Get Irs 8582 2012

How it works

-

Open form follow the instructions

-

Easily sign the form with your finger

-

Send filled & signed form or save

How to fill out the IRS 8582 online

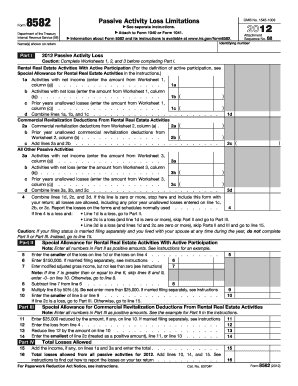

The IRS 8582 form is essential for reporting passive activity loss limitations for individuals and entities engaged in rental real estate activities. This guide provides straightforward instructions on how to complete the form correctly, ensuring you understand each component and step involved in the online process.

Follow the steps to successfully complete the IRS 8582 form online.

- Click ‘Get Form’ button to obtain the form and open it in the editor.

- Begin by filling in the name(s) shown on your return and your identifying number in the appropriate fields at the top of the form.

- Complete Part I. Begin with Worksheet 1 to determine your activities with net income and net loss from rental real estate activities and record those amounts in lines 1a, 1b, and 1c.

- For lines 2a and 2b, refer to Worksheet 2 to document commercial revitalization deductions and prior year deductions.

- Moving to lines 3a, 3b, and 3c in Part I, you will need to complete Worksheet 3 for all other passive activities, and then combine figures as instructed.

- On line 4, combine the totals from lines 1d, 2c, and 3d. If this total is zero or positive, you are finished with this part and can include the form with your return.

- If line 4 reflects a loss, proceed to Part II. Here, you must record the smaller loss from line 1d or line 4 on line 5, then complete additional calculations on lines 6 to 10.

- If applicable, check the requirements for Part III regarding special allowances and complete lines 11 to 14 accordingly.

- In Part IV, summarize the total losses allowed. For line 15, add any applicable income, and on line 16, summarize your total losses from all passive activities for the year.

- Once all information is completed, review the form for accuracy, then save, download, print, or share your completed IRS 8582 form as required.

Complete your IRS 8582 form online accurately and ensure timely submission alongside your tax return.

Get form

The income limit for passive activity losses generally applies to non-real estate activities and may phase out at certain adjusted gross income levels. Taxpayers can claim up to $25,000 in losses against non-passive income if their income is below a specific threshold. As you navigate these limits, the IRS 8582 provides essential guidance to ensure accurate reporting.

Get This Form Now!

Industry-leading security and compliance

-

In businnes since 199725+ years providing professional legal documents.

-

Accredited businessGuarantees that a business meets BBB accreditation standards in the US and Canada.

-

Secured by BraintreeValidated Level 1 PCI DSS compliant payment gateway that accepts most major credit and debit card brands from across the globe.