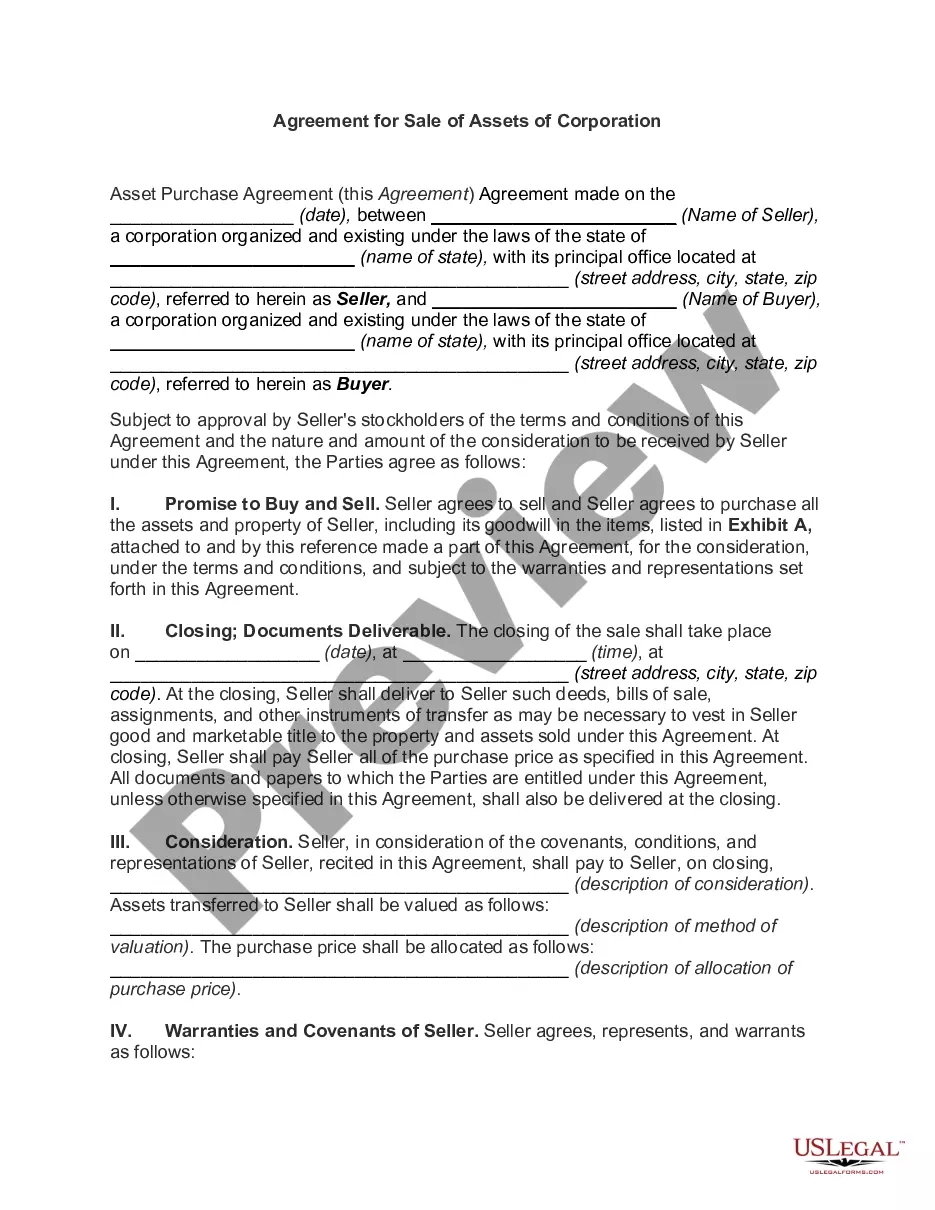

New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets

Description

How to fill out Agreement For Sale Of All Assets Of A Corporation With Allocation Of Purchase Price To Tangible And Intangible Business Assets?

Selecting the finest valid document template can be challenging. Of course, there are numerous designs accessible online, but how do you find the authentic version you need.

Utilize the US Legal Forms platform. This service offers thousands of designs, including the New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, which can be utilized for business and personal purposes. All forms are verified by professionals and meet state and federal requirements.

If you are currently registered, Log In to your account and click on the Obtain button to download the New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets. Use your account to review the valid forms you have previously obtained. Navigate to the My documents tab of your account and download another copy of the document you need.

Select the file format and download the valid document template to your device. Complete, modify, and print and sign the received New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets. US Legal Forms is the largest collection of valid forms where you can find various document templates. Use the service to download properly crafted documents that comply with state requirements.

- First, ensure that you have selected the correct form for your jurisdiction/area.

- You can preview the form by using the Preview button and review the form description to confirm it is the correct one for you.

- If the form does not meet your needs, utilize the Search field to find the appropriate form.

- When you are sure the form is suitable, click the Get now button to acquire the form.

- Choose the pricing plan you wish and enter the required information.

- Create your account and complete your order using your PayPal account or credit card.

Form popularity

FAQ

A Purchase Price Allocation (PPA) adjustment in accounting reallocates the purchase price among the assets being acquired. This process ensures that both tangible and intangible assets are correctly valued and reported. Utilizing the New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets ensures that your PPA adjustments align with legal and financial standards.

Yes, the amortization of Purchase Price Allocations (PPA) can be tax deductible. This means that businesses can deduct the amortized expenses over time, which can provide a financial benefit. Under the New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, understanding these deductions can help you manage overall tax liability effectively.

In New Mexico, the apportionment factor generally relies on the same three factors as in other states: property, payroll, and sales. The state's unique blend of these elements will define your business's tax obligations. When handling the New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, this factor is essential for ensuring compliance and financial accountability.

In New York State, the apportionment factor is calculated similarly, focusing on the relative share of property, payroll, and sales within the state. Businesses must track these metrics accurately for tax reporting. If your corporation operates in multiple states, consider how the apportionment factor will interact with your New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets.

The apportionment formula in New Mexico typically consists of a three-factor approach: property, payroll, and sales. Each factor is weighted equally to determine how much of a corporation’s income is taxable in the state. This formula is particularly relevant when executing a New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, as it influences future tax liabilities.

Apportionment involves distributing income or expenses across different jurisdictions based on a specific formula. In New Mexico, different factors such as property, payroll, and sales can influence this calculation. When engaged in a New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, ensuring accurate apportionment can help maximize financial benefits.

To dissolve a corporation in New Mexico, you must file Articles of Dissolution with the Secretary of State and settle all outstanding debts and tax obligations. After dissolution, you should properly allocate any remaining assets in line with a New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets to ensure compliance with legal and fiscal requirements.

Depreciation reduces the tax basis of an asset over time, reflecting its decrease in value due to wear and tear. When preparing for a New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, consider how depreciation affects the valuation of both tangible and intangible assets, as this will influence your overall financial strategy.

Yes, there is a personal property tax in New Mexico. This tax applies to tangible assets owned by the business and must be reported annually. When negotiating a New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, it's crucial to account for this obligation as it can influence the valuation of assets.

The Ptet rate, or the Personal Property Tax rate, in New Mexico varies by county. Local governments assess the tax on tangible personal property, affecting businesses. If you’re entering a New Mexico Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets, understanding the rate can impact your transaction.