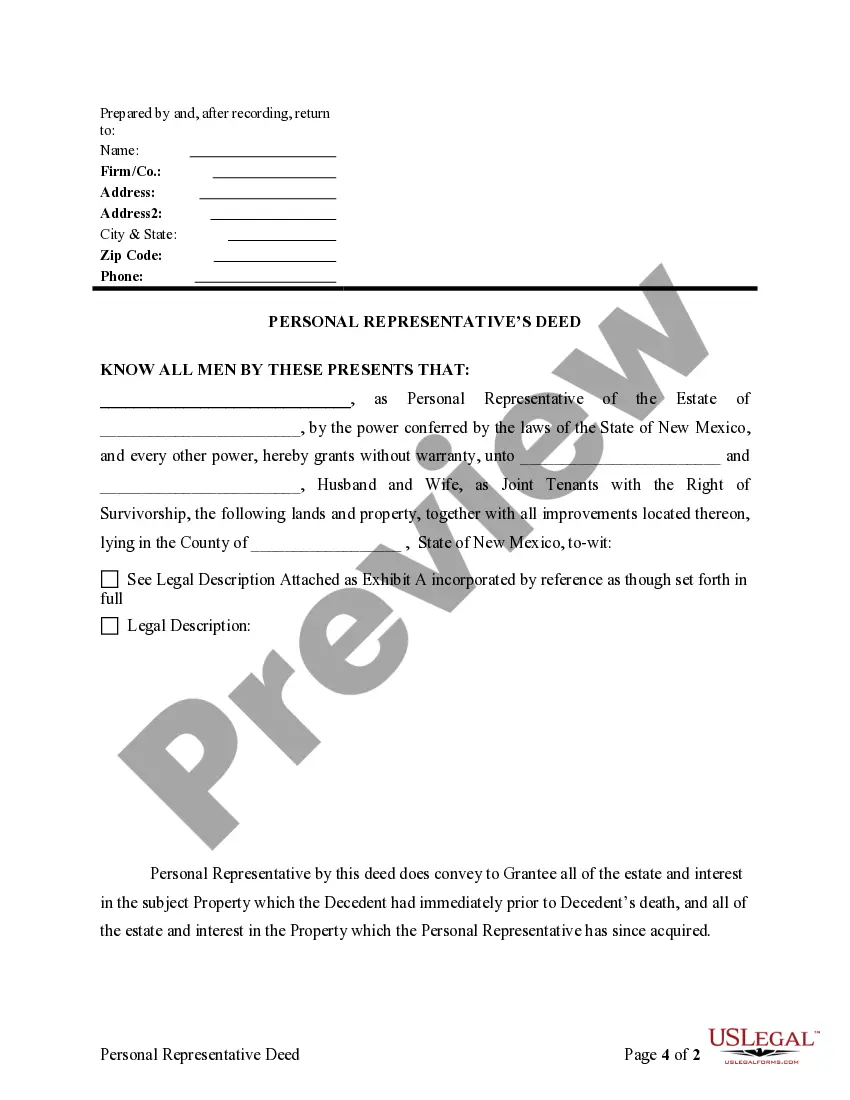

Personal Representative Deed New Mexico Withholding: An Overview In the state of New Mexico, when it comes to property transactions involving a Personal Representative Deed, certain withholding requirements must be considered. This article aims to provide a detailed description of what Personal Representative Deed withholding in New Mexico entails, including an explanation of withholding and relevant keywords. Personal Representative Deed: Before delving into the withholding aspect, let's briefly explain what a Personal Representative Deed is. A Personal Representative Deed, also known as an Executor's Deed, is a legal document used to transfer real property from an estate to heirs or beneficiaries. It is typically executed by an appointed personal representative, often referred to as the executor or administrator, who is responsible for managing the affairs of a deceased individual's estate. New Mexico Withholding: In New Mexico, the Tax Administration Act (Section 7-1-8.1 NASA 1978) stipulates that certain real property transactions may be subject to withholding requirements. Specifically, when a Personal Representative Deed is used to transfer property, the buyer or transferee is obligated to withhold a percentage of the gross sales price and remit it to the New Mexico Taxation and Revenue Department (TRY). Withholding Percentage and Threshold: The withholding percentage for Personal Representative Deed transactions in New Mexico is generally 3% of the gross sales price. However, it is important to note that certain exemptions or reductions may apply based on the total sales price threshold. As of the time of writing, the current threshold for exemption or reduced withholding is set at $100,000. Dealing with Exceptions: There are exceptions to the withholding requirement for certain types of Personal Representative Deed transactions. For instance, if the property being transferred is the buyer's main residence, the withholding requirement may be waived. Additionally, if the buyer or transferee obtains a certification from the TRY stating that the seller is not liable for withholding, the transaction may be exempted from withholding as well. Reporting and Remitting: To ensure compliance, it is crucial for the buyer or transferee to file a Personal Representative Deed Real Estate Withholding Tax Return (Form RPD-41096) with the TRY. This form provides the necessary information, including details of the transaction, the amount withheld, and the applicable exemptions. The withholding amount must be remitted to the TRY within 20 days from the date of transfer of the property. Conclusion: In conclusion, Personal Representative Deed New Mexico Withholding is a process that requires buyers or transferees to withhold a percentage of the gross sales price when acquiring property through a Personal Representative Deed. The applicable withholding percentage is generally 3%, with exemptions or reduced withholding available for transactions below the $100,000 sales price threshold. Compliance with reporting and remitting obligations to the TRY is essential to avoid penalties and ensure smooth property transfers.

Personal Representative Deed New Mexico

Description Personal Representative Deed Form New Mexico

How to fill out Personal Representatives Form?

Among lots of free and paid samples that you’re able to get on the net, you can't be sure about their reliability. For example, who created them or if they’re competent enough to deal with what you require them to. Always keep relaxed and make use of US Legal Forms! Find New Mexico Quitclaim Deed for Personal Representative's Deed templates created by skilled lawyers and get away from the costly and time-consuming process of looking for an lawyer and after that having to pay them to draft a papers for you that you can find on your own.

If you have a subscription, log in to your account and find the Download button next to the form you’re trying to find. You'll also be able to access all of your previously saved files in the My Forms menu.

If you are making use of our service the very first time, follow the tips listed below to get your New Mexico Quitclaim Deed for Personal Representative's Deed with ease:

- Make certain that the file you see is valid in the state where you live.

- Look at the file by reading the description for using the Preview function.

- Click Buy Now to begin the ordering procedure or look for another sample utilizing the Search field found in the header.

- Select a pricing plan sign up for an account.

- Pay for the subscription with your credit/debit/debit/credit card or Paypal.

- Download the form in the needed file format.

Once you have signed up and bought your subscription, you can use your New Mexico Quitclaim Deed for Personal Representative's Deed as often as you need or for as long as it continues to be active where you live. Revise it with your favorite offline or online editor, fill it out, sign it, and create a hard copy of it. Do far more for less with US Legal Forms!