Loading

Get Md Noi Mortgage Loan Default

How it works

-

Open form follow the instructions

-

Easily sign the form with your finger

-

Send filled & signed form or save

How to fill out the MD NOI Mortgage Loan Default online

Filling out the MD NOI Mortgage Loan Default form is a crucial step for individuals facing potential foreclosure. This guide will provide clear, step-by-step instructions to help you complete the form accurately and efficiently online.

Follow the steps to fill out the MD NOI Mortgage Loan Default form online.

- Click ‘Get Form’ button to obtain the form and open it in your preferred online editor.

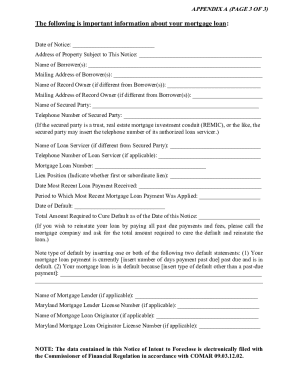

- Begin by reading the entire Notice carefully. This includes the details regarding the loan status and the potential consequences of not addressing the default.

- Locate the section dedicated to filling out your personal information. Enter the name of the borrower(s), the address of the property, and the mailing address of the borrower(s) accurately.

- In the section labeled 'Name of Secured Party', provide the name of the mortgage company. You will also need to fill in the telephone number for easy communication regarding your loan.

- Next, indicate the mortgage loan number and the lien position (first or subordinate). This information is essential for precise identification of your loan.

- Complete the section detailing the loan's default status. Insert the number of days the payment is past due and any other relevant default reasons, if applicable.

- After entering the required information, review the details to ensure accuracy. Mistakes may delay processing or complicate your situation.

- Finally, save the changes you made, and choose to download or print the completed form. You may also share it if necessary for further assistance.

Take action now and complete the MD NOI Mortgage Loan Default form online to secure your options.

Foreclosure in Maryland usually takes around six months to a year after the notice of default is issued. This timeframe can vary based on the circumstances of your case. The process involves specific legal steps that must be followed, making it crucial to stay informed about your situation. Engaging with our platform at USLegalForms can provide insights to help navigate this challenging time.