We use cookies to improve security, personalize the user experience, enhance our marketing activities (including cooperating with our marketing partners) and for other business use.

Click "here" to read our Cookie Policy. By clicking "Accept" you agree to the use of cookies. Read less

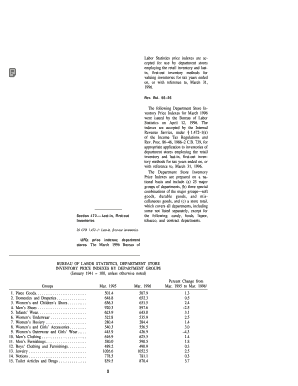

R use by department stores employing the retail inventory and lastin, first-out inventory methods for valuing inventories for tax years ended on, or with reference to, March 31, 1996. Rev. Rul. 96 26 The following Department Store Inventory Price Indexes for March 1996 were issued by the Bureau of Labor Statistics on April 12, 1996. The indexes are accepted by the Internal Revenue Service, under 1.472 1(k) of the Income Tax Regulations and Rev. Proc. 86 46, 1986 2 C.B. 739, for approp.

How It Works

Open form follow the instructions

Easily sign the form with your finger

Send filled & signed form or save

3the rating

★★★★★

★★★★

★★★

★★

★

4.8Satisfied

56 votes

How to fill out and sign goods2

online?

Get your online template and fill it in using progressive

features. Enjoy smart fillable fields and interactivity. Follow the simple instructions

below:

Are you seeking a fast and practical tool to fill in Revenue Ruling 1996-26 - LIFO at a reasonable cost? Our platform provides you with a rich library of forms available for submitting online. It only takes a few minutes.

Keep to these simple steps to get Revenue Ruling 1996-26 - LIFO prepared for submitting:

Get the sample you will need in our library of legal forms.

Open the template in the online editor.

Go through the instructions to discover which details you must give.

Select the fillable fields and add the required data.

Add the relevant date and insert your electronic signature once you fill out all of the fields.

Look at the document for misprints and other mistakes. If there?s a need to correct something, the online editor as well as its wide range of instruments are at your disposal.

Download the filled out form to your computer by clicking on Done.

Send the e-document to the intended recipient.

Filling in Revenue Ruling 1996-26 - LIFO does not need to be complicated any longer. From now on simply get through it from your apartment or at your business office from your mobile device or PC.

Get form

Experience a faster way to fill out and sign forms on the web.

Access the most extensive library of templates available.

Rul FAQ

471 costs were equal to book cost of goods sold both to type of costs being capitalized and amount of those costs. For example, manufacturers generally include direct labor, direct material, and overhead costs into book inventory.

IRC section 471 contains the general rules describing how taxpayers with inventories should account for their gains and losses. These inventory accounting rules include how to account for cost of goods sold as well as indirect costs.

Pre-production section 471 costs are defined as the section 471 costs described in § 1.263A–1(d)(2) that are direct material costs that a taxpayer incurs during its current taxable year plus the section 471 costs for property acquired for resale (see § 1.263A–1(e)(2)(ii)) that a taxpayer incurs during its current ...

Last-in, First-out (LIFO) and First-in, First-out (FIFO) are two methods of inventory accounting used for both financial accounting and tax. purposes.

Pre-production section 471 costs are defined as the section 471 costs described in § 1.263A–1(d)(2) that are direct material costs that a taxpayer incurs during its current taxable year plus the section 471 costs for property acquired for resale (see § 1.263A–1(e)(2)(ii)) that a taxpayer incurs during its current ...

Phone and Internet usage are a mixed cost for service businesses. For example, businesses can usually get fixed phone line fees and standard monthly rates for Internet access. However, making lots of calls or web usage beyond a basic data limit, or making unexpected calls overseas, may lead to extra charges.

Section 1.471-3 of the Income Tax Regulations provides rules for determining the cost of merchandise on hand at the beginning of the taxable year and the cost of merchandise purchased or produced since the beginning of the taxable year.

Answer and Explanation: IRC does not allow to book accounting using LIFO, and the taxpayers to apply LIFO for tax purposes have to apply it for the financial reporting's income measurement. Hence, companies that are using LIFO have to shift to FIFO or average cost for tax purposes.

STAN Related content

Recent Federal Income Tax Developments

by IB Shepard · 1996 — that have been previously determined by IRS ruling not to...

Use professional pre-built templates to fill in and sign

documents online faster. Get access to thousands of forms.

Keywords relevant

to Revenue Ruling 1996-26 - LIFO

Lastin

outerwear

3the

goods2

Total3

Education2

rul

STAN

1Absence

cfr

Improvements2

proc

Misc

valuing

Domestics

If you believe that this page should be taken down, please

follow our DMCA take down processhere.

Ensure the security of your data and transactions

USLegal fulfills industry-leading security and compliance

standards.

VeriSign secured

#1 Internet-trusted security seal. Ensures that a website is

free of malware attacks.

Accredited Business

Guarantees that a business meets BBB accreditation standards

in the US and Canada.

TopTen Reviews

Highest customer reviews on one of the most highly-trusted

product review platforms.

BEST Legal Forms Company

TOP TEN REVIEWS WINNER - 9 YEARS STRAIGHT!

USLegal has been awarded the TopTenREVIEWS Gold Award 9 years in a row as the most comprehensive and helpful online legal forms services on the market today. TopTenReviews wrote "there is such an extensive range of documents covering so many topics that it is unlikely you would need to look anywhere else".

USLegal received the following as compared to 9 other form sites. Forms 10/10, Features Set 10/10, Ease of Use 10/10, Customer Service 10/10.