Get Cg 20 15 2013-2026

How it works

-

Open form follow the instructions

-

Easily sign the form with your finger

-

Send filled & signed form or save

How to fill out the CG 20 15 online

Filling out the CG 20 15 endorsement form is an essential step in ensuring your commercial general liability insurance meets the needs of your specific business arrangements. This guide provides step-by-step instructions for users to fill out the form accurately and efficiently.

Follow the steps to complete the CG 20 15 endorsement form online.

- Click the 'Get Form' button to access the CG 20 15 endorsement form and open it for completion.

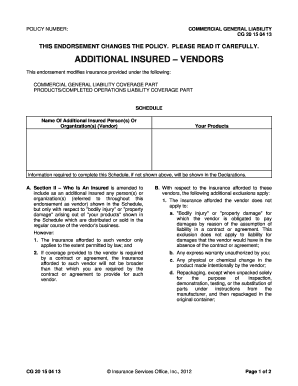

- Locate the Schedule section. In this area, you will need to enter the names of the additional insured persons or organizations (vendors) for which you are seeking coverage.

- In the 'Your Products' section, provide details about the products related to the endorsement. This information is crucial as it relates to the coverage being sought for the additional insured.

- Review Section II. Here, you must confirm your understanding that the endorsement modifies the insurance provided for the additional insured regarding 'bodily injury' or 'property damage' associated with your products.

- Familiarize yourself with the exclusions mentioned in the endorsement. These outline limitations on the coverage provided to vendors and should be acknowledged as you fill out the form.

- Complete any remaining sections as necessary, ensuring all information is accurate and complete according to your policy's requirements.

- Once you have reviewed all entries for accuracy, you can save your changes, download the completed form, print it, or share it as needed.

Complete your CG 20 15 endorsement form online today to ensure your insurance coverage is up to date.

Related links form

A CG 20 15 endorsement is a document that alters an insurance policy to include additional insured parties under specific conditions. This endorsement clarifies the extent of coverage afforded to those named as additional insureds, often crucial for contractors and subcontractors. Utilizing a CG 20 15 endorsement can streamline protection mechanisms for various business operations. Make sure your policies are properly aligned to leverage its benefits efficiently.