A deed of trust is a document which pledges real property to secure a loan, used instead of a mortgage in certain states. A deed of trust involves a third party called a trustee, usually an attorney of officer of the lender, who acts on behalf of the lender. When you sign a deed of trust, you in effect are giving a trustee title to the property, but you hold the rights and privileges to use and live in or on the property. If the loan becomes delinquent the beneficiary can file a notice of default and, if the loan is not brought current, can demand that the trustee begin foreclosure on the property so that the beneficiary (lender) may either be paid or obtain title. Unlike a mortgage, a deed of trust also gives the trustee the right to foreclose on your property without taking you to court first.

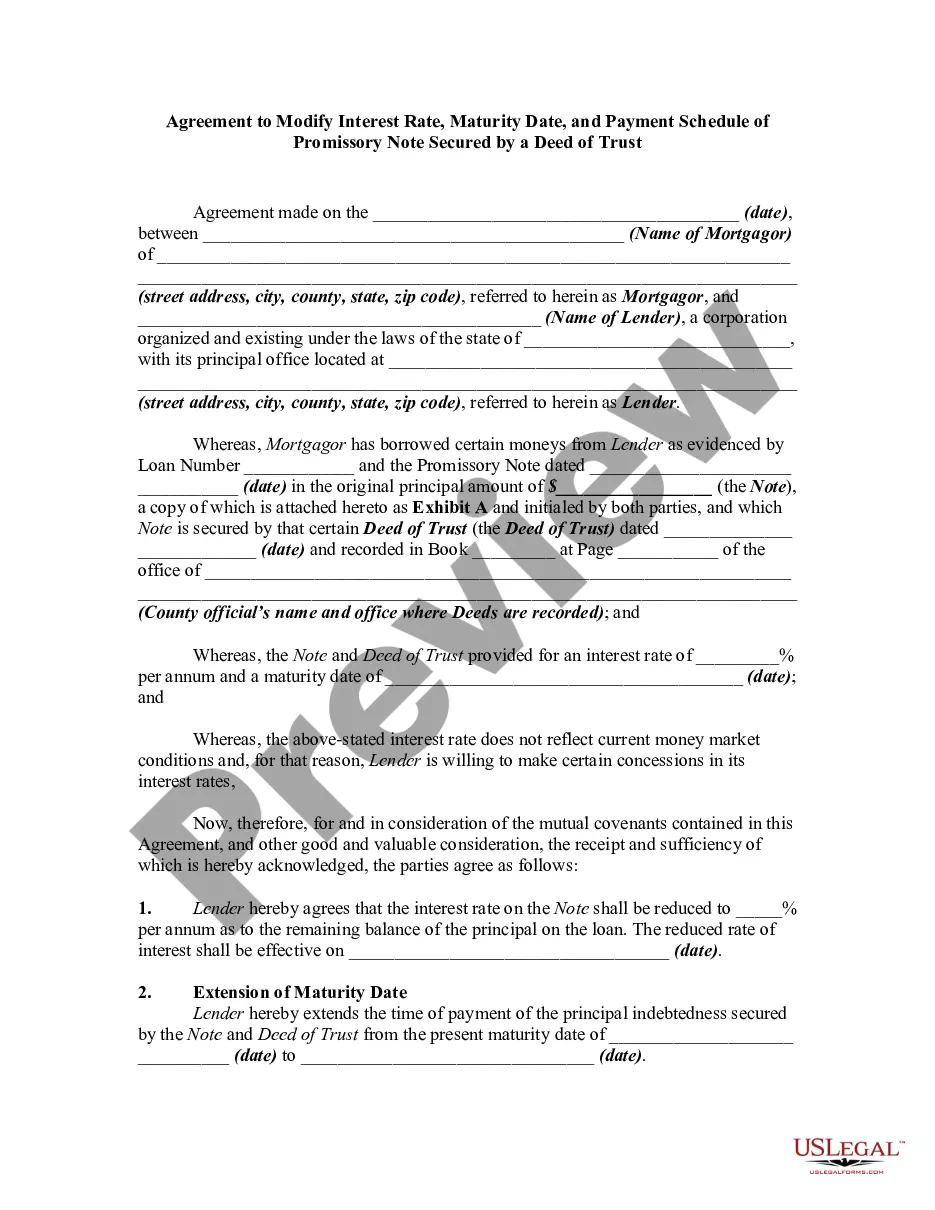

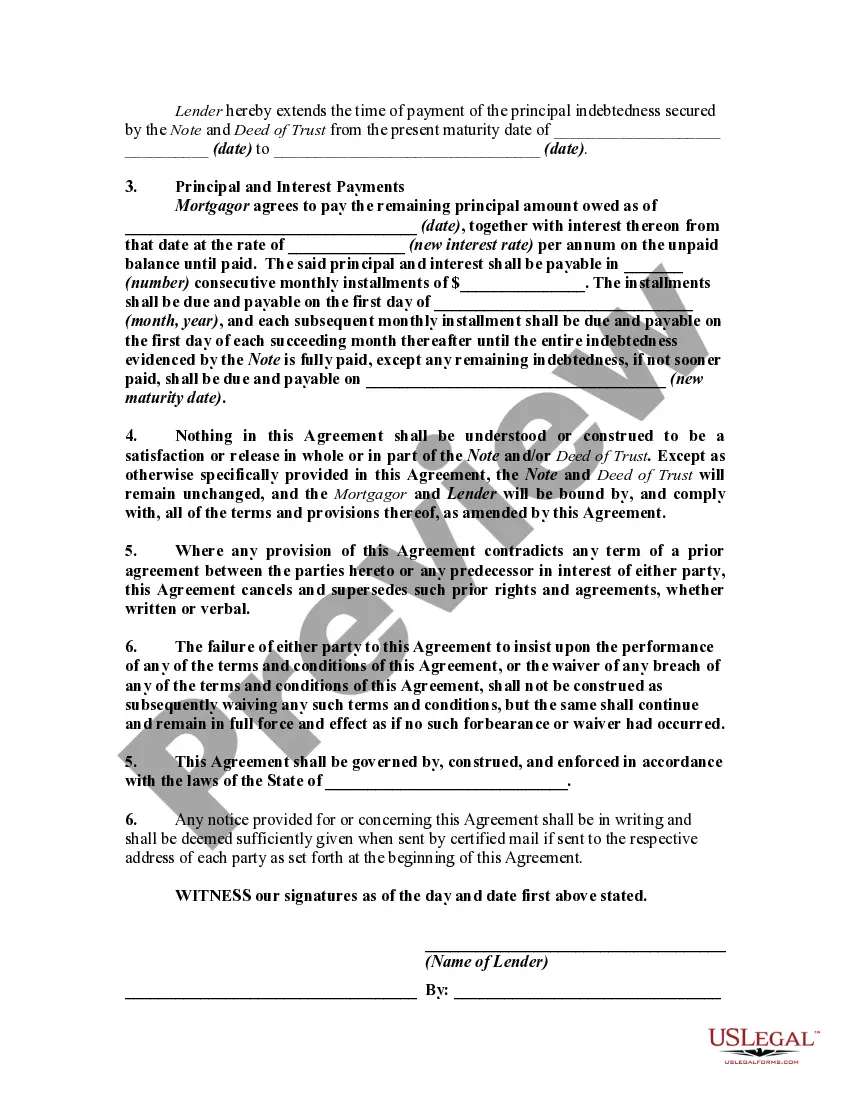

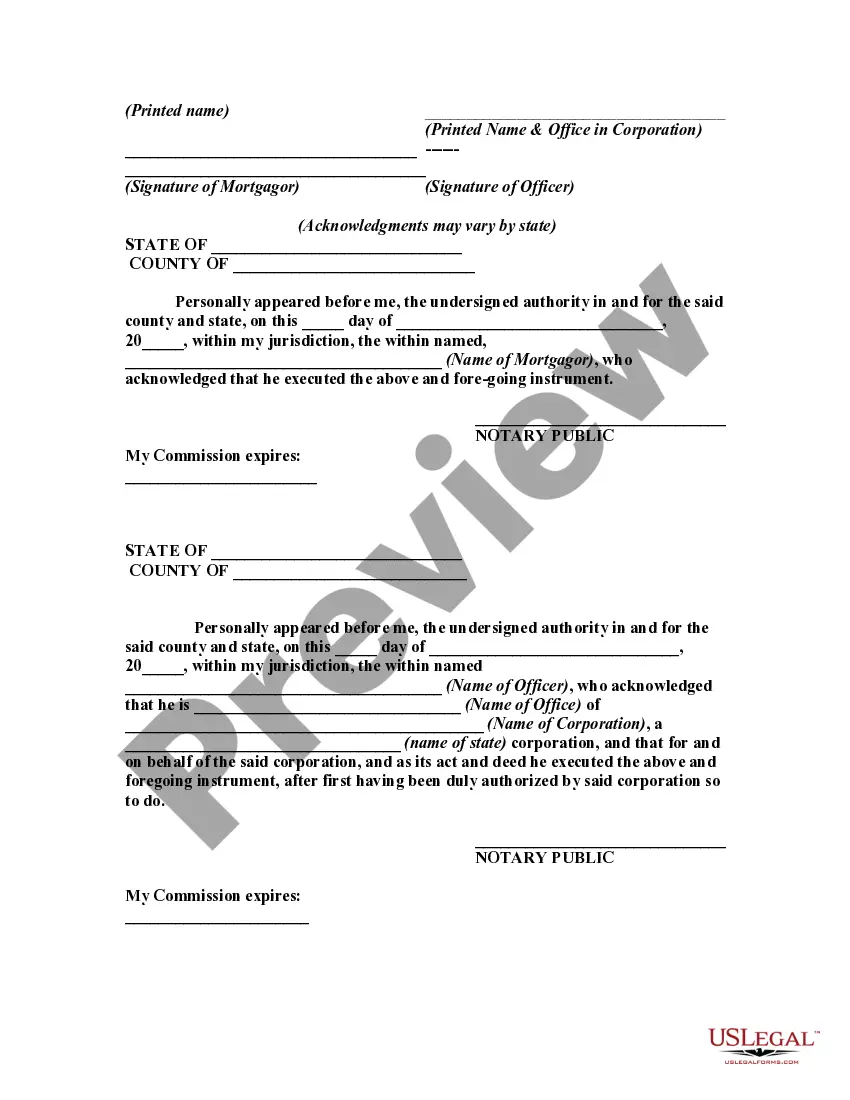

An agreement modifying a promissory note and deed of trust should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original deed of trust was recorded.

An agreement promissory note for tuition fee is a legally binding document signed between two parties, typically a student and an educational institution. This note outlines the terms and conditions under which the student agrees to repay the tuition fees owed to the institution. The main purpose of an agreement promissory note for tuition fee is to establish a formal agreement, ensuring that the student acknowledges their financial obligation and commits to repaying the tuition fees in a specified manner. This document helps provide clarity and security to both parties involved. Key elements included in an agreement promissory note for tuition fee are the names and contact information of the parties involved, the date of the agreement, the total amount owed, and the agreed-upon repayment terms. The repayment terms usually include the frequency of payments, the payment amount, and any specific deadlines or grace periods. There are different types of agreement promissory notes for tuition fees, each tailored to fit specific circumstances and requirements. Some commonly named variations include: 1. Installment Promissory Note: This type of note allows the student to repay the tuition fees in equal installments over a specified period. 2. Deferred Payment Promissory Note: This note permits the student to postpone the repayment of tuition fees until a later predetermined date, usually after completing their studies. 3. Balloon Promissory Note: With this note, the student agrees to make smaller periodic payments during their studies, with the remaining balance due after graduation or a certain milestone. 4. Consolidation Promissory Note: This note is used when a student consolidates multiple outstanding tuition fees into a single, manageable repayment plan. 5. Co-signer Promissory Note: In cases where a student does not meet the credit requirements, a co-signer may be required to sign this note, assuming responsibility for the repayment if the student fails to fulfill their obligations. It is crucial for both parties to carefully review and understand the terms specified in the agreement promissory note for tuition fee before signing. This helps ensure transparency, prevent misunderstandings, and establish a secure financial arrangement between the institution and the student.