Strict Foreclosure In Real Estate

Description

Form popularity

FAQ

The fastest way to stop a foreclosure is by filing for bankruptcy, which can temporarily halt the process. However, this approach can have long-term implications, so it is crucial to consult with a legal expert. Understanding the implications of strict foreclosure in real estate through resources like USLegalForms can help you make informed decisions to protect your interests.

The best alternative to foreclosure often includes options like short sales or deed in lieu of foreclosure. These methods allow homeowners to sell their property for less than what is owed or to voluntarily transfer ownership to the lender, mitigating further financial damage. Utilizing platforms like USLegalForms can help you explore strict foreclosure in real estate and identify strategies tailored to your circumstances.

Homeowners typically suffer the most in a foreclosure situation, facing financial strain and emotional distress. They may lose their homes and damage their credit scores, which can affect future borrowing possibilities. Understanding strict foreclosure in real estate can provide insight into the specific impacts on homeowners and highlight the importance of seeking assistance.

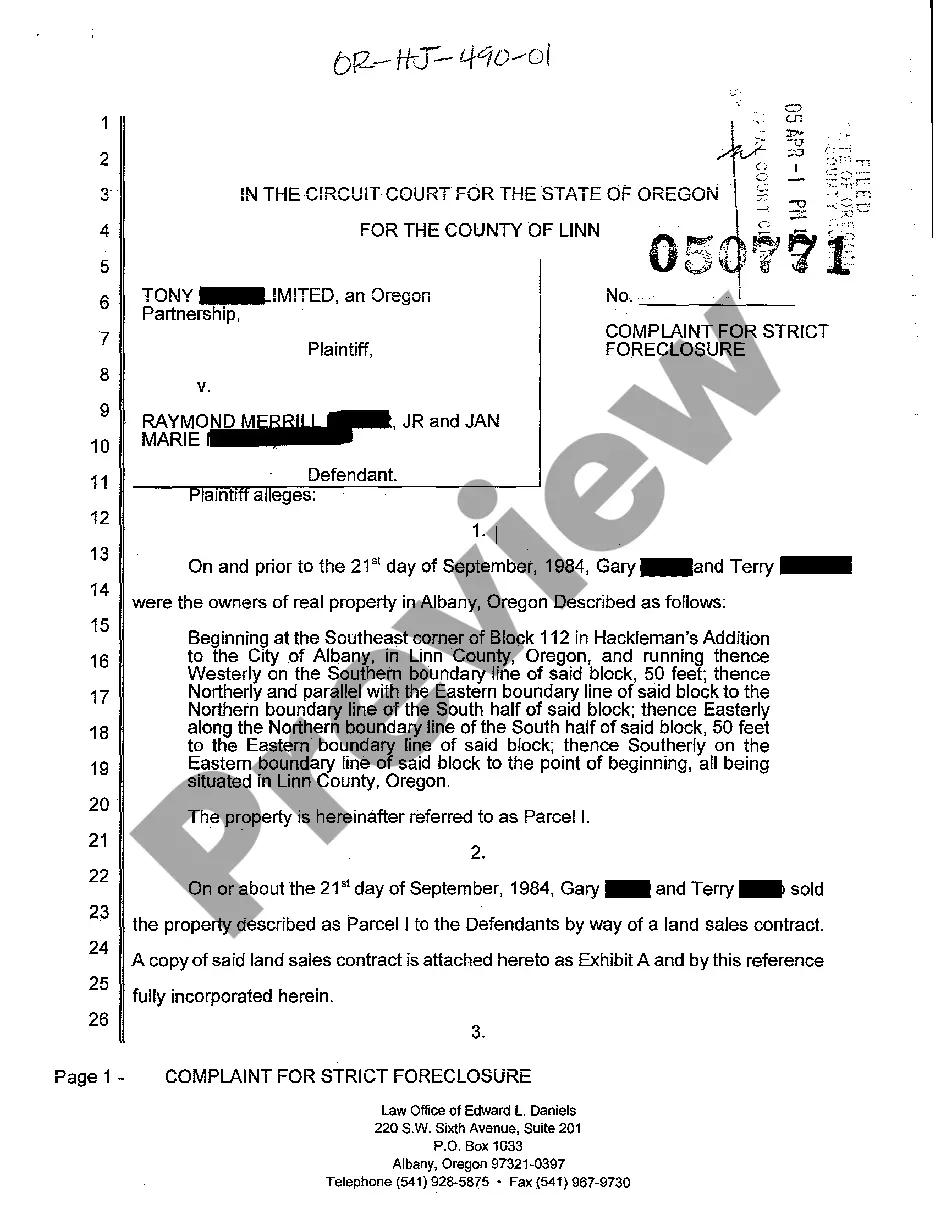

The most common method of foreclosure in real estate is the judicial foreclosure process. This approach requires lenders to go through the court system before taking possession of the property. It's essential to understand how strict foreclosure in real estate differs, as it can provide different options and strategies for homeowners in distress.

An example of strict foreclosure in real estate can be seen when a homeowner defaults on their mortgage in Connecticut. The lender can file a lawsuit to obtain a court order that allows them to take full ownership of the property without an auction. This method can expedite the process for lenders, allowing them to regain their investment. If you need more insights about strict foreclosure procedures, USLegalForms offers valuable templates and information that can help.

Strict foreclosure in real estate primarily occurs in states like Connecticut, New Jersey, and Vermont. In these states, if a borrower defaults, the lender can take back the property without selling it at auction. This process gives lenders a more direct route to reclaiming ownership. If you are navigating strict foreclosure, consider using USLegalForms for guidance and resources.

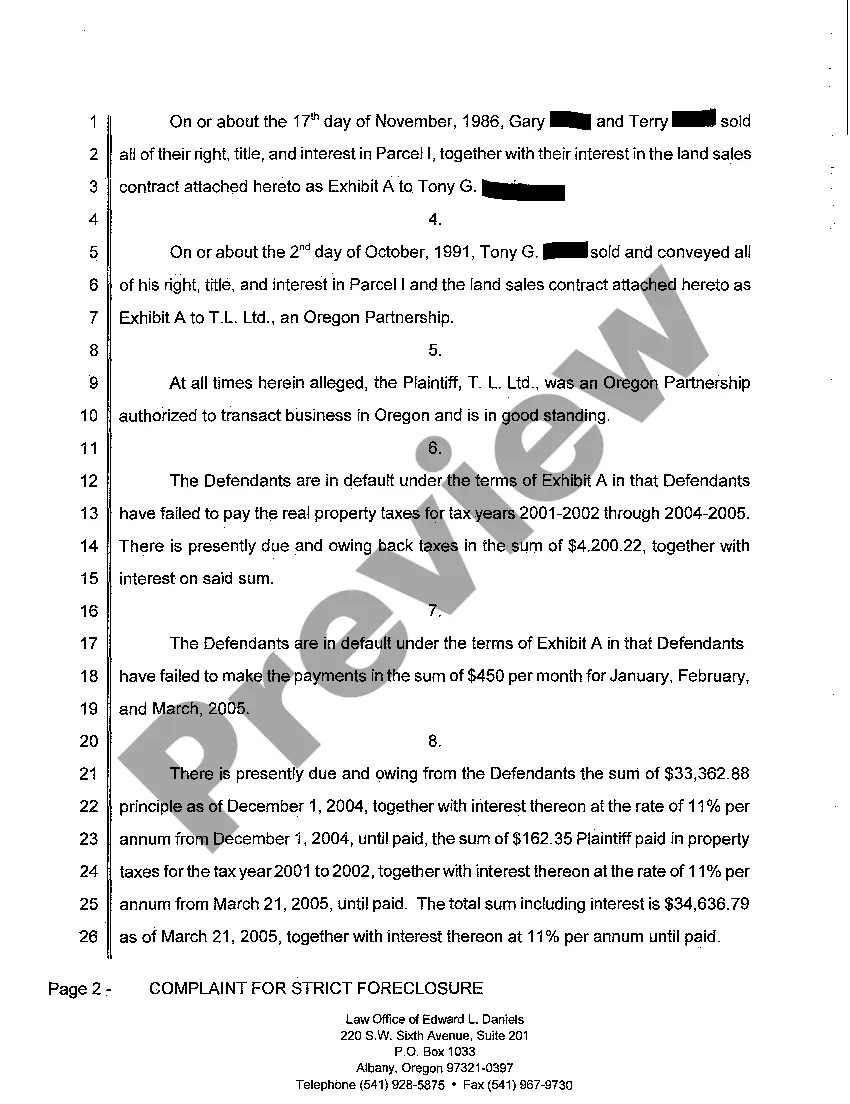

In a strict foreclosure, the lender files a lawsuit against the borrower to recover the owed amount. If the court rules in favor of the lender, the borrower may lose all rights to the property without the possibility of an auction. This decisiveness can leave the borrower with little recourse to avoid losing their home. To confidently navigate a strict foreclosure in real estate, consider resources like UsLegalForms to understand your legal rights and options effectively.

In Connecticut, the foreclosure process can vary in duration, but it often takes several months to over a year to complete. If the lender opts for a strict foreclosure, the timeline may be shorter, as these cases do not require an auction. Generally, the overall timeline depends on various factors, including court schedules and the specifics of the case. Understanding strict foreclosure in real estate in Connecticut helps you prepare for potential delays and consider your options.

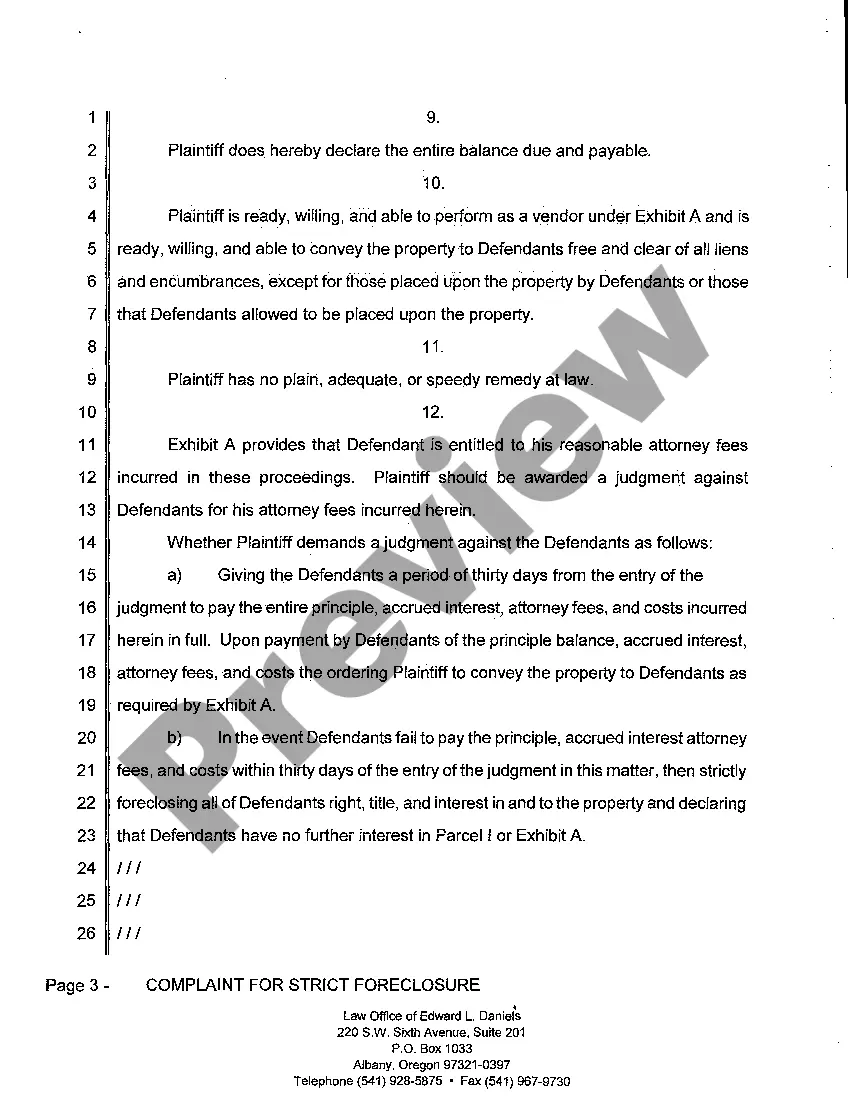

One key characteristic of strict foreclosure is that it allows the lender to bypass the lengthy auction process typically associated with regular foreclosure. Instead, the lender can gain title to the property swiftly, subject to court approval. This method can provide a faster resolution of the mortgage debt issue, which benefits lenders seeking to recover losses. Familiarity with strict foreclosure in real estate can help you understand your rights and obligations as a borrower or lender.

The 120-day rule for foreclosure generally refers to a requirement that lenders must wait a minimum of 120 days before initiating foreclosure proceedings. This rule is designed to give borrowers more time to rectify their financial situation and potentially save their homes. Understanding the implications of this rule is crucial for anyone navigating strict foreclosure in real estate.