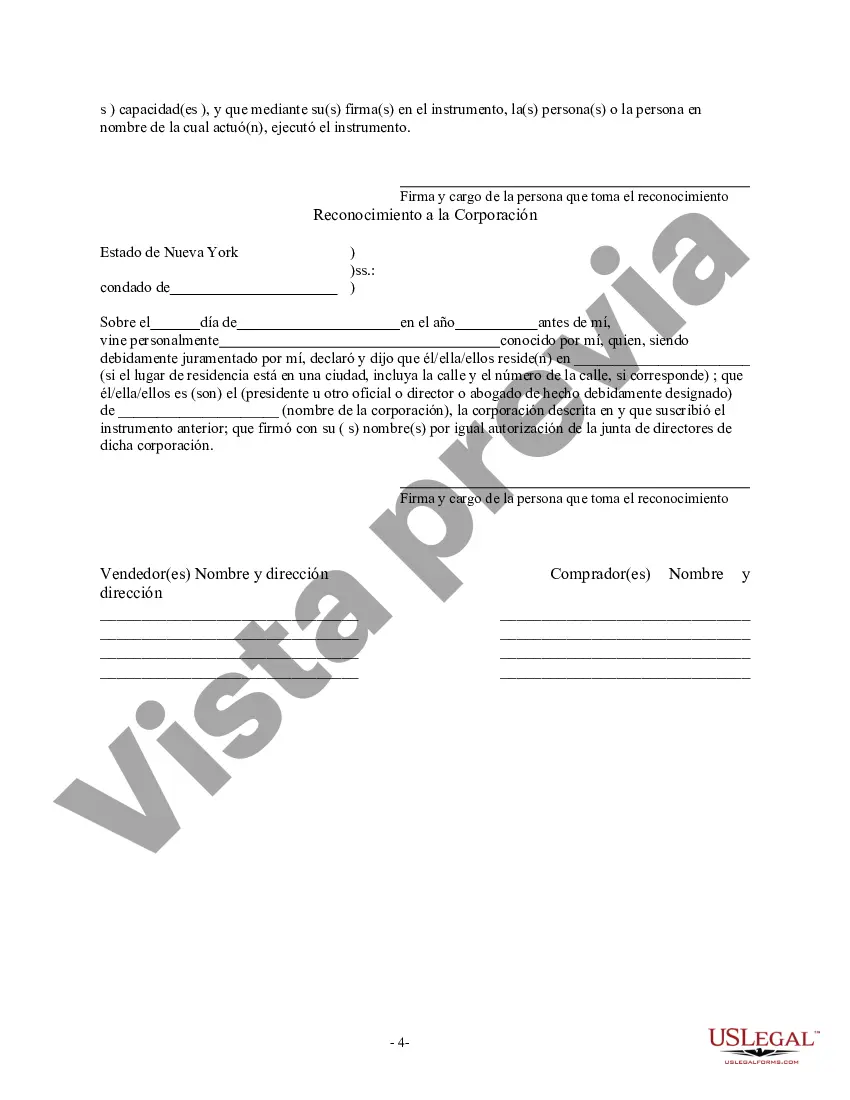

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.New York Factura de venta en relación con la venta del negocio por parte del vendedor individual o corporativo - New York Bill of Sale in Connection with Sale of Business by Individual or Corporate Seller

Description

How to fill out New York Factura De Venta En Relación Con La Venta Del Negocio Por Parte Del Vendedor Individual O Corporativo?

US Legal Forms is a unique system where you can find any legal or tax document for submitting, including New York Bill of Sale in Connection with Sale of Business by Individual or Corporate Seller. If you’re tired with wasting time looking for suitable samples and paying money on document preparation/attorney service fees, then US Legal Forms is exactly what you’re seeking.

To experience all of the service’s benefits, you don't have to download any software but just choose a subscription plan and register your account. If you already have one, just log in and find an appropriate sample, save it, and fill it out. Downloaded files are stored in the My Forms folder.

If you don't have a subscription but need to have New York Bill of Sale in Connection with Sale of Business by Individual or Corporate Seller, check out the instructions below:

- make sure that the form you’re looking at applies in the state you want it in.

- Preview the sample its description.

- Simply click Buy Now to access the sign up webpage.

- Pick a pricing plan and proceed signing up by providing some info.

- Select a payment method to complete the sign up.

- Download the file by choosing the preferred format (.docx or .pdf)

Now, submit the document online or print out it. If you are unsure about your New York Bill of Sale in Connection with Sale of Business by Individual or Corporate Seller sample, contact a legal professional to review it before you send out or file it. Get started without hassles!