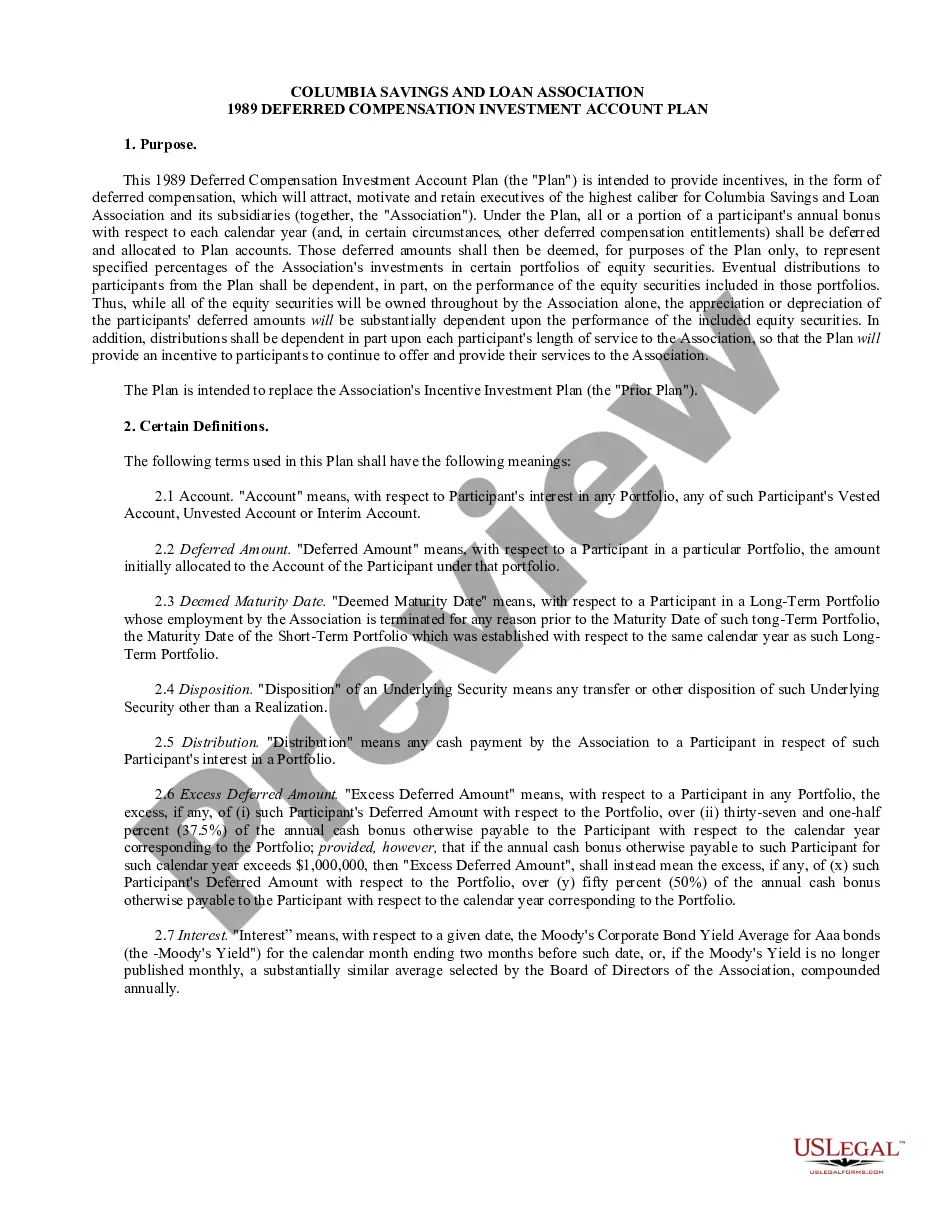

Riverside California Approval of deferred compensation investment account plan

Description

How to fill out Approval Of Deferred Compensation Investment Account Plan?

A documentation procedure invariably accompanies every legal action you undertake.

Starting a business, applying for or accepting a job offer, transferring ownership, and numerous other life circumstances necessitate the preparation of official paperwork that differs across the nation.

This is why having everything organized in a single location is so advantageous.

US Legal Forms constitutes the most comprehensive online repository of current federal and state-specific legal templates.

This is the easiest and most dependable method to acquire legal documents. All samples offered by our library are professionally crafted and verified for conformity with local statutes and regulations. Organize your documents and manage your legal matters effectively with US Legal Forms!

- Here, you can effortlessly discover and obtain a document for any personal or business purpose relevant to your county, including the Riverside Approval of deferred compensation investment account plan.

- Finding samples on the platform is incredibly simple.

- If you already possess a subscription to our library, Log In to your account, use the search bar to locate the sample, and click Download to save it to your device.

- Subsequently, the Riverside Approval of deferred compensation investment account plan will be available for additional use in the My documents section of your profile.

- If you are engaging with US Legal Forms for the first time, adhere to this straightforward guideline to acquire the Riverside Approval of deferred compensation investment account plan.

- Ensure you have accessed the correct page with your regional form.

- Utilize the Preview mode (if accessible) and navigate through the template.

- Examine the description (if available) to confirm the form meets your needs.

- Search for another document using the search option in the event that the sample is unsuitable.

- Click Buy Now once you identify the necessary template.

- Select the appropriate subscription plan, then Log In or create an account.

- Choose the desired payment method (credit card or PayPal) to proceed.

- Choose the file format and save the Riverside Approval of deferred compensation investment account plan to your device.

- Use it as required: print it or fill it out electronically, sign it, and submit where necessary.

Form popularity

FAQ

An eligible deferred compensation plan under IRC Section 457(b) is an agreement or arrangement (which may be an individual employment agreement) under which the payment of compensation is deferred (whether by salary reduction or by nonelective employer contribution).

Unlike a 401k with contributions housed in a trust and protected from the employer's (and the employee's) creditors, a deferred compensation plan (generally) offers no such protections. Instead, the employee only has a claim under the plan for the deferred compensation.

Record the journal entry upon disbursement of cash to the employee. In 2020, the deferred compensation plan matures and the employee is paid. The journal entry is simple. Debit Deferred Compensation Liability for $100,000 (this will zero out the account balance), and credit Cash for $100,000.

The plan is a voluntary savings program that allows employees to defer any amount, subject to annual limits, from their paycheck on a pretax basis. In addition, employee contributions and their earnings, if any, can benefit from the power of tax-deferred compounding.

You may withdraw money from your 457 plan when you retire or leave your job and possibly when you experience financial hardship. You'll have to make mandatory withdrawals after age 70 ½, and your beneficiary can withdraw money from the plan upon your death.

Typically, Fidelity says, you and your employer agree on when withdrawals can start. It may be five years, 10 years or not until you reach retirement. If you retire early, get fired or quit for another job before the due date, your employ gets to claw back some of that compensation as a penalty.

A deferred compensation plan withholds a portion of an employee's pay until a specified date, usually retirement. The lump sum owed to an employee in this type of plan is paid out on that date. Examples of deferred compensation plans include pensions, 401(k) retirement plans, and employee stock options.

Deferred compensation plans don't have required minimum distributions, either. Based upon your plan options, generally, you may choose 1 of 2 ways to receive your deferred compensation: as a lump-sum payment or in installments.

Qualified plans allow employees to put their money into a trust that's separate from your business' assets. An example would be 401(k) plans. Nonqualified deferred compensation plans let your employees put a portion of their pay into a permanent trust, where it grows tax deferred.

Deferred compensation plans are best suited for high-income earners who want to put away funds for retirement. Like 401(k) plans or IRAs, the money in these plans grows tax-deferred and the contributions can be deducted from taxable income in the current period.