Loading

Get Irs 1042-t 2024-2026

How it works

-

Open form follow the instructions

-

Easily sign the form with your finger

-

Send filled & signed form or save

How to fill out the IRS 1042-T online

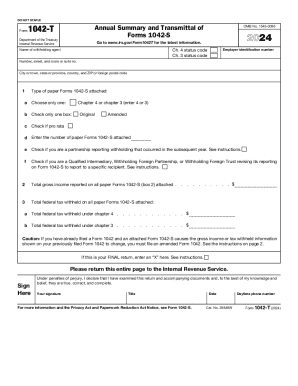

The IRS 1042-T form is crucial for transmitting paper Forms 1042-S, related to withholding income for foreign persons. This guide provides clear, step-by-step instructions to assist users in correctly filling out the form online.

Follow the steps to successfully complete the IRS 1042-T.

- Press the ‘Get Form’ button to access the IRS 1042-T form and open it in your browser.

- Fill in the identifying information, including your name as the withholding agent, employer identification number, and complete address with city, state, and ZIP code.

- In line 1, select the type of Forms 1042-S attached by entering '4' for chapter 4 or '3' for chapter 3. Make sure only one is selected.

- Check the appropriate box for original or amended forms in line 1b. Only one box should be checked.

- If applicable, indicate whether you are filing pro rata in line 1c by checking the box.

- In line 1e, check the box if you are a partnership reporting withholding that occurred in the subsequent year.

- Indicate in line 1f if applicable that you are a Qualified Intermediary, Withholding Foreign Partnership, or Withholding Foreign Trust revising its reporting.

- Enter the total gross income reported on all attached Forms 1042-S for line 2.

- Complete line 3 by entering the total federal tax withheld from the attached Forms 1042-S. Use line 3a for chapter 4 and line 3b for chapter 3, but do not complete both.

- If this is your final return, mark an 'X' in the final return box.

- Review all entered information for accuracy before proceeding.

- Once completed, save your changes, download a copy of the form, print it if needed, or share as required.

Start completing your IRS 1042-T document online for efficient filing.

Use Form 1042 to report the following: The tax withheld under chapter 3 on certain income of foreign persons, including nonresident aliens, foreign partnerships, foreign corporations, foreign estates, and foreign trusts. The tax withheld under chapter 4 on withholdable payments.