Loading

Get Us Bank Underwriting C2 2002-2026

How it works

-

Open form follow the instructions

-

Easily sign the form with your finger

-

Send filled & signed form or save

How to fill out the US Bank Underwriting C2 online

Filling out the US Bank Underwriting C2 online is a crucial step in the mortgage process. This guide will provide comprehensive instructions to help you successfully complete the form and submit it efficiently.

Follow the steps to accurately complete your underwriting checklist

- Click ‘Get Form’ button to obtain the document and access it for completion.

- Begin by providing the borrower's information, including the U.S. Bank home mortgage loan number, correspondent name, and telephone number. Ensure all details are accurate for effective processing.

- Next, fill in the processor's name and the preferred closing date, which is essential for scheduling purposes.

- Specify the fax number for the underwriting decision to ensure prompt communication. It is important to verify that the number is correct to avoid delays.

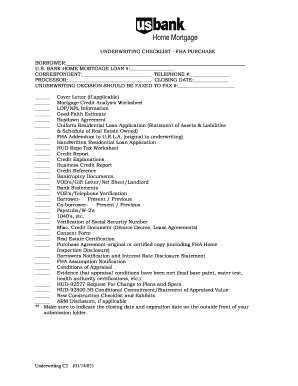

- Review the checklist of required documents to ensure all necessary paperwork is gathered. Each item listed, from the mortgage credit analysis worksheet to the purchase agreement, must be accounted for.

- If applicable, attach any cover letters and include specific information related to the FHA addendum or handwritten applications as needed based on your situation.

- Once all sections are completed and verified, you can save your changes, download the completed form for your records, print it for physical submission, or share it via fax or email as required.

Complete your documentation online now for a smoother mortgage process.

The four stages of underwriting consist of application submission, risk assessment, decision-making, and post-decision review. Each stage in US Bank Underwriting C2 ensures that everything from documentation to borrower eligibility is thoroughly examined. Engaging effectively in these stages leads to well-informed lending decisions.