Debt Collector Information With Credit Card

Description

How to fill out Letter Informing Debt Collector Of False Or Misleading Misrepresentations In Collection Activities - Communicating Or Threatening To Communicate To Any Person False Credit Information, Including The Failure To Communicate That A Debt Is Disputed?

Managing legal documents can be exasperating, even for the most proficient professionals.

When you're seeking Debt Collector Information With Credit Card and don't have the opportunity to invest in finding the correct and current version, the experience can be overwhelming.

US Legal Forms meets all your requirements, from personal to business documentation, all in one location.

Utilize advanced tools to complete and manage your Debt Collector Information With Credit Card.

Here are the steps to follow after accessing the form you need: Confirm this is the right form by previewing it and reading its description. Ensure that the document is recognized in your state or county. Click Buy Now when you're prepared. Choose a monthly subscription plan. Select the file format you prefer, and Download, fill out, sign, print, and send your documents. Enjoy the US Legal Forms online library, backed by 25 years of experience and trustworthiness. Revamp your everyday document management into a straightforward and user-friendly process today.

- Tap into a resource pool of articles, guides, handbooks, and materials related to your situation and needs.

- Save time and effort in locating the documents you require, and utilize US Legal Forms’ sophisticated search and Preview function to find Debt Collector Information With Credit Card.

- If you have a monthly subscription, Log In to your US Legal Forms account, search for the form, and access it.

- Check the My documents tab to review the documents you've previously saved and manage your folders as desired.

- If this is your first experience with US Legal Forms, create an account and gain unlimited access to all the platform's benefits.

- A robust online form library could be a significant advantage for anyone looking to handle these situations effectively.

- US Legal Forms is a leader in web legal documents, offering over 85,000 state-specific legal forms available at your convenience.

- With US Legal Forms, you can access legal and organizational documents specific to your state or county.

Form popularity

FAQ

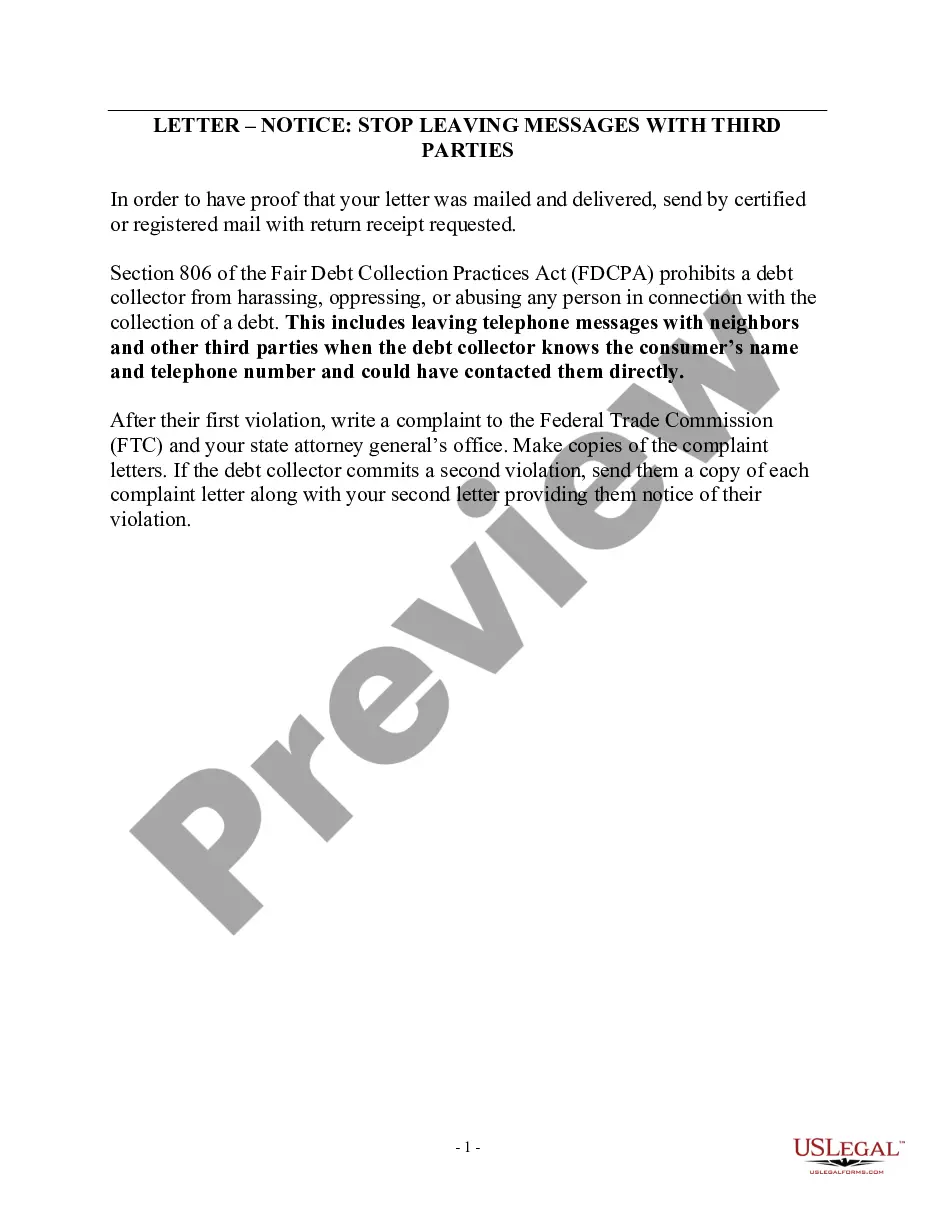

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

If you choose not to verify your identity by providing information, like your Social Security number, the debt collector will generally ask you for another form of identification, including: Account number for the debt in question, if you know it. Other contact information, such as your current or previous address.

Paying a debt collector with a credit card won't make the debt go away. Instead, you will have new debt?and additional finance charges. ?Paying one debt off while racking up new debt is an oxymoron in itself,? warns Howard Dvorkin, founder of Consolidated Credit Counseling Services.

This is where we get our "7-in-7" concept. You can attempt to contact a consumer about 1 debt 7 times in 7 days. And it's the "1 debt" that's key here. Phone numbers do not matter; how many debts your agency has for the consumer does.

Summary: If you're being sued by a debt collector, here are five ways you can fight back in court and win: 1) Respond to the lawsuit, 2) make the debt collector prove their case, 3) use the statute of limitations as a defense, 4) file a Motion to Compel Arbitration, and 5) negotiate a settlement offer.