Form Modification Loan With Balloon Payment

Description

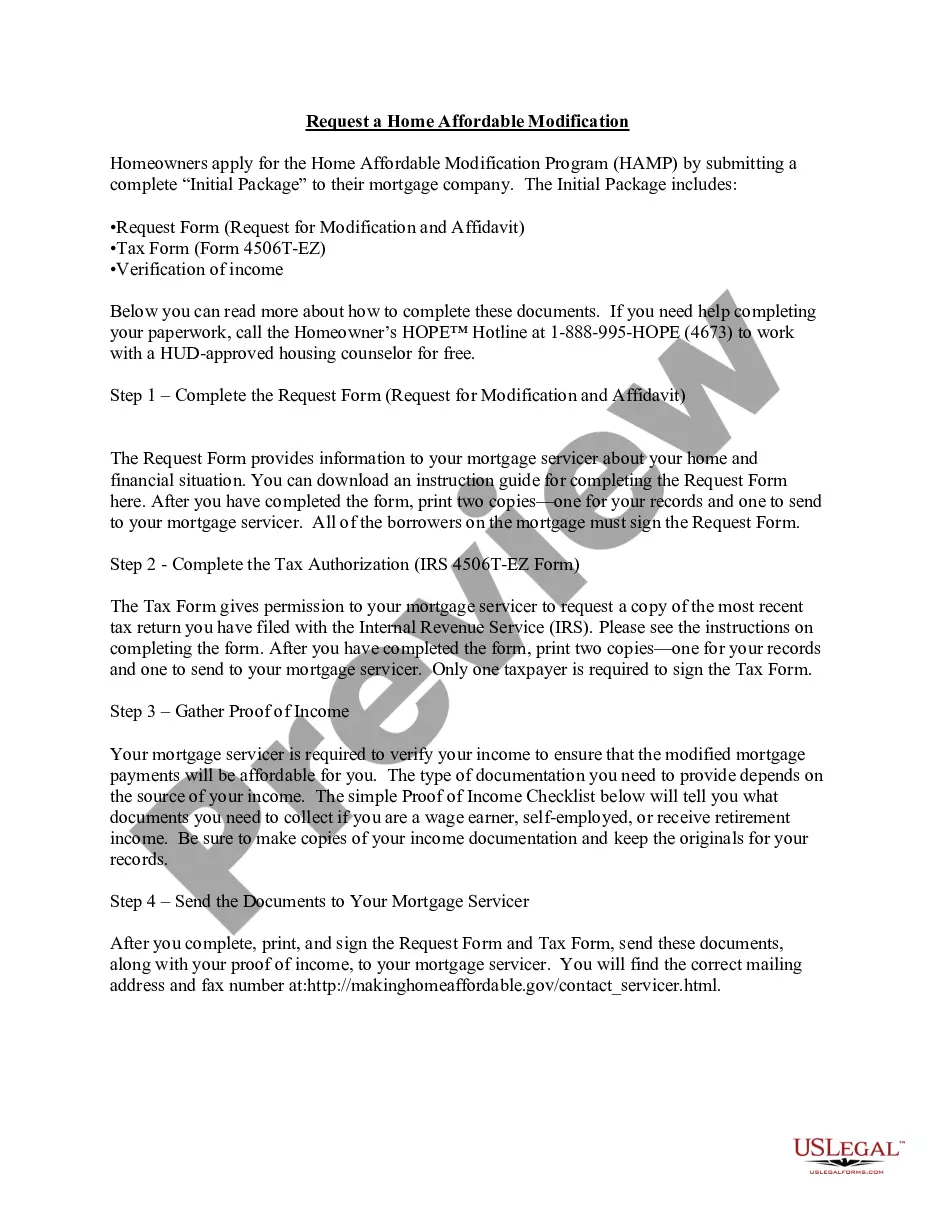

How to fill out HAMP Loan Modification Package?

The Form Modification Loan With Balloon Payment you see on this page is a reusable formal template drafted by professional lawyers in accordance with federal and state laws and regulations. For more than 25 years, US Legal Forms has provided individuals, organizations, and legal professionals with more than 85,000 verified, state-specific forms for any business and personal situation. It’s the fastest, easiest and most reliable way to obtain the documents you need, as the service guarantees bank-level data security and anti-malware protection.

Acquiring this Form Modification Loan With Balloon Payment will take you only a few simple steps:

- Search for the document you need and review it. Look through the file you searched and preview it or check the form description to verify it satisfies your needs. If it does not, make use of the search bar to find the right one. Click Buy Now once you have located the template you need.

- Subscribe and log in. Select the pricing plan that suits you and register for an account. Use PayPal or a credit card to make a prompt payment. If you already have an account, log in and check your subscription to continue.

- Get the fillable template. Pick the format you want for your Form Modification Loan With Balloon Payment (PDF, Word, RTF) and save the sample on your device.

- Complete and sign the paperwork. Print out the template to complete it manually. Alternatively, utilize an online multi-functional PDF editor to rapidly and precisely fill out and sign your form with a eSignature.

- Download your paperwork one more time. Use the same document again anytime needed. Open the My Forms tab in your profile to redownload any previously downloaded forms.

Subscribe to US Legal Forms to have verified legal templates for all of life’s situations at your disposal.

Form popularity

FAQ

We can use the below formula to calculate the future value of the balloon payment to be made at the end of 10 years: FV = PV*(1+r)n?P*[(1+r)n?1/r]

-The borrower's income was not sufficient to support the modified payment amount. -The borrower had already missed too many payments before applying for the modification. -The property value had declined, making it worth less than the outstanding loan balance.

In addition to extinguishing the debt by paying off the balloon payment, a borrower can: Refinance the loan. A lender may be willing to work with a borrower to repurpose the debt into a different loan vehicle or modify the terms of the original agreement.

A balloon payment is a larger-than-usual one-time payment at the end of the loan term. If you have a mortgage with a balloon payment, your payments may be lower in the years before the balloon payment comes due, but you could owe a big amount at the end of the loan.

What are two ways to calculate a balloon payment? Find the present value of the payments remaining after the loan term. Amortize the loan over the loan life to find the ending balance.