Arkansas Fair Credit Act Disclosure Notice

Description

How to fill out Fair Credit Act Disclosure Notice?

US Legal Forms - one of the most extensive collections of legal documents in the United States - provides a range of legal record templates that you can acquire or print.

By utilizing the website, you can access thousands of documents for commercial and individual purposes, organized by categories, states, or keywords. You can obtain the latest versions of documents such as the Arkansas Fair Credit Act Disclosure Notice in just moments.

If you hold a membership, Log In and retrieve the Arkansas Fair Credit Act Disclosure Notice from the US Legal Forms repository. The Acquire button will be displayed on each document you review.

Once you are satisfied with the document, validate your choice by clicking the Get now button. Afterward, select the pricing plan that suits you and enter your details to register for an account.

Proceed with the payment. Use your Visa or Mastercard or PayPal account to complete the transaction. Obtain the format and retrieve the document to your device. Make changes. Fill out, edit, and print and sign the saved Arkansas Fair Credit Act Disclosure Notice. Each template you add to your account does not expire and belongs to you indefinitely. Therefore, to obtain or print another copy, simply visit the My documents section and click on the document you require.

- You can access all previously saved documents in the My documents section of your account.

- If this is your first time using US Legal Forms, the following are simple instructions to assist you in getting started.

- Confirm you have selected the correct document for the city/state.

- Click the Preview button to inspect the document's content.

- Refer to the document outline to ensure you have chosen the correct document.

- If the document does not satisfy your needs, utilize the Lookup field at the top of the page to find one that does.

Form popularity

FAQ

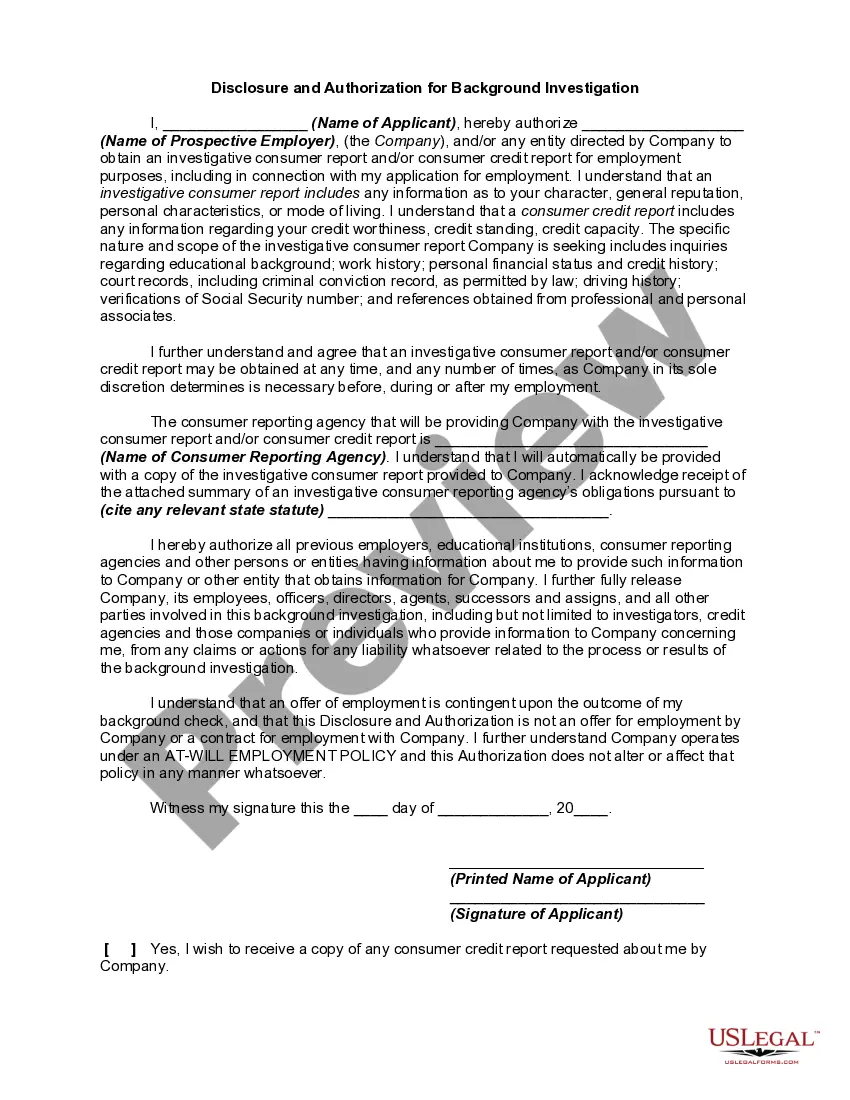

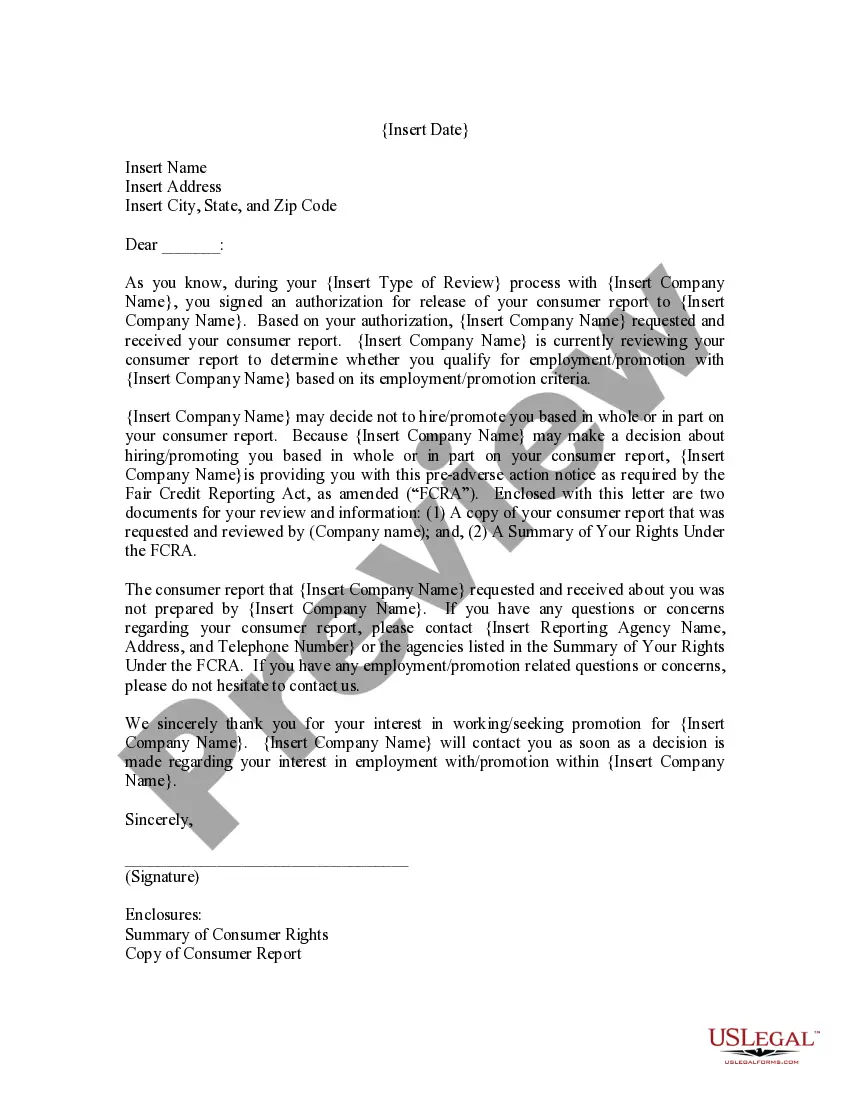

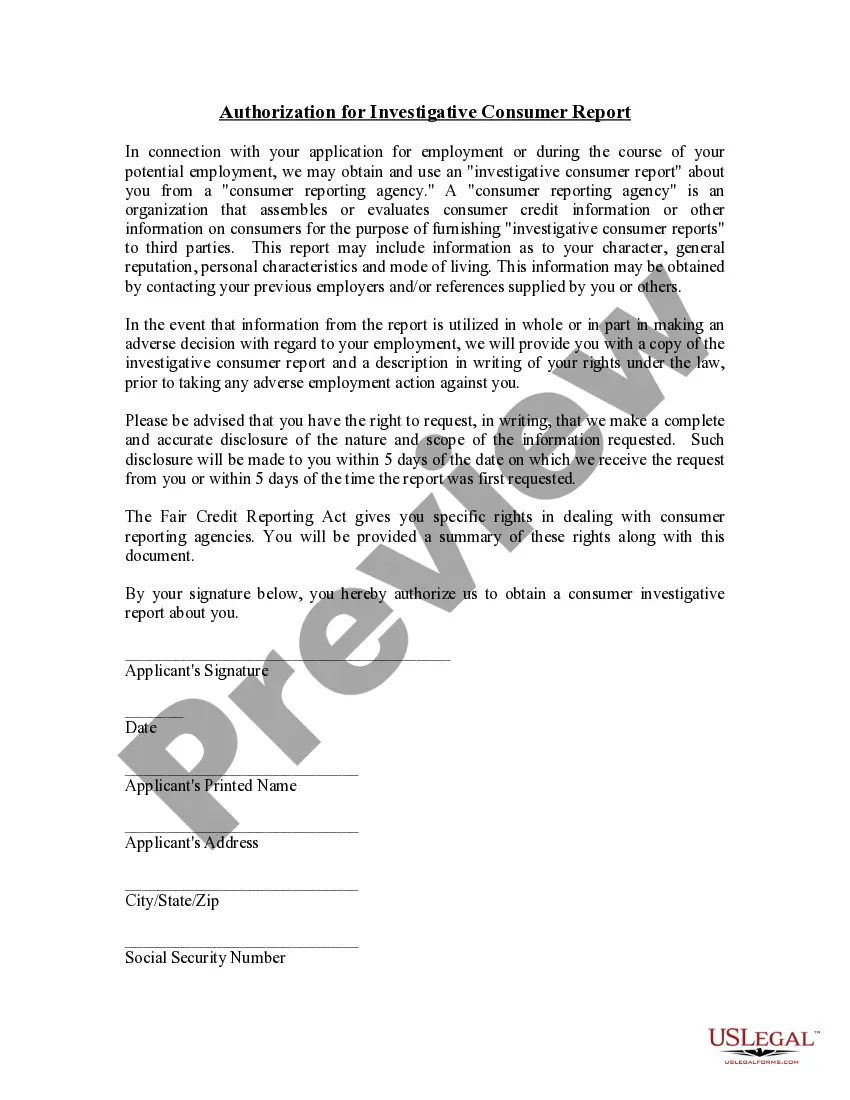

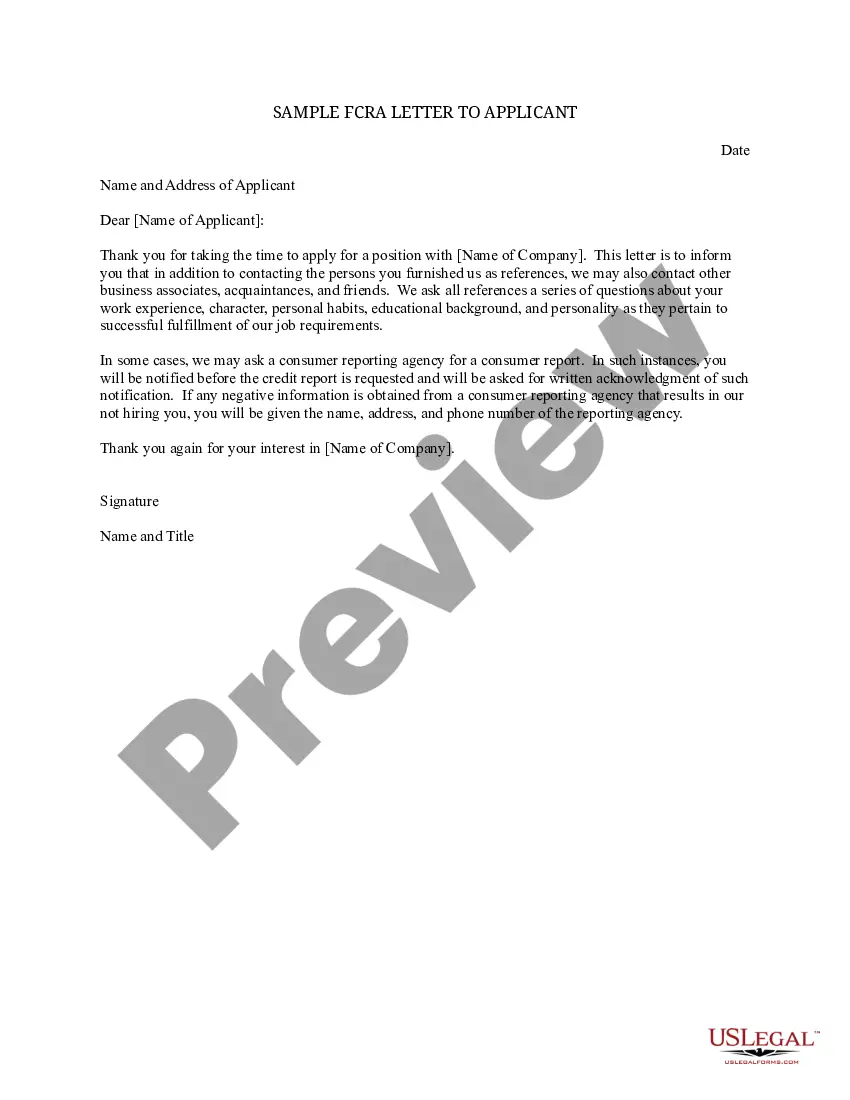

Under the FCRA, an employer may not run a background check on a prospective employee without first providing "a clear and conspicuous disclosure . . . in a document that consists solely of that disclosure, that a consumer report may be obtained for employment purposes." For efficiency, many employers include all

2022 You have the right to know what is in your file. report; 2022 you are the victim of identity theft and place a fraud alert in your file; 2022 your file contains inaccurate information as a result of fraud; 2022 you are on public assistance; 2022 you are unemployed but expect to apply for employment within 60 days.

The Fair Credit Reporting Act (FCRA) is a federal law that helps to ensure the accuracy, fairness and privacy of the information in consumer credit bureau files. The law regulates the way credit reporting agencies can collect, access, use and share the data they collect in your consumer reports.

The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.

What Is the Fair Credit Reporting Act?The right to know what's in your credit file.The right to request a credit score (more on this in a minute)The right to an adverse action notice if a creditor denies you financing because of something on your credit file.The right to seek damages for violations.More items...?

Under the FCRA, an employer may not run a background check on a prospective employee without first providing "a clear and conspicuous disclosure . . . in a document that consists solely of that disclosure, that a consumer report may be obtained for employment purposes." For efficiency, many employers include all

A creditor must disclose a consumer's credit score and information relating to a credit score on a risk-based pricing notice when the score of the consumer to whom the creditor extends credit or whose extension of credit is under review is used in setting the material terms of credit.

The Fair Credit Reporting Act describes the kind of data that the bureaus are allowed to collect. That includes the person's bill payment history, past loans, and current debts.

Consumer Rights Under the Fair Credit Reporting Act By law, they are entitled to one free credit report every 12 months from each of the three major bureaus. They can request their reports at the official, government-authorized website for that purpose, AnnualCreditReport.com.

Consumer reporting agencies must correct or delete inaccurate, incomplete, or unverifiable information. Inaccurate, incomplete, or unverifiable information must be removed or corrected, usually within 30 days. However, a consumer reporting agency may continue to report information it has verified as accurate.