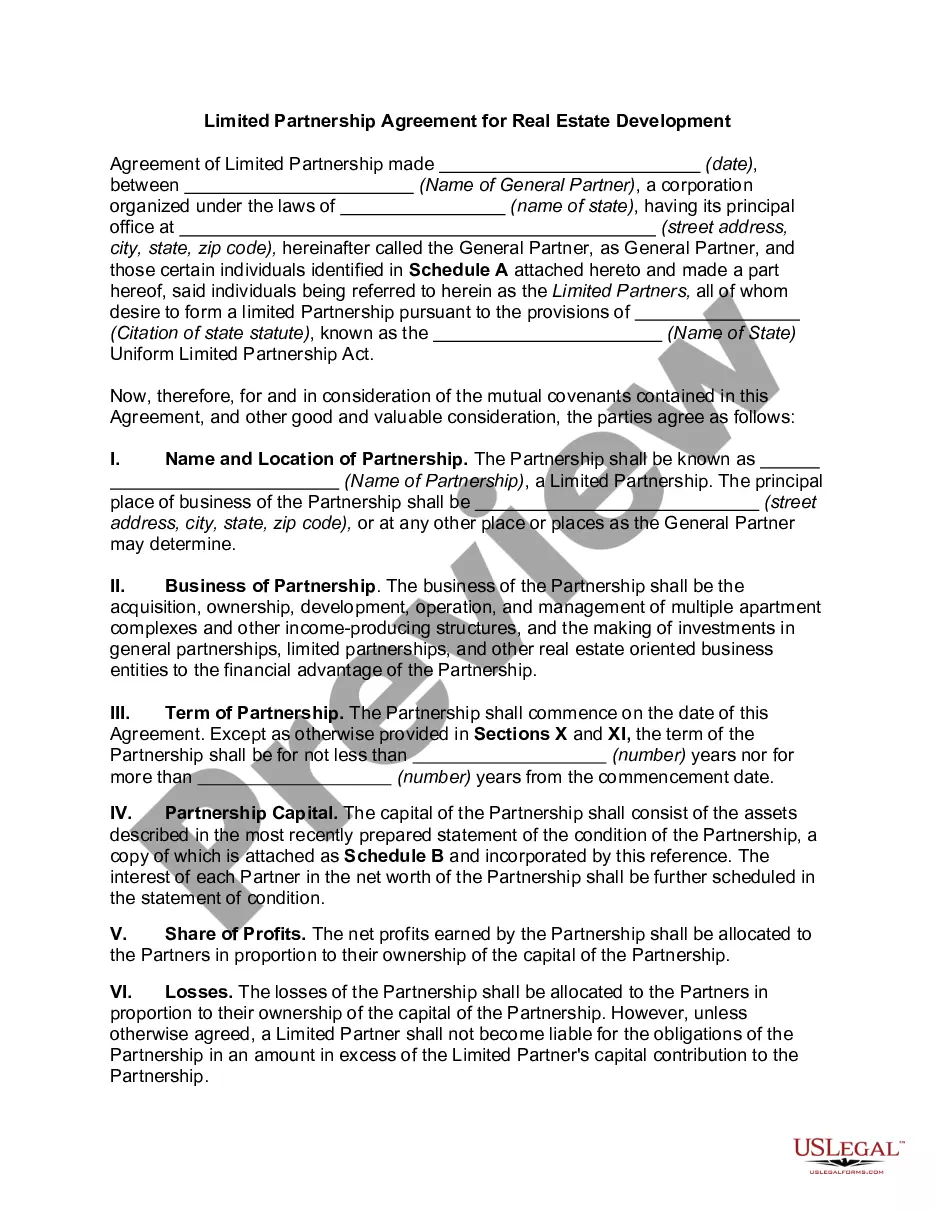

Kentucky Partnership Agreement for Development of Real Property

Description

How to fill out Partnership Agreement For Development Of Real Property?

Finding the correct legitimate document template can be quite a challenge.

Of course, there are numerous formats available on the web, but how can you locate the genuine document you require.

Use the US Legal Forms website.

First, make sure you have selected the correct form for your city/state. You can examine the document using the Review button and check the description to confirm it is suitable for you.

- The service offers thousands of formats, including the Kentucky Partnership Agreement for Development of Real Property, which you can use for business and personal purposes.

- All the forms are reviewed by professionals and comply with federal and state regulations.

- If you are currently registered, Log In to your account and click the Acquire button to download the Kentucky Partnership Agreement for Development of Real Property.

- Use your account to browse through the legal forms you have previously purchased.

- Navigate to the My documents tab of your account and retrieve another copy of the document you need.

- If you are a new user of US Legal Forms, here are simple instructions to follow.

Form popularity

FAQ

200bThe tax imposed by KRS 141.0401 is a tax imposed on those entities with limited liability in the state of Kentucky and not an income tax. Therefore, the Limited Liability Entity Tax (LLET) paid is not an add-back to determine Kentucky taxable income; it is deductible for Kentucky and federal purposes.

A single member LLC whose single member is an individual, estate, trust, or general partnership must file a Kentucky Single Member LLC Individually Owned Income and LLET Return (Form 725) or a Kentucky Single Member LLC Individually Owned LLET Return (Form 725-EZ) to report and pay any LLET that is due.

Kentucky's limited liability entity tax applies to traditional corporations, S corporations, LLCs, limited partnerships (LPs), and limited liability partnerships (LLPs). The tax is based on a business's annual gross receipts. For businesses with gross receipts less than $3 million, there is a minimum LLET of $175.

You may be exempt from withholding for 2021 if both the following apply: 20, you had a right to a refund of all Kentucky income tax withheld because you had no Kentucky income tax. liability, and. 20, you expect a refund of all your Kentucky income tax withheld.

Kentucky, however, imposes a Limited Liability Entity Tax (LLET) on LLCs that have more than $3 million in gross receipts or profits. The tax is on those same receipts or profits and is payable to the Kentucky Department of Revenue (DOR). Use DOR Form 720 to pay this tax.

INCOME TAX: PROPRIETORSHIPS AND PASS-THRU ENTITIES If the corporate partner's only business activity in Kentucky is the pass-through entity interest, then the corporate partner is subject to Kentucky's corporation income tax on its distributive share income multiplied by the three-factor apportionment formula.

Partnerships must create a Kentucky Form 4562, Schedule D and Form 4797 by converting federal forms.

For taxable years beginning on or after January 1, 2021, and before January 1, 2026, qualifying pass-through entities (PTEs) may annually elect to pay an entity level state tax on income. Qualified taxpayers receive a credit for their share of the entity level tax, reducing their California personal income tax.

These instructions have been designed for pass- through entities: S-corporations, partnerships, and general partnerships , which are required by law to file a Kentucky income tax and LLET return. Form PTE is complementary to the federal forms 1120S and 1065.

These partnerships are required by law to file a Kentucky Partnership Income and LLET Return (Form 765). Form 765 is complementary to the federal form 1065. HOW TO OBTAIN ADDITIONAL FORMS. Forms and instructions are available at all Kentucky Taxpayer Service Centers (see page 19).